Understanding What is the Difference Between Tangible and Intangible Assets

It is imperative to comprehend the difference between tangible and intangible assets as a businessperson, investor and financial analyst. Assets form a fundamental aspect of the balance sheet and valuation of any company and identifying how such assets should be addressed in an accounting context as well as the business strategy is fundamental to sound decision making. In this article it will unravel the major distinctions, examples and financial ramifications of tangible and intangible assets, while also highlighting what are the best tools used in financial analysis to better evaluate their impact.

Defining Tangible Assets

Tangible resources are those physical resources that are measurable with specific value and can be felt, relocated as well as utilized in day to day activities. These are the type of assets that companies rely on to create production of goods or services, aid in their operations and create income. Due to their physical nature, Tangible assets are usually simpler to price with either the market based method or the cost based pricing method.

Examples of tangible assets include:

- Buildings and real estate

- Machinery and equipment

- Vehicles

- Land

- Inventory

- Furniture and fixtures

These assets are written off over a period of time with exclusion of land which is not depreciated. Depreciation comes in handy as the process would enable firms to spread the expense of physical assets throughout its useful life to lessen taxable income and gives insight into asset value during time.

Understanding Intangible Assets

On the other hand, intangible are non-physical. They constitute fixed rights, intellectual rights or brand value that add towards the long term competitiveness or revenue generating power of a firm. Intangible assets may be intangible but in many cases, they may be very valuable especially in knowledge based and digital economy.

Common examples of intangible assets include:

- Trademarks and trade names

- Patents

- Copyrights

- Customer relationships

- Goodwill

- Software

- Licenses and permits

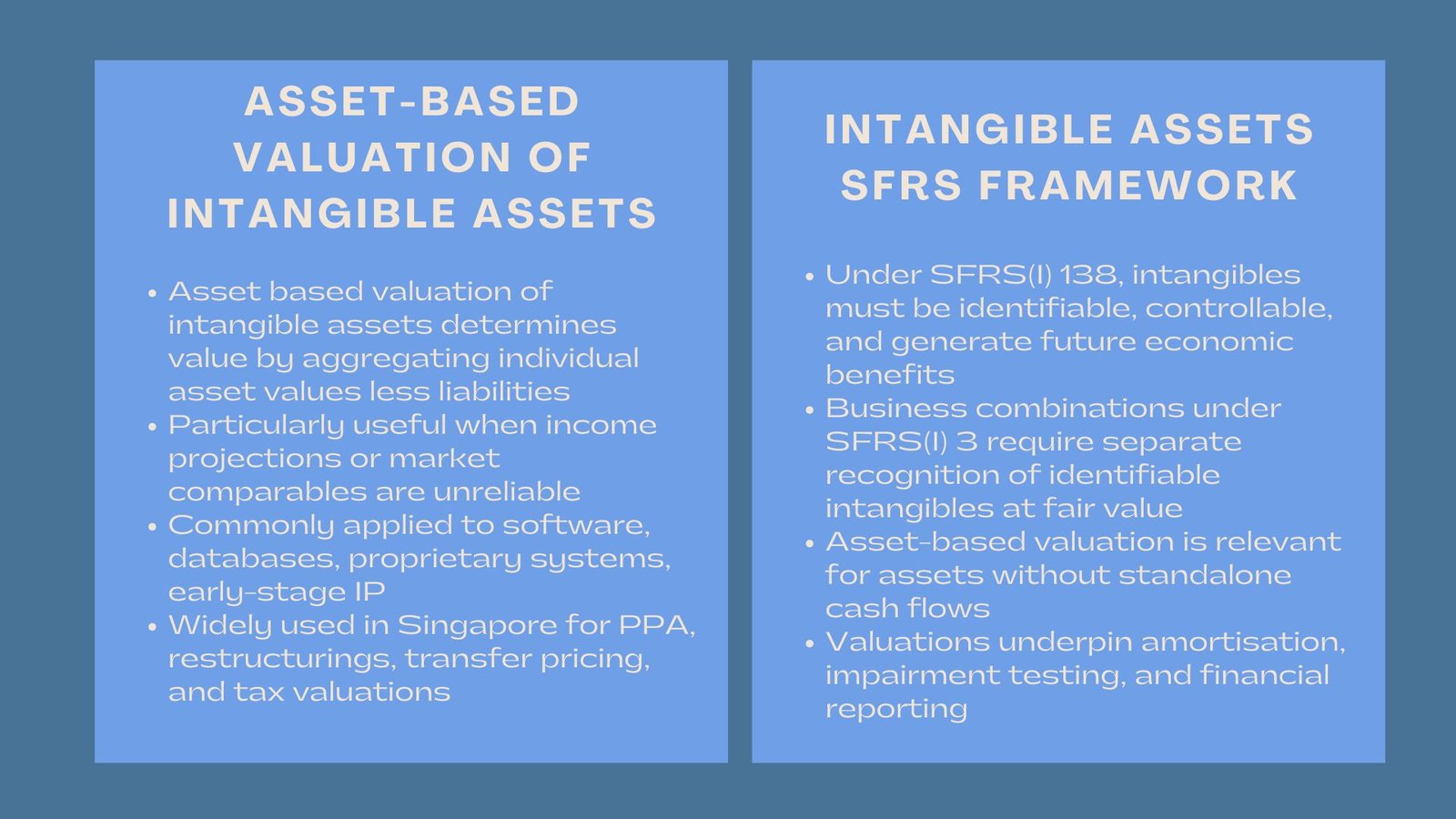

Compared with tangible assets, intangible assets are either amortized during their useful life or (where they are of indefinite life, as in the case of goodwill), annually tested to ensure that they are not impaired. Intangibles are more difficult to identify, measure, and verify and as such, accounting and valuation of the same are more complicated. For businesses seeking guidance on how to value intangible assets in Singapore, professional support from intangible asset valuation consultants in Singapore can provide clarity and accuracy in the process.

