Understand How to Account for Intangible Assets After Acquisition ASC 350 Guide

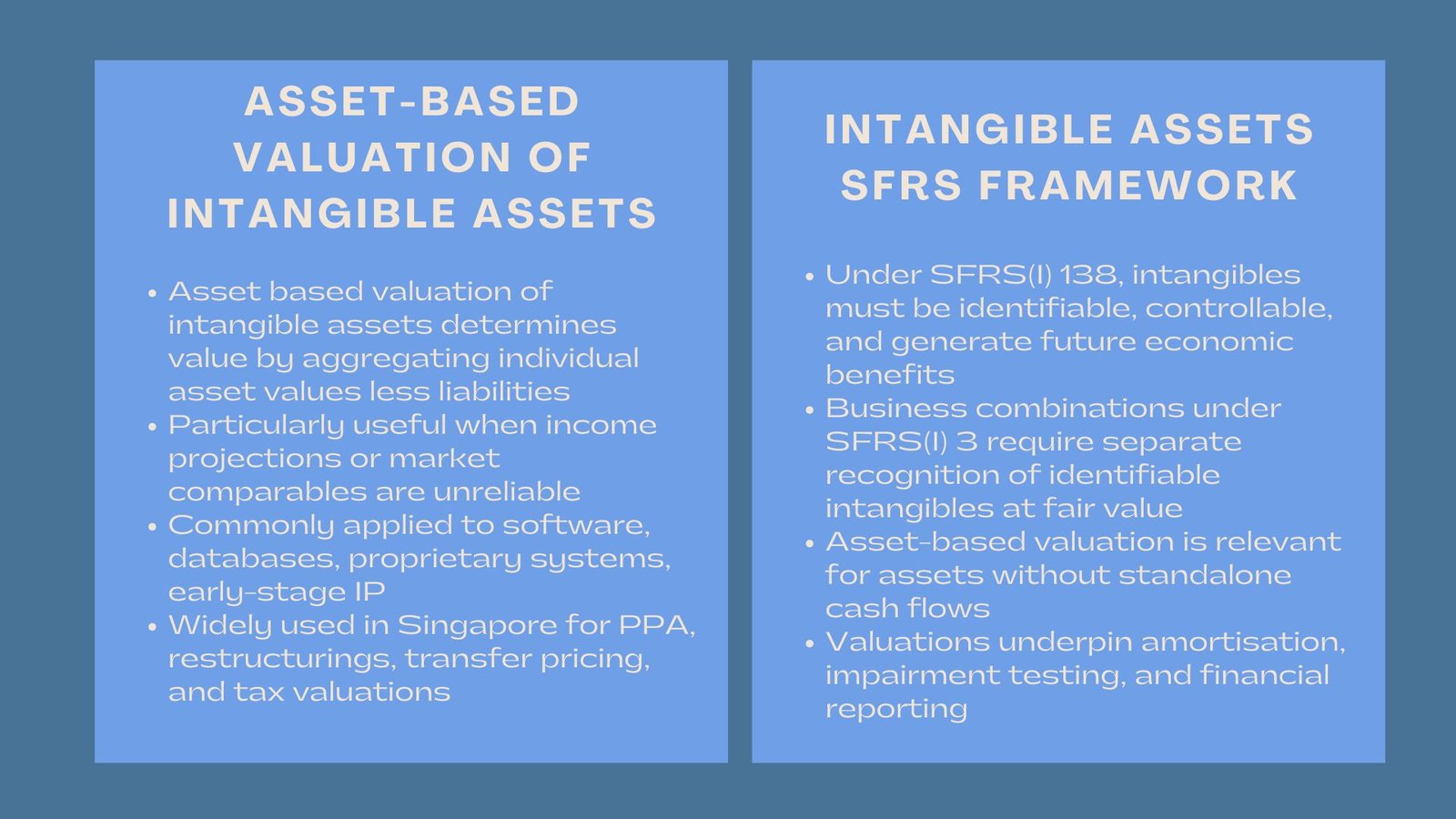

A purchase of a firm may also include associated with it both physical properties and operations as well as a variety of intangible assets such as brand names, customer lists, patents, or technology which may not have been previously reported as such. Once acquired, these intangibles have to be identifiable, measured and accounted for duly as per accounting rules, often requiring expertise in how to assess a business value for acquisition. In the United States, ASC 350 (Intangibles–Goodwill and Other) deals with this in the first place, and many companies rely on intangible asset valuation services in Singapore for compliance and reporting.

This article discusses the main provisions of the ASC 350, post acquisition treatment of intangible assets, valuation and amortization process, impairment testing requirements, and the real challenge companies have witnessed in their application.

