When Should a Company Obtain an Intangible Asset Valuation?

Understanding When Should a Company Obtain an Intangible Asset Valuation?

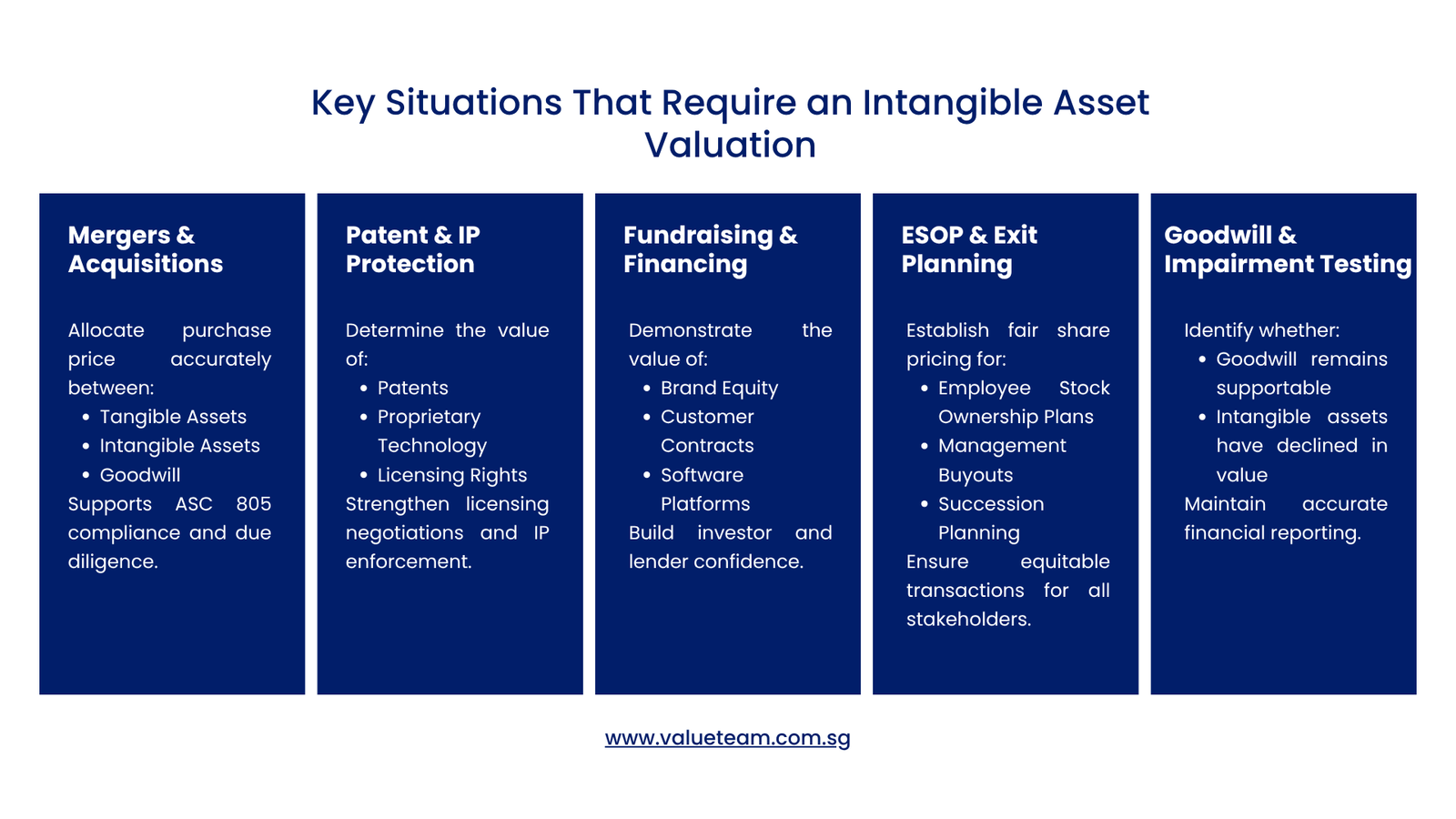

The corporate intangible asset valuation is used to measure the fair value of something that is not physical, like a patent or a trademark, a copyright, customer relationships and software. This valuation should be performed by a company when acquiring or merging a company, when a company puts itself on the books of an employee stock ownership plan, when required by ASC 805 intangible asset valuation standards for financial reporting, in the event of impairment testing, when entering into licensing agreements, or for litigation purposes. This valuation helps with the preparation of accurate financial statements, making informed business decisions, and adhering to accounting and tax laws. In a tech start-up that’s trying to safeguard its IP, or in a big company handling intangibles from deals, it’s imperative to know when to call in the valuation professionals.

Are You Planning an Acquisition or Merger?

The most common requirement for the valuation of corporate intangible assets is from acquisitions. The price of acquiring another company has to be divided up between tangible assets (buildings, equipment), intangible assets (customer lists, technology, brands) and goodwill. Intangible asset valuation isn’t well understood by many, and it can cause financial restatements and audit findings if not identified and valued properly. The valuation of, say, a mid-sized software company buying a competitor who has an existing database and a customer base, for example, involves valuing the technology platform, trademark rights, and customer base—each of which provides a different cash-flow benefit to the purchase transaction. Professional valuation makes the purchase price allocation (PPA) defensible and in accordance with GAAP.

Valuation isn’t just to help with accounting purposes; it’s also to help with a negotiation strategy. Sellers are generally emphasizing that their brand is well-recognized and/or they have loyal customers, and buyers want independent confirmation of the value of the assets. A credible valuation helps to close this gap. For a healthcare consulting company, think about a small practice that has a niche specialty and high credibility in its area. The client retention metrics, revenue concentration and competitive positioning underpin the value of that reputation, which justifies paying a premium and also prevents the buyer from paying too much for the intangibles that might not continue to work after the acquisition. It is also vital during stock-for-stock mergers, where each dollar of purchase consideration is of significant importance to both parties that do the due diligence.

Are You Protecting Patents or Intellectual Property?