Key Differences Between Tangible and Intangible Assets

Physical Form and Perception

The most apparent distinction is that tangible assets are seen tangible and eliminated. Intangible ones are not. This does not just affect their use but also their perception and comprehension by the investors and stakeholders. The existence of tangible resources usually gives security since it is assured that the assets could be liquidated, but the intangible ones might seem ambiguous or risky to pursue unless their worth is made specific.

Measurement and Valuation

Tangible assets may usually be measured according to the market price, depreciated value or replacement cost. Comparables are normally available since they have physical presence and are in most cases purchased or sold in open markets. Intangible assets are usually more difficult to value professionally, and valuation methods may include the income, market or cost approaches to value a particular asset (see discounted cash flow from future benefits, comparable transactions approach, or cost of recreation approach).

Accounting Treatment

From a financial reporting standpoint, tangible and intangible assets are treated differently:

- Tangible assets suffer wear and tear and are booked under property, plant and equipment (PPE) in the balance sheet.

- Intangibles can be carried in an amortization schedule over an estimated useful life, or can be tested annually for impairment (indefinite-lived). Most accounting rules, including IFRS and US GAAP, do not recognize the capitalization of internally developed intangibles (experience gains such as internally generated brand equity).

Legal Rights and Ownership

Real resources carry with them definite rights to ownership and ease of transfer or mortgage. Intangible resources cannot be given physical protection; thus they are hard to protect in terms of law, and in most cases, legalization should only be one patent, copyright, or license agreement. Their value may be neutralized by lack of clarity or enforceability concerning ownership, unless care is taken.

Business Implications

Asset-Based Lending and Collateral

Physical assets are usual security arsenals to loans and financing. Lenders and banks are more inclined to issue loans that would be secured by realty, machines or stock. Conversely, intangible assets are more difficult to use as collateral, but may represent a large part of the total value of that particular company, at least, in tech, pharmaceutical and media sectors.

Strategic Value

Many times intangible assets are more strategic than tangible ones. Think of the trademark of a world organization such as Apple or Coca-Cola. The brand, design, and customer loyalty are the most valued aspects of the company as they propel high prices and market dominance, although the physical factories and machines also have value. In such a way, the value of a patent portfolio in a pharmaceutical company can reach billions, though the gear is not impressive.

Post-Merger Valuation and Integration

Accounting rules like IFRS 3 and the ASC 805 apply Purchase Price allocation (IPA) to the tangible and the intangible assets during the mergers and acquisitions. Here the difference starts to be of more importance. A considerable portion of the purchase price could be divided up among intangible assets such as customer relationship, trade names, or technology and all such intangibles that are supposed to be valued independently and then amortized or checked separately based on possible loss or impairment.

Tax Considerations

There is a tremendous difference in the tax lines between tangible and intangible assets. The depreciation of actual assets could be claimed yearly and lower the revenue. On the same note, it is also a form of tax deduction when intangible assets such as some or all of brand value are amortised (depending on whether tax authorities permit deductions in this regard). The deductibility of a goodwill impairment or amortization, however, varies in many cases depending on jurisdiction and is bound to several restrictions.

Challenges in Managing Intangible Assets

Whereas physical property is quite easy to deal with and take care of, intangible property is complicated in its own ways:

- Identification: Most companies find it hard to identify all their intangibles assets, particularly, when they were internally developed.

- Legal Protection: To ensure that patents, trademarks and copyrights are sufficient it is necessary to defend them actively.

- Volatility in Valuation: The valuation of intangible assets may change significantly and at a short pace owing to the market circumstances, lawsuits, or obsolescence.

- Impairment Risk: the intangible assets are more likely to incur a charge due to impairment charges unlike the tangible assets when future cash flows are not satisfying.

The Growing Role of Intangible Assets in Modern Business

With the digital and knowledge-intensive economy creating plenty of sustainable competitive advantages, asset intangibility contributes more to the firm value than it has ever been. It is not uncommon to come across startups or even technology giants that have very little in physical assets to show yet may be highly valued in the stock market due to intangibles like intellectual property, user base or internal algorithms. The role of these assets in value is essential knowledge to contemporary investors and executives.

Investors are also assuming various forms of adjusted valuation approaches to capture the incremental prominence of the intangible capital. This comprises intellectual property valuation, brand valuation as well as data monetization framework. Regulators also are modifying standards (such as the BEPS initiatives and transfer pricing guidelines of the OECD) in an attempt to capture the value of intangibles in international transactions.

Conclusion

Physical presence is not the only distinction between tangible and intangible assets; it implies the manner in which value is generated, safeguarded and appreciated in the corporate environment. Although tangible assets are easier to measure as they provide concrete value, intangible assets can be the answer to long term growth, strategic advantage and market differentiation.

To business, both categories are critical in controlling their balance sheet, raising finances, formulating tax plans, and in case of merging or acquisition. Investors and analysts view the prospect of evaluating and measuring the intangible assets as a better way of seeing the real value of a company.

With the increasing role of intangibles in the creation of value and the development of economies, correct determination of the value of both tangible and intangible assets will continue to be one of the pillars in good financial management and strategic planning.