Understanding ASC 350: The Core Framework

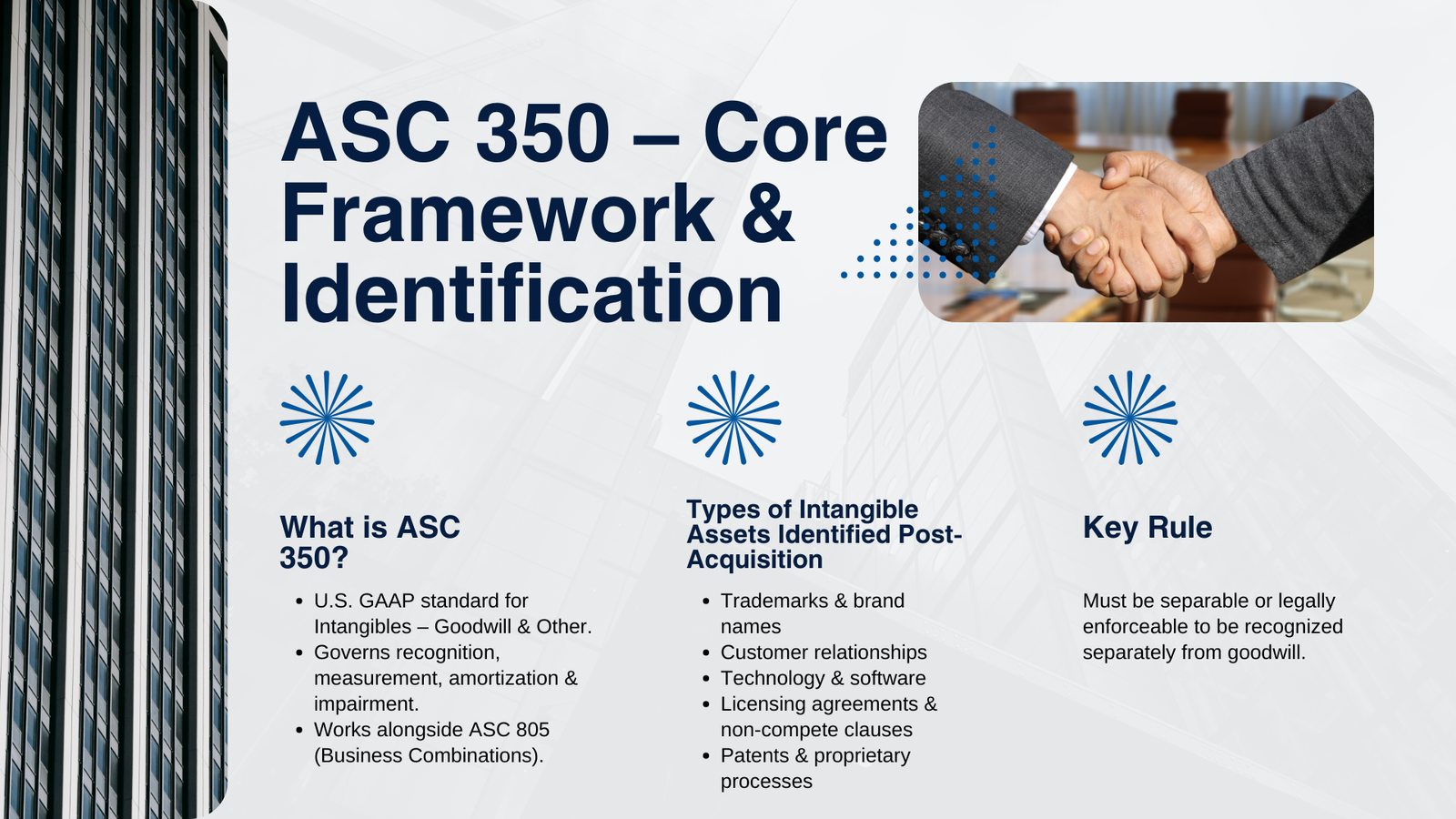

ASC 350 is one of the components of the U.S. GAAP framework, as given by the Financial Accounting Standards Board (FASB). It clearly deals with the issue of how intangibles other than goodwill should be identified, measured and thereafter treated as intangible assets.

Upon this aspect of distinguishing between finite lived intangibles- which are amortisated over their life period- and indefinite-lived intangibles- which are not amortisated but tested at the annual period of impairment.

The ASC 805 standard (Business Combinations) provides guidelines on how the assets are initially recognized in the acquisition process. The transaction is then formulated, after which ASC 350 comes in and it deals with how those intangibles are to be treated following acquisition.

Identifying Intangible Assets After an Acquisition

Identification of the intangible assets acquired is the initial step that should be followed in the application of ASC 350. Whereas certain ones might already be included in the balance sheet of the company bought, others might no longer be reflected until the purchase is made following the purchase accounting regulations.

