Valuing Goodwill and Intangible Assets

The purchase price which is reported as the headline in nearly all major mergers or acquisitions is more than the fair value of identifiable net assets of the target company. That distance, which can be small, but is so frequently vast, is goodwill. Beside the goodwill are a group of intangible assets; customer relationships, proprietary technology, brand names, non-competence agreements, licences, and so forth. These items combined may comprise most of what an acquirer is actually purchasing, but they are also one of the most technically challenging items to estimate in any deal. To the first-time finance practitioner, the principles and techniques of goodwill and intangible valuation of assets are not something to memorize and trickle down to their subordinates; they are essential.

The topic has become significant due to the change of business models whereby physical capital is no longer the basis of business models but knowledge, relationships and intellectual property. The pharmaceutical company drug pipeline, the software company codebase, the consumer brand loyalty, these are the assets that create value in the contemporary business but they are so far off the balance sheet that they are only made visible when a deal takes place. The accounting standards including IFRS 3 and ASC 805 stipulate that when a transaction is completed, the acquirers have to identify intangible asset valuation techniques, through recognised methods of valuing intangible assets. The left over that cannot be traced to any particular asset or liability is then considered as goodwill.

The article is aimed at an analysts and associates and finance managers involved in or preparing to be involved in goodwill valuation in a merger and acquisition, business combination or impairment testing. It discusses the conceptual difference between goodwill and other intangibles, these are the main valuation methodologies of practice, a purchase price allocation exercise process, the issues that practitioners face most frequently and the lessons learned by experienced practitioners in the field. It ends with a list of practical implications that every practitioner may use to enhance the quality and defensibility of his or her intangible asset analyses.

Understanding the Distinction Between Goodwill and Identifiable Intangibles

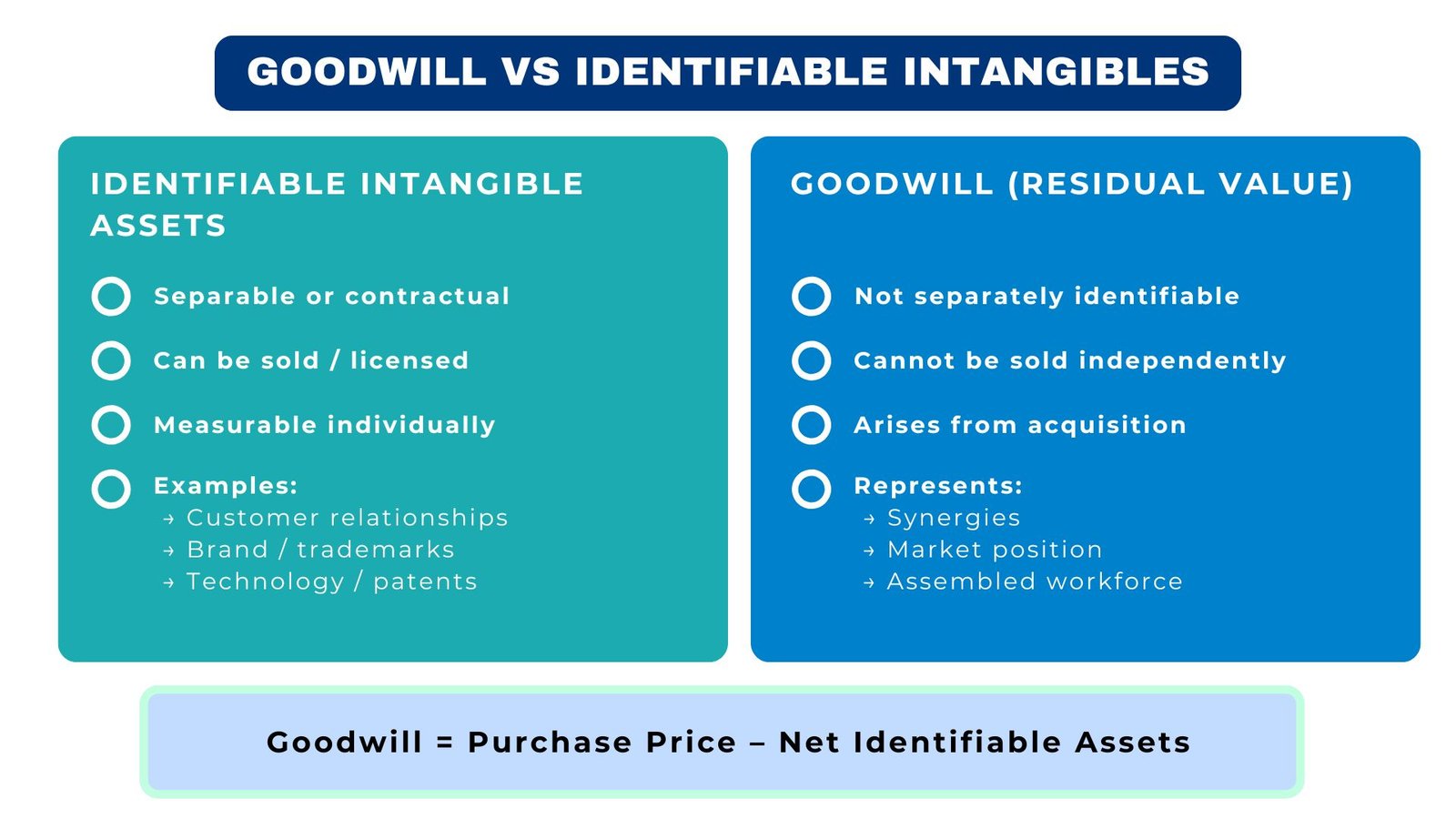

It is first necessary to know what goodwill is before any valuation can commence, and, of paramount importance, what it is not. A lot of junior practitioners confuse the goodwill with the general premium in a deal and therefore, this is oversimplified. Under the IFRS 3 and the US GAAP counterpart, the goodwill is the remaining consideration given, once the fair values of all identifiable assets to be acquired; and liabilities to be assumed have been taken away. The identifiable intangible assets, in their turn, have to pass certain requirements: they have to be either separable (that is, they can be sold, licensed, or transferred as a separate entity) or be a result of a contractual or legal right. This difference is not just a matter of academia – it is the motivating force behind the whole process of purchase price allocation (PPA) exercise.

Under the IFRS and the US GAAP, identifiable intangibles are generally divided into five categories, which are marketing-related (brand names, trademarks), customer-related (customer lists, relationship assets), artistic-related (copyrights, media content), contract-based (favourable leases, licensing agreements), and technology-based (patents, software, trade secrets). All the categories have various economic features, useful life, and relevant intangible assets valuation methods. An asset of customer relationship of a B2B industrial supplier, such as that, will be valued quite differently than a brand asset of a fast-moving consumer goods company, although both of them are under the same accounting regulation as identifiable intangibles.

Goodwill, in its turn, is all that cannot be singled out: the accumulated workforce, the synergies that will be achieved through the combination, the going concern premium, the advantage of the market position of the company acquired, and any other value contained in the business in general. Due to the nature of goodwill being a residual, the amount of goodwill is directly as a result of the quality and completeness of the process applied to recognize and measure the underlying intangibles. This is what goodwill and intangible asset valuation are so significant about, however, an undervalued relationship with a customer or a forgotten technology asset is not a vacuum it will burst goodwill and result in an asset that will be later tested on the annual impairment test.

Table 1: Important Categories of Identifiable Intangible Assets

| Category | Examples | Common Valuation Method | Typical Useful Life |

| Marketing-related | Brand names, trade names, trade dress. | Relief-from-Royalty | Indefinite or 10–20 years |

| Customer-related | Customer databases, customer relationship, backlog. | Multi-Period Excess Earnings | 5–15 years |

| Technology-based | Software, trade secrets, patents. | Relief-from-Royalty / Cost | 3–10 years |

| Contract-based | Leases, licences, franchise rights are favourable. | Income Approach (direct) | Contract term |

| Artistic-related | Copyrights, media archives, content storage. | Income Approach (royalty) | Life of the law or economics. |

The Principal Intangible Asset Valuation Techniques

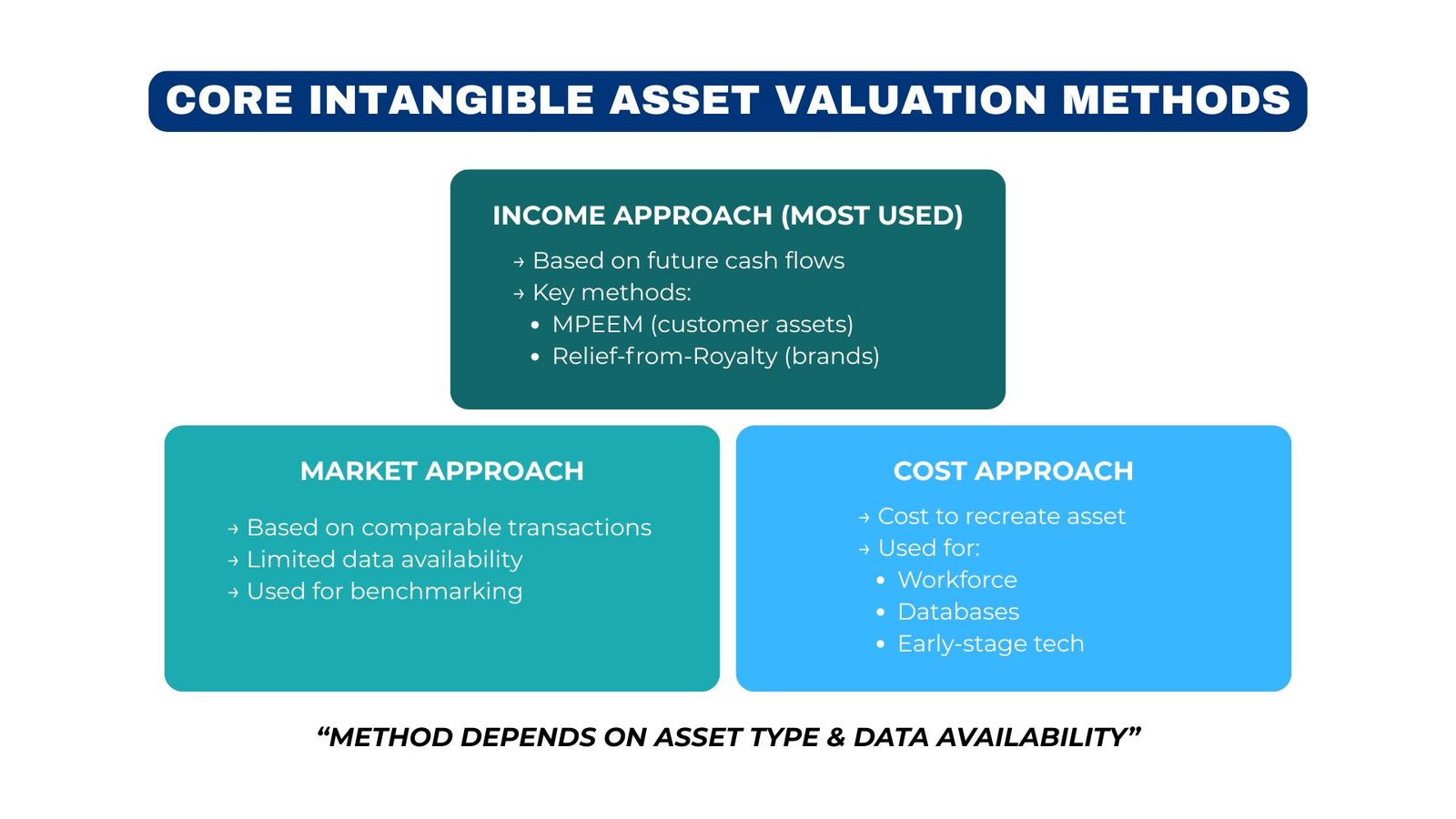

The three main methods that are applied in the valuation of the goodwill and intangible assets are the income method, the market method and the cost method. Practically, the intangible asset work is overtaken by the income approach since most intangibles are valued on the basis of their ability to provide economic benefits cash flows, cost savings, or higher prices in the long term. The Multi-Period Excess Earnings Method (MPEEM) and the Relief-from-Royalty Method (RFR) are the two most popular intangible asset valuation techniques based on income that are used by the practitioners. They all have logic, data requirements and spheres of its proper application.

The MPEEM is normally used on the major intangible asset of the business which is acquired, that is the asset that produces the largest percentage of the revenues of the company. It operates by projecting the cash flows which can be ascribed to the intangible which has been adjusted by the contributory asset charges (CACs) which indicates the cost of all other assets necessary to bring the revenues. The resulting excess earnings are then discounted back to present value at a rate that is a reflection of the risk that the intangible is subjected to. A common case in point: an acquisition of a European industrial automation firm by a US-traded strategic buyer, the long-term relationships with the customers of the target were declared the highest-ranking intangible. The MPEEM was put in place with the use of a five year projection of the customer revenues with the adjustment of the anticipated rates of attrition based on historical data and discounted at a rate reflective of the contractual stability of such relationships.

Compared to it, RFR method is more appropriate in case of brand names, patents and proprietary technology – assets and which in theory can be licensed to third party. In the method, the royalty rate that one of the market participants would pay to use the intangible is estimated and the rate is applied to the estimated revenues that the asset can generate, and the savings on the royalty payments are then discounted to present value. The market method of applying observable transactions of similar intangibles is not often applied in PPA work because of the lack of data, but is sometimes employed to support the conclusions of RFR on well-known brand groups. The most suitable method is the cost approach that approximates the cost to replace the asset, this applies best in workforce-in-place, proprietary databases or assembled technology where the income-based methods cannot be applied. The choice of the appropriate method is also one of the most significant ones in the goodwill valuation in mergers and acquisitions, and the given decision should always be clearly explained in any valuation report.

Process Flow 1: The Right Intangible Asset Valuation Method.

| Step | Question to Answer | If Yes | If No |

| 1 | Are the separate identifiable cash flows of the asset? | Take into consideration income approach (MPEEM). | Proceed to Step 2 |

| 2 | Is it possible to license the asset to a third party and at a market rate? | Apply Relief-from-Royalty method | Proceed to Step 3 |

| 3 | Is there similar similar transaction that is observable in the market? | Consider market approach | Proceed to Step 4 |

| 4 | Is the asset replicable by way of development or acquisition? | Apply cost approach | Consult specialist- could be residual/goodwill. |

| 5 | Are there a number of approaches? | This is triangulation and rationale documentation. | Choose one of the best methods and explain why. |

The Purchase Price Allocation Process: Five Essential Steps

The formal process of assigning the entire consideration paid by an acquirer on the identifiable assets and liabilities of the acquired business is called a purchase price allocation, the excess of which is called goodwill. This has to be done as mandated by accounting standards and normally by a special team of valuers, either an in-house or an outsourced team, during the measurement period after the close of deals. In the case of practitioners who are new to this process, the following five steps will give them a guideline on how to go about a PPA exercise in a disciplined and rigorous manner. These steps contain extreme technical judgment, and each of them stipulates what will be put in the balance sheet of the acquirer as goodwill upon acquisition.Identify the amount of consideration that has been transferred.

- Determine the total consideration transferred. It entails the actual cash purchase price, deferred or contingent consideration (earn-outs) issued, and shares issued and any property assumed liabilities that constitute part of the economics of the deal. The consideration passed determines the limit within which all the assets and liabilities identified should be gauged.2. Recognize and list all the intangible assets.

- Identify and catalogue all intangible assets. At the same time as the deal team, legal counsel and management of the business being acquired, the valuation specialist determines all the potentially separable or contractual intangibles. This action involves intensive involvement in the business model, the way the business makes money, how the company keeps customers and how the company has created its competitive advantage.3. use relevant methods of valuing the assets.

- Apply appropriate valuation techniques to each asset. Depicting the selection frame in the foregoing section, attempt the most suitable of the recognised techniques of valuing intangible assets to each of the identified assets. This process will involve financial modelling, market research and discount rates that are indicative of the risk profile of each particular asset.4. Establish the fair value of the tangible assets and liabilities.

- Determine the fair value of tangible assets and liabilities. The physical assets, property, equipment and inventory should also be carried at fair value as at the date of acquisition of the asset. The values are directly inputted into the PPA equation and influence the balance of goodwill left

- Calculate and sense-check goodwill. Goodwill, = total consideration less the amount of all the identified net assets, at fair value. A sense-check at this point is to evaluate the economic rationale of the resulting goodwill, is it in line with what can be identified as synergies, assembled workforce value or even market-premiums? In case goodwill is too large in relation to the rationale of the deal, it is an indicator that one or more intangibles have been underpriced.

Challenges in Practice and Lessons from the Field

The seasoned practitioners in the field of goodwill and intangible asset valuation are always pointing out three classes of difficulty which include data constraints, judgement decisions on useful life, and management of audit and regulatory examinations. All are real-life challenges of operations, and all have provided lessons of the profession which the beginner professional can gain more through knowing before experience first presents it to him.

The most pressing problem is possibly data restrictions. The intangible asset valuation techniques which are income based MPEEM and RFR are highly sensitive to the quality of the inputs. Revenues projected, the rate of customer attritions, royalty rate, and discount rate will all demand either company-specific data or market data, and both of them may not be easy to acquire. Within the acquisition of one of the Australian mid-sized healthcare technology companies by a pan-Asian strategic group, the valuation team discovered that the history of customer attrition had never been systematically monitored historically. Instead of making a generic assumption, the team collaborated with the sales management of the target to recreate four years of attrition data of the CRM records and contract files. This rebuilding endeavor gave two weeks to the project schedule, however, generated a much more justifiable customer relationship worthiness- and eventually minimized the threat of post-close audit challenge.

Another aspect of recurrent difficulty in goodwill valuation in mergers/ acquisitions is the assigning of useful lives to intangible assets. The accounting standards dictate that finite-lived intangibles should be amortised over the useful economic life whereas under IFRS, indefinite-lived intangibles (and the goodwill itself) are to be tested annually. This useful life that is attributed has an impact on the trend of post-acquisition earnings and the current risk of impairment. A five-year life asset allocating a technology asset shall be written off before a ten-year life asset will result in a highly varied earnings profile of the acquirer. The incentive to impairment risk of assigning shorter life and longer life to the asset (longer life will have less amortisation charges at the start of the period) is something that auditors and standard-setters are very conscious of and hence practitioners should be ready to support their useful life assumptions with stringent market evidence and company-specific data. In one of the most remarkable instances of acquiring a German automotive software provider, the acquiring group first put a life span of ten years on the core software platform. The audit team was obligated in the course of audit to show that the comparable software assets in the industry had a life expectancy of over seven years, which, as it turned out, they could not, in the case of the most technology-specific elements. The life was recalculated downwards on those assets, and it had a significant influence on post-acquisition earnings per share.

Table 2: Common Challenges in Intangible Asset Valuation and How to Address Them

| Challenge | Root Cause | Practical Solution |

| Absence of historical data of attrition. | Target failed to monitor the churn of the customers in a systemic manner. | Build up out of CRM / contract records; exploit industry benchmarks with reservations. |

| Setting up of the right royalty rates. | Little publice licensing transactions data. | Cross-check with internal transfer pricing Use royalty rate databases (RoyaltyStat, ktMINE); |

| The defence of useful life assumptions. | Scutiny and audit subjectivity. | Prepare evidence in the market; look at what competitors reveal and research in the industry. |

| Contributory assets allocation in MPEEM. | There are several assets that are contributing to cash flows. | Apply WACC decomposition; make sure that CAC rates are internally consistent. |

| Dealing with earn-out contingent consideration. | Payments in future, that are based on performance levels. | Model probability-weighted scenarios; update fair value at each reporting date |

Process Flow 2: Purchase Price Allocation Timeline and Responsibilities

| Phase | Timing (Post-Close) | Activity | Responsible