Improving IFRS for Intangibles Recognition and Valuation

Learn Improving IFRS for Intangibles Recognition and Valuation

In the contemporary economy, the importance of intangible assets is growing-brands, customer relations, intellectual property, proprietary technology, and goodwill. Nevertheless, the International Financial Reporting Standards (IFRS) continue to fail to capture the actual representations in the stated economic value of these assets in business financial reports. The generally used IFRS especially IAS 38 and IFRS 3 have a limited recognition and measurement scope and hence can easily produce financial reports that are a source of misrepresenting the actual value of a company.

With changes occurring in the business scenario the reintroduction on the treatment of intangibles by IFRS is eminent. The paper discusses the shortcomings of the existing IFRS guidance, the arguments of the case of fair value measure and the possibility that an increased disclosure might act as a compromise.

The Importance of Intangibles in Today’s Economy

The proportion of intangible assets relative to the total corporate value in the world has increased over the last twenty years. Intangible assets in the form of enterprise value greater than 80 percent of intangible assets are found in technology, pharmaceutical and service businesses. The changes in this evolution have not been addressed in the financial reporting standards, however.

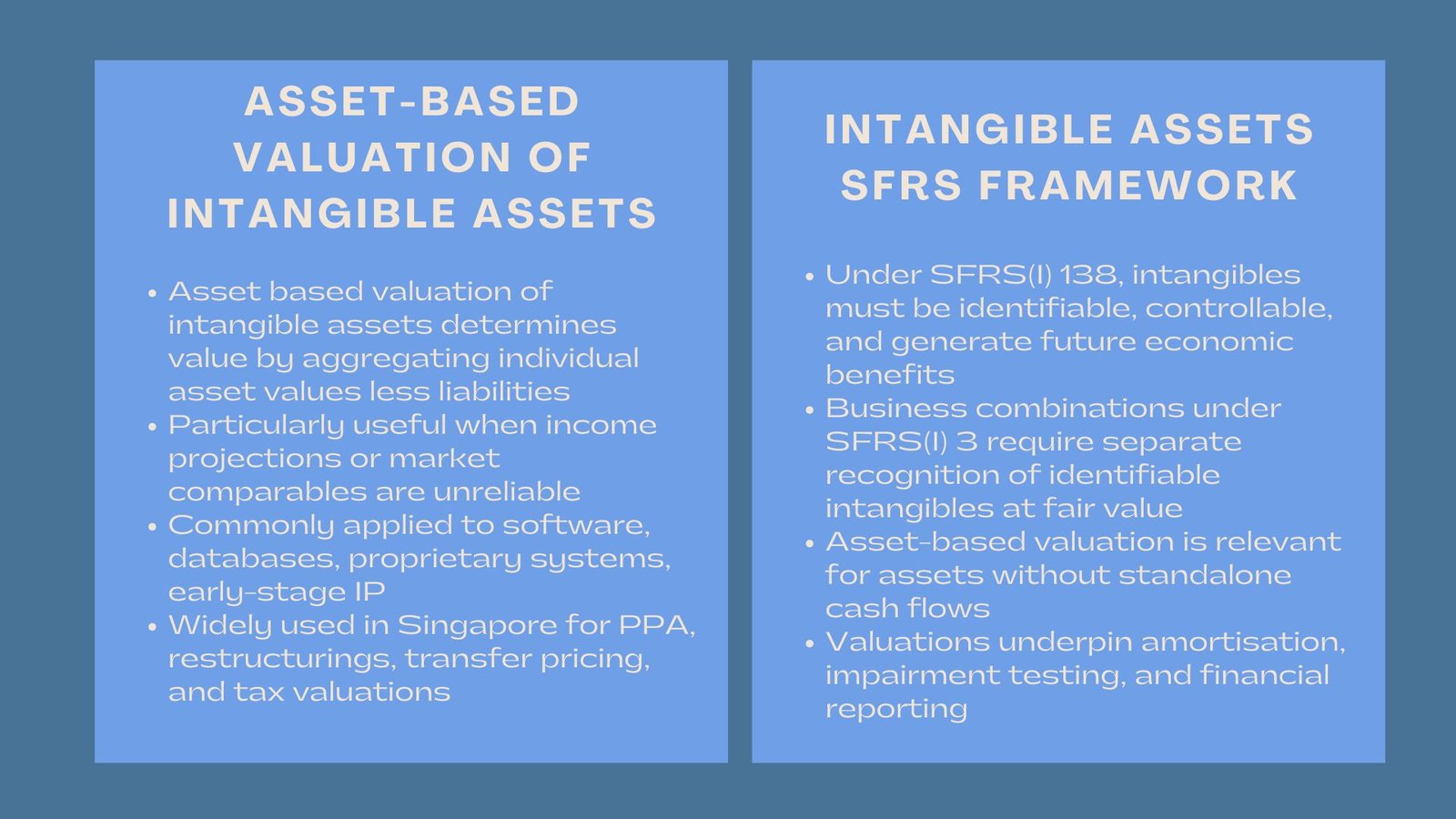

The current IFRS does not require the recognition of internally generated intangible assets in the balance sheet with the exception of strict criteria being met. When they are identified, they are usually not transparent and comparable, their calculation methods, in particular, and the assumptions are likely to be non-transparent and non-comparable even in the case of purchased intangibles through business combinations.