Common types of intangible assets include:

- Trademarks and brand names

- Customer relationships

- Technology and software

- Licensing agreements

- Non-compete clauses

- Patents and proprietary processes

An asset is required to meet certain standards to be identifiable individually as compared to goodwill. What the asset must be against ASC 350 is that it could be identified with means that it could be separated to the business or it can come in the form of contract rights or legal rights.

Measuring and Recording Intangible Assets

Once identified, the acquirer shall need to measure each of the intangible assets at fair value as of the acquisition date. This can include third party valuation, in particular of more complicated or valuable intangibles.

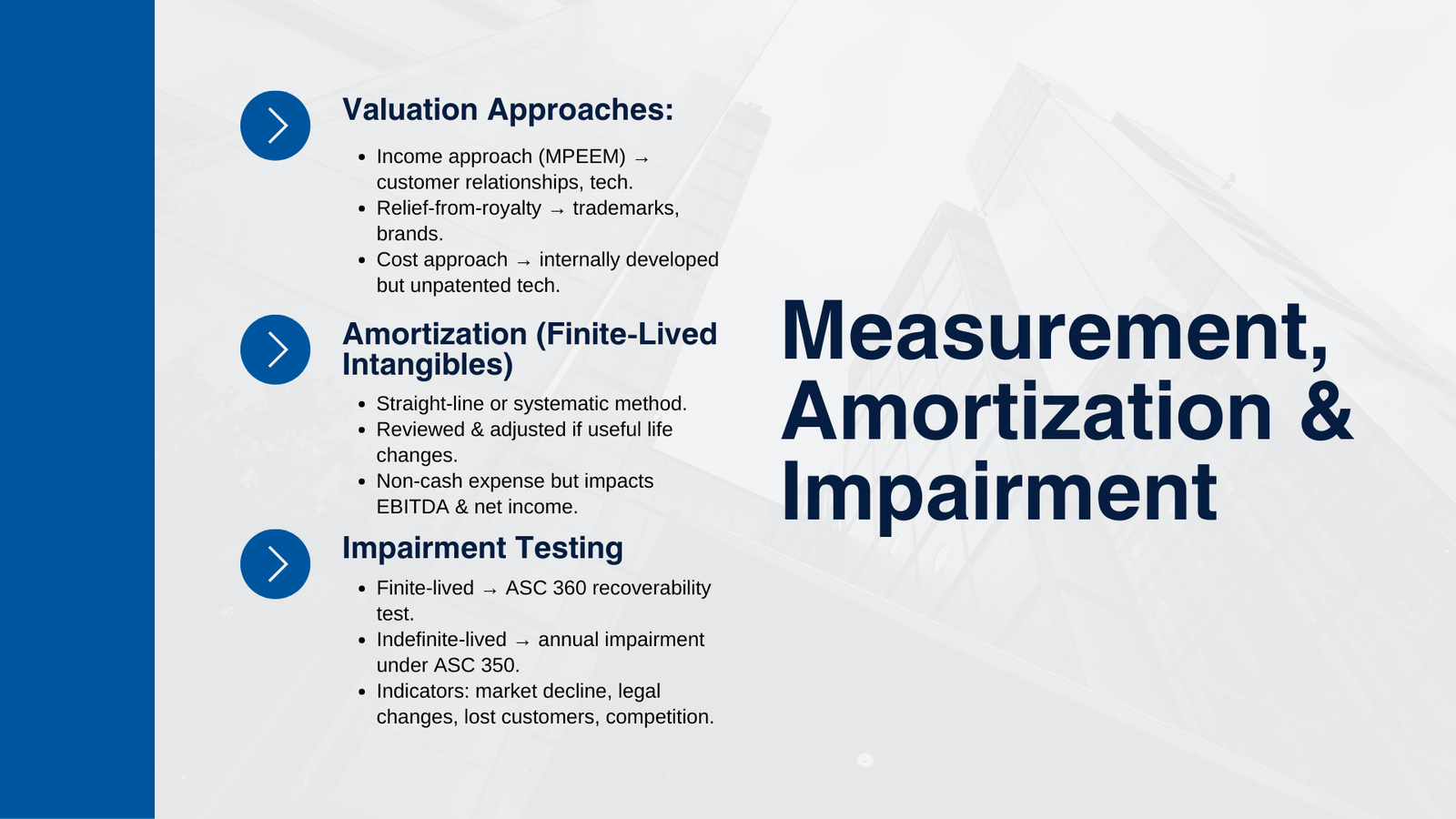

Different valuation methods may be applied, depending on the nature of the asset:

- Customer relationship or technology is normally common in the income approach like Multi-Period Excess Earnings Method (MPEEM).

- The relief-from-royalty approach normally applies to trademarks or brands.

- Cost based approach can be used on the internally developed but not patented technologies.

Such assets must be valued once and then put on the balance sheet of the acquirer as finite-lived or indefinite-lived.

Amortization of Finite-Lived Intangible Assets

Amortization applies to intangible assets having a limited life over which it has to be extended over calculated years of usefulness. The amortization expense is estimated as an expenditure against earnings on a straight-line or other systematic basis that measures the pattern of consumption of the asset.

The asset life at least should be reviewed after every report period. In case of extension or reduction of the life of either new information or changes in the market, the adjustment of the amortization schedule has to be done.

Notably, the amortization of intangible assets is a non-cash item; nevertheless, it decreases the reported earnings, which might influence the indicators such as EBITDA and net income.

Impairment Testing for Intangible Assets

The ASC 350 mandates companies to perform at least once a year of testing of indefinite-lived intangible assets to be impaired, but do so more often should there be indicators showing an impairment. Since those assets are not amortized, impairment testing is needed to provide that the recorded value over time is representative of economic reality.

In the case of finite-lived intangible assets, the impairment testing is carried out under ASC 360 (Property, Plant and Equipment) whereby an assessment on the recoverability of an asset must pass the triggering event.

Some common indicators of impairment include:

- Decline in market value

- Negative industry or economic trends

- Significant changes in usage or legal rights

- Loss of key customers or competitive advantages

If impairment is indicated, the asset’s carrying amount is compared with its fair value. Any excess of carrying value over fair value is recognized as an impairment loss.

The Role of Goodwill and Its Distinction

Goodwill is also under ASC 350 even though it is handled differently compared with other intangibles. Goodwill is an excess amount over the fair value of identifiable net assets and is not amortized. As an alternative, it is impaired on a yearly basis at the level of a reporting unit.

The companies should differentiate the goodwill with identifiable intangibles. Proper allocation in these categories may not be adequately met and this may result in falsely accounted balances and harsher audit due to a regulatory inspection.

The entities should conduct step-zero qualitative tests or procede to quantitative goodwill impairment tests according to ASC 350 upon purchase.

Reporting Requirements and Financial Statement Impact

Once recorded, intangible assets are presented on the balance sheet under non-current assets. The related amortization and impairment expenses are included in the income statement.

Disclosures under ASC 350 are also critical. Financial statements must provide:

- Carrying amount of intangible assets, gross and minus accumulated amortization

- The amortization cost of the period

- The weighted-average amortization period in place

- Information on the impairment losses, in case there are some

- Qualitative disclosures of indefinite-lived assets

A company with intangible assets should provide clear disclosures so that investors and analysts know what the intangible assets entail and the amount of risk that is involved in these assets, which also supports decisions on how to analyse a company performance using financial statements.

Practical Challenges in Implementation

There are a number of practical difficulties in accounting of the intangible assets under ASC 350 even though it seems to have clear papers:

- Complex valuations: Unusual intangible assets may have complicated values that may demand specialized experience.

- Subjectivity in useful life: The anticipated number of periods or years of usefulness of finite-lived assets is judgmental.

- Hard to capture all assets: All assets cannot be identified and some of the intangibles can be knit deep in operations and not easily isolated.

- Shifting market conditions: Any of the factors that affect impairment test-market share or protection under the law to name just two-can vary dramatically over time.

- Cost of compliance: Evaluating the participation of valuation companies and preparation of documents may be resource-intensive to the medium size companies.

The companies have to undertake internal control measures, use cross-functional teams, and have comprehensive records to impress the auditors and regulators.

How ASC 350 Aligns with Strategic Planning

ASC 350 is not only an obligation on compliance, but also has links to wider strategic and financial planning. Learning the importance of intangible assets aids the management in making proper decisions concerning allocation of capital, mergers and acquisition, divestitures, and investment in the brand.

Also, the debt covenants, tax planning, and executive payouts based on earnings measures may be impacted by impairment charges as well as amortization schemes.

The treatment of intangibles is a growing concern to investors and the stake of an enterprise, in particular, since resulting value stands to comprise the majority of enterprise value in advanced, knowledge-based businesses.

Conclusion: A Framework for Long-Term Clarity

Intangible assets that have been acquired need to be properly accounted for so that a fair picture of the worth of a company is portrayed. ASC 350 provides feature guidance that ensures existence, measurement, amortization and impairment of these assets with the aim of measuring their actual economic benefit reporting in the financial statements.

Although the regulations can be burdensome especially when related to valuation and filing and compliance, compliance gives rise to a strategic advantage. It increases the area of transparency, investor buoyancy, and also provides companies with chances in audit preparedness and further capital deals.

Whether you are purchasing a tech startup with rich intellectual property or combining with another consumer company heavy with brand, ASC 350 will ensure the post acquisition balance sheet shows all that has been acquired not just the bricks and mortar.