When companies must protect their IP investments, enter into licensing agreements, or determine the worth of their IP holdings for strategic planning, a patent valuation becomes crucial. In fact, in many companies, patents can be the most valuable asset, particularly in the biotechnology, pharmaceutical, semiconductor and software sectors, and many companies do not realize just how valuable they are. A formal valuation will measure the competitive edge that patents create and enable decisions on enforcing IP rights, licensing IP technology to third parties or acquiring complementary technology.

Suppose you are a manufacturing company that has created a breakthrough process with five granted patents. The company first runs a valuation, performed by the relief-from-royalty method, before it can be negotiated for use by other parties. The company performs a valuation before entering into licensing negotiations with potential parties, using the relief-from-royalty method that estimates the amount that a willing party would be willing to pay on an annual basis for the right to use the technology. The valuation shows that the patent portfolio has a $2 million annual value through royalties, making it appropriate to discuss patents with a high license negotiation energy level and also to invest in patent prosecution for pending patents. Likewise, when litigating, companies can obtain expert testimony using a detailed patent valuation. In addition, IP-intensive organizations will periodically review their portfolios to understand whether there are patents that are no longer being used that can be sold or abandoned to reduce the burden of maintenance costs.

Is Your Company Financing Growth or Seeking Investment?

As companies look for growth funding, be it from banks, through venture funding or private equity, lenders and investors are raising their “radar” on intangible assets, whether for collateral or value drivers. Corporate intangible asset valuation proves the power of a company’s brand, customer base, software applications and other IP-related income. This is especially true for asset-light business models in tech, SaaS, digital media and professional services companies, where tangible assets account for only 10-20% of the enterprise value.

A B2B SaaS business with $10 million in annual recurring revenue (ARR) and a customer renewal rate of 95% has some valuable customer relationships and proprietary software. A VC who’s reviewing the business will ask for proof that there’s a formal valuation of customer relationships, as well as technology, that backs the company’s valuation multiples (usually between 6x-10x ARR for the good SaaS companies). On the other hand, if a company is looking for a traditional bank loan, it may be shocked to discover that the best collateral it has is its brand equity and customer contracts, which a secured lender does not want to rely on. The role of valuation reports in these scenarios is to help build trust, speed up funding processes, and possibly even refine the terms provided.

Are You Setting Up an ESOP or Exit Strategy?

The company must be valued by an independent valuation procedure for the establishment of the shares of the employees or employees and management in the case of employee stock ownership plans (ESOP) and management buyouts. Intangible assets like the company culture, leadership team expertise, customer loyalty, and operational processes can account for 40-70% of enterprise value for founder-owned businesses whose owners are looking to hand over the business to their employees or exit the business. With a detailed corporate intangible asset valuation, these components are distinct, allowing share prices to be defensible and fair for all involved, including employees, vendors, and the remaining shareholders.

If the company is a 20-year-old engineering consulting company with solid client relationships and proprietary processes, and the management team is considering setting up an ESOP to incentivize their highest-skilled engineers and offer a succession plan, then the answer is likely “yes. If a company is a 20-year-old engineering consulting firm with good client relationships and proprietary processes, and the management team is considering setting up an ESOP to incentivize their most highly skilled engineers and provide a succession pathway, the answer is maybe “yes. The valuation process also highlights that 55% of the value of the enterprise is attributed to intangible assets, which include the business’s reputation and experience in niche markets, long-term customer relationships, and unique processes for delivering projects. This separation allows the ESOP trustee and management to come up with a price per share that is representative of the economic value that the engineering team has created. It also explains what assets would be lost if key individuals were to leave following a transaction, so that management can take steps to offer retention incentives to key jobs. If that isn’t the case, then ESOPs can end up paying too much for goodwill or not valuing the intangible assets, which will drive future cash flows.

Is Your Company Facing Impairment Risk or Reporting Significant Goodwill?

Any acquirer that has acquired a company and acquired significant amounts of intangible assets or goodwill should periodically assess the goodwill or intangible assets for impairment. As per ASC 805 and IAS 36, when market conditions change, competition increases, and customers leave, management must consider whether the values of these assets that management has recorded are supportable. An impairment test involves comparing the carrying value of the asset or the cash-generating unit with the fair value of the asset or with the market-observable price (usually the fair value is calculated using a discounted cash flow analysis). When the fair value is less than the carrying value, the impairment charge appears in the income statement, which decreases profitability and shareholder equity.

Assume a technology company bought a competitor for $50 million three years ago, spending $30 million on intangible assets and goodwill (including customer relationships and technology). Now, if the market disruption or customer churn indicates that future cash flows are likely to be 30% lower than they were when the business was acquired, management will have to have an impairment analysis done. This valuation is done by an independent valuer who establishes the current fair value and calculates the impairment loss. Appropriate and accurate impairment testing safeguards the credibility of companies’ financial reports and helps prevent surprises in the future. Annual impairment reviews with consistent methodologies and assumed parameters help finance teams in the efficiency of their audit process and minimize the chances of a qualified opinion or restatement.

Five Essential Steps in the Valuation Process

- Step 1: Identify and Classify Assets—Identify assets that exist, what sorts they are, and their importance to the valuation purpose (acquisition, impairment, licensing).

- Step 2: Valuation Methodology—Based on data available and asset characteristics, choose from the market approach, income approach or cost approach (relief from royalty approach for IP, multi-period excess earnings approach for customer relationships, replacement cost approach for databases).

- Step 3: Collect Financial and Operational Data—Obtain historical financial statements, revenues by customer segment, customer retention data, competitor data and other forward-looking business plans and forecasts to support cash flow forecasting.

- Step 4: Develop Key Assumptions and Model—Construct a valuation model that includes revenue growth rates, margin assumptions, discount rates (WACC or other relevant risk-adjusted discount rates) and terminal value calculations.

- Step 5: Perform Sensitivity Analysis and Documentation—Test how changes in key assumptions (growth, margins, discount rate) affect conclusions and document all methodologies, data sources, and judgments for audit and compliance purposes.

Table 1: Common Intangible Asset Valuation Methodologies -When Should a Company Obtain an Intangible Asset Valuation?

| Methodology | Best For | Key Inputs |

| Relief from Royalty | Patents, trademarks, licenses | Licensed revenue, royalty rate, discount rate |

| Multi-Period Excess Earnings | Customer relationships, contracts | Revenue, margin growth, attrition rate |

| Cost Approach | Software, databases, user manuals | Development costs, obsolescence adjustments |

| Market Comparables | All—where observable transaction data exists | Comparable transaction prices, multiples |

Common Challenges and Lessons Learned

Valuation of intangible assets is subjective in nature, and the following are some difficulties encountered: First, many companies do not have detailed historical financial data by customer segment or product line to isolate the contribution of particular intangible assets to cash flows. Secondly, expectations for future growth, attrition and competition can differ widely depending on market expectations and management opinion. Valuation done in a bull market can appear more favourable during a period of a bear market. Third, valuers must often use the income or cost approaches for valuing many intangible assets – approaches that rely heavily on projections of cash flows and the assumptions underlying the discount rate. Such challenges highlight the necessity for hiring seasoned valuers who are well-versed in accounting principles and the industry.

Experience shows that there are several best practices: (1) do not wait to the last minute in a transaction process or planning process to value the assets, because this causes you to make conservative or questionable assumptions to arrive at the valuation. (2) Create comprehensive books of accounts, broken down by business line or customer group, to assist in valuation analysis and tracking and measuring post-acquisition performance against expectations. (3) Engage tax professionals in addition to valuation experts, because valuation conclusions can have a bearing on the financial reporting and tax deductions for acquired intangibles under §197. Revisit valuation assumptions every year of the first five years after closing for acquisitions where there is a deviation from the projected cash flows, as it could be an indication of impairment or opportunities to optimize the integration. (5) Make assumptions clearly documented – auditors and regulators would look for clear rationales for the key judgment areas. By adopting a mindset of continuous valuation as opposed to a one-off process, organizations will benefit from improved reporting quality, tax efficiency and strategic decision making over the long term.

Real-World Application: A Retail Acquisition Case Study

A national mid-market retailer purchased a regional store chain that had 50 stores and a well-known brand recognition and customer loyalty program. The selling company had $200 million in sales per year, but was losing margin due to evolving consumer preferences. The offerer made a cash and equity offer for $160 million, which was much higher than the company’s book value. Intangible asset valuation standards in ASC 805 required the allocator to allocate the purchase price to identifiable assets. During the valuation process, three intangible assets were identified as being significant:

- Customer List and Loyalty Program—Worth $45 million, based on the value of the customers’ database, shopping history and brand loyalty—this supports retention rates above market.

- Assessed Trademarked Brand and Store Names valued at $22 million (with an assumption of 8% on projected store revenues).

- In-Store Lease Rights—Going for $18 million as a contractual intangible, these are the favourable lease terms for locations that draw high amounts of foot traffic at rates below market.

The valuation resulted in a valuation of intangible assets of $85 million, of net tangible assets of $50 million and of goodwill of $25 million. After acquisition, the acquirer monitored the performance of the customer list (attrition, spending patterns) and then compared it with projections. The finance team spotted a sign of impairment, and when the number of customer churns was 15% higher than expected, it called in the valuation firm to review. The revised analysis resulted in a $12 million impairment charge that the company took in Year Two. This openness ensured the financial integrity of the company with investors and gave them valuable feedback: the analysis of the impairment showed that some store sites had higher rates of attrition, and so the attention of management was drawn to the sites which were not performing, so that integration and marketing campaigns could be targeted at them. A lack of a disciplined valuation and impairment review process could have caused the company to cover up the problem, and then be hit by a much bigger and more severe write-down.

Frequently Asked Questions (FAQ) : When Should a Company Obtain an Intangible Asset Valuation?

How long does an intangible asset valuation typically take?

The length of time may vary based on the complexity of the valuation, availability of data and whether the valuation is used for transaction closing or routine reporting. An easy single asset valuation can take anywhere from 4 to 6 weeks, while a full-scale corporate intangible asset valuation for a large acquisition, with multiple assets, stakeholder reviews and tax coordination, can take as long as 8–12 weeks. Organized financial data in advance and provide it greatly speeds the process up.

Who should perform an intangible asset valuation?

An independent, credentialed appraiser, usually a CVA (Chartered Valuation Analyst), a member of the American Society of Appraisers (ASA), or a specialist at a Big Four accounting firm should be used for valuations. Independence plus credentials are crucial to getting the audit accepted and external trust, especially in M&A and financial reporting situations.

What is the difference between book value and fair value of intangible assets?

The book value represents the value of the historical cost of the intangibles acquired in the books (after amortization). The fair value of an asset is equal to the market price or present value of the expected cash flows associated with the asset. Fair value is the basis for acquisition accounting, impairment testing and financial reporting, while book value is the recorded, historical basis for ongoing amortization and tax depreciation.

Can a company value its own intangible assets or must it hire external experts?

Internal teams can collect data and be helpful in analyzing it; however, external independent teams should be encouraged where possible for regulatory compliance, audit acceptance and objectivity. The internal valuation might not be sufficiently credible for litigation, financing or auditing. Benchmarking databases and the industry’s expertise are also provided by outside experts, which help to increase valuation reliability.

How often should a company update its intangible asset valuations?

Annual impairment testing is performed on an annual basis for financial reporting purposes if there are indicators (ASC 360, ASC 805). Valuations are normally provided to support the allocation of the purchase price at the date of acquisition for acquired intangibles. Periodic reviews (every 1-3 years) keep up-to-date understanding of the value of IP and customers for internal strategic purposes (such as licensing, M&A planning).

What role does a ‘patent valuation for businesses’ play in M&A due diligence?

A patent valuation for companies during an M&A due diligence process helps uncover the patents that have value, can be enforced and are relevant to the target’s core business. Valuers evaluate the strength of a patent (grant scope, prosecution history), competitive landscape, remaining useful life and licensing potential. This can be used to help in the process of negotiating purchase price and to determine potential post-acquisition exposure or concerns (such as patent litigation exposure).

When Should a Company Obtain an Intangible Asset Valuation? – Conclusion

An intangible asset valuation for a company is not just about ticking boxes for compliance. It can be used as a strategic tool to uncover the actual makeup of enterprise value, provide guidance for important business decisions and ensure the integrity of financial reporting. Valuation, whether it is for assessing an acquisition opportunity, licensing IP for new revenues, external financing or managing goodwill following an acquisition, gives the facts on which to take confident action with clarity.

Finance executives need to be mindful that in today’s economy, customer relationships, proprietary technology, brands, as well as contracts, are intangible assets that can provide a competitive advantage and generate cash flows. Waiting or not valuing first encompasses the risk of missing out on hidden value, mispricing deals or audit risk. Organizations with structured valuation disciplines, on the other hand, benefit from a variety of advantages such as negotiating M&A based on an informed strength, ensuring reliable compliance with GAAP and ASC 805 intangible asset valuation requirements, finding assets that are undervalued (e.g., for licensing or divestment), and creating stakeholder confidence through transparent financial communication.

To take the next step, evaluate your organization’s inventory and valuation of intangible assets readiness. For recent acquisitions, where goodwill is allocated to the accounts in the books and records, manage for impairment on an annual basis, using credible external valuations. For businesses running IP-rich business lines, consider doing a strategic patent valuation to uncover licensing or partnership opportunities. If you are considering a financing round or acquisition, start valuation planning early – the time and effort invested in doing so often comes back to you through the speed of the transaction, certainty of price and acceptance by regulators. Last but not least, foster an attitude that intangible asset valuation is a continuous process and not a crisis management situation within your finance and accounting teams. This attitude equips your organization to be competitive, report on your performance with credibility and develop enduring shareholder value.