For companies exploring how to do valuation of an accounting business Singapore, or seeking clarity on economic profit vs accounting profit explained Singapore, these issues highlight the growing importance of intangible valuation and business valuation Singapore in financial reporting. This gap forms an asymmetry of information between the management team and the stakeholders, especially the investors and analysts who determine the value of an enterprise, its risk, and their possible returns based on financial statements.

Limitations of Current IFRS Guidance

Two main standards that concern intangibles are IAS 38 Intangible Assets and IFRS 3 Business Combinations. Nonetheless, each has severe limitations to its applicability with regard to the modern setting:

- Internally generated intangibles: Even expenditures on most research and brand development are expensed as opposed to capitalized, even though they have long-term value.

- Recognition thresholds: Intangibles are required to be identifiable, controllable and measurable in order to qualify to be entered in the balance sheet. A lot of good but inseparable assets do not pass the test: assembled workforce, corporate culture, etc.

- Amortization vs. impairment: Finite-lived intangibles must be amortized and indefinite-lived intangibles presumably must be impaired tested annually. This would distort earnings and balance sheets in the event that there is not a capture of fair value changes in real time.

- Post-acquisition treatment: A lot of intangible assets that are included in a business combination are carried at amortized costs once they have been identified and lose relevance as business circumstances shift.

The net-effect of this is that intangibles heavy companies may appear underpriced when it comes to financial statements, a fact that makes investment decisions and corporate governance problematic.

The Case for Fair Value Measurement

One of the solutions suggested has been to change the measurement basis of intangible assets, to reassess their fair value as opposed to using cost basis. This would make the accounting treatment more inline with economic realities of businesses, especially of high-growth/IP-intensive sectors.

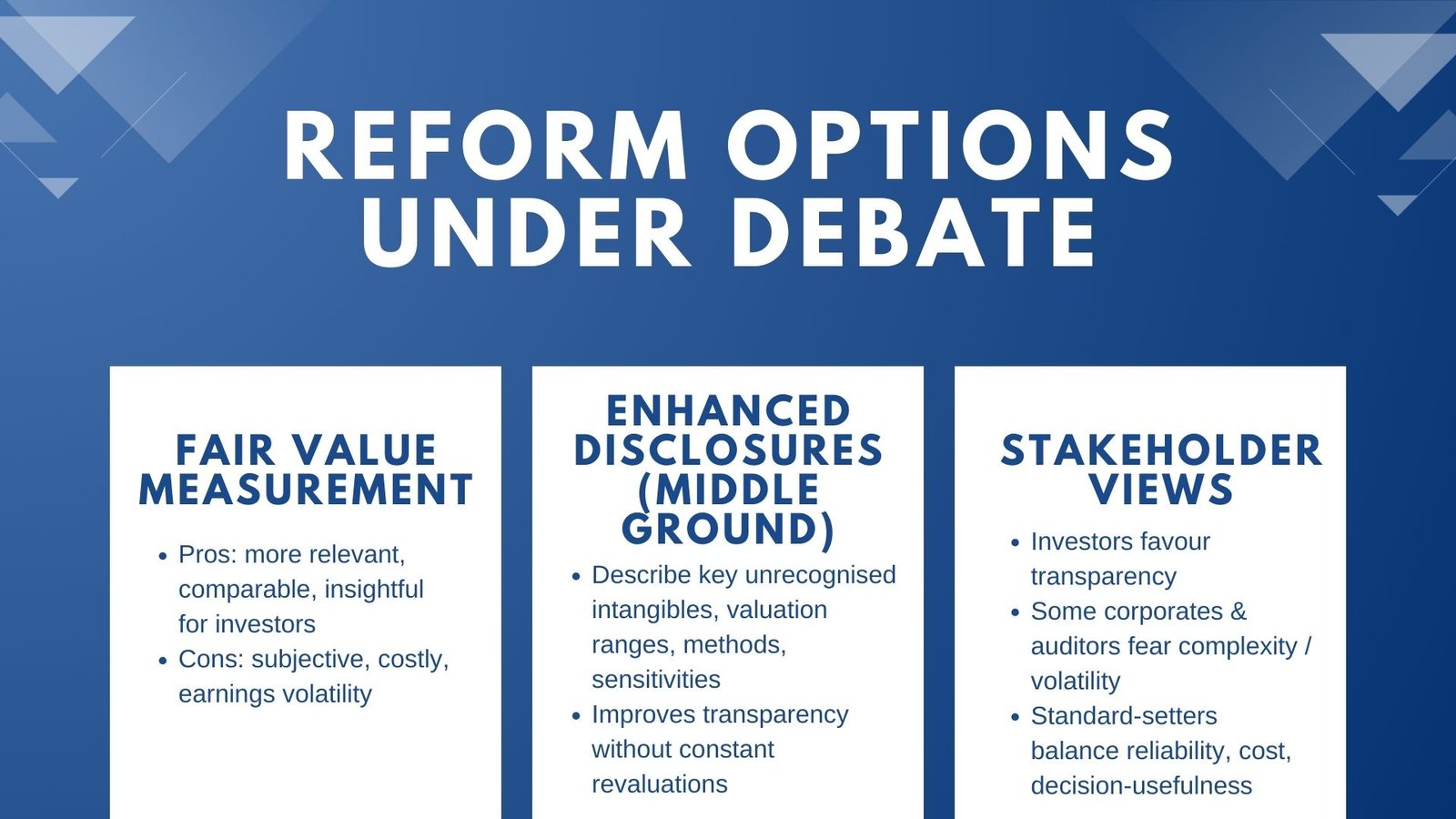

Advantages of fair value accounting for intangibles include:

- Improved relevance: The financial reports would show current conditions of the market thereby increasing the usefulness of reported figures on a decision-making level.

- Comparability: Cross-company and cross-industry comparisons can be more meaningfully made when similar intangible assets are measured by application of the same fair value techniques (e.g. an income or market approach).

- Investment insights: Fair value disclosures also assist investors to have a better understanding of the potential and future performance of a given company.

However, fair value measurement also brings concerns:

- Subjectivity: Intangible valuation is by its nature judgmental. Lack of a strong guidance can lead to risks of inconsistency and manipulation.

- Cost and complexity: Reoccurring revaluation of the intangible assets may require a lot of resources, particularly on SMEs.

- Volatility: The recognition of fair value changes as a profit or loss may aggravate the earnings volatility, something that may not be desirable by some stakeholders.

IFRS 13, which gives the framework of fair value measurement, has not been developed and applied to measure intangibles sufficiently. At the present, the companies are left to choose whether to conduct the revaluations that are to be disclosed on periodic basis or to employ the fair value model under limited circumstances where these models are permitted.

Enhanced Disclosure: A Middle Ground?

Of the drawbacks and disadvantages of accounting full fair value adoption, a few practitioners argue that full fair value recognition should be accompanied by an increased amount of disclosure as a realistic middle ground. Instead of acknowledging recognition or fair value reporting, firms may give specific disclosures of internally-generated intangibles, valuation procedures and the strategic significance.

Examples of such disclosures may include:

- Description of significant intangibles not recognized on the balance sheet

- Management estimates of fair value ranges

- Valuation techniques used, including key assumptions and sensitivities

- Strategic importance of certain assets in driving future performance

The method has benefits in that it enhances the transparency and enables the stakeholders to have a better judgment; it does not overwork the companies requiring regular revaluation or restructuring of the existing systems. Nevertheless, due to the commonly occurring conditions of disclosures being both not audited and voluntary, it should nonetheless not hold the same degree of recognition as that accorded to financial statements.

Stakeholder Perspectives on IFRS Reform

Calls for reform are growing louder from various quarters of the financial ecosystem:

- Investors and analysts desire more transparency in the intangible resources in order to make informed judgments regarding the ability of the companies and their value as well as risk.

- The treatment of intangibles is an area that is the focus of standard-setters like the IASB, though few steps forward are being made as other priorities are overriding those of the treatment of intangibles and opposition is witnessed by organizations and industry players.

- There are splits within the corporates in that some will argue in favor of more recognition and fair value but others fear complexity and volatility.

- Auditors and the regulators attempt to ensure that the credibility of financial statements is maintained, that they are consistent and comparable; therefore, they are reluctant to change important things.

The ideal solution will likely balance transparency, reliability, and cost-effectiveness, while ensuring that reported figures remain decision-useful in a variety of business contexts.

What the Future Might Hold

Several possible directions are emerging in the international debate on improving IFRS for intangibles:

- Broader improvement criteria: More internally generated intangibles to be capitalized under particular circumstances (e.g. can be proven as having economic benefit).

- Optional fair value revaluation model: Companies would be permitted to adopt the fair value model on selected classes of intangibles and even on intangibles in general, as they are doing in the property, plant and equipment the case of IAS 16.

- Industry specific advice: Differing industries can be supplied with industry specific rules, due to the fact that in various industries intangible properties are highly different.

- Mandatory disclosure frameworks: Imposing standardised templates or requiring disclosure of the intangible assets in notes to the financial statements.

- Connection with sustainability and ESG reporting: With non-financial reporting gaining popularity, intangibilities such as brand, reputation and innovation can find expression in broader forms of reporting than the traditional financial statements.

Each path carries trade-offs, but they all aim to close the gap between reported figures and economic reality.

Conclusion: Improving IFRS for Intangibles Recognition and Valuation

Intangible assets could use some changes in their treatment in IFRS. As intangibles now make up the spinal column of value creation in the knowledge economy, this situation hinders practical applicability of financial statements in a particular way. Although the full fair value adoption is not simple and quite controversial, a mixed approach to increased recognition, optional fair value testing, and disclosures observations might be the best we can do.

The various stakeholders, including preparers and auditors, as well as investors and regulators, should work together so that any reforms can bring significant changes that will not pose any excessive burden or risk. Revising IFRS intangibles is not a technical matter, but what a financial reporting framework should do to better reflect the sources of value in today’s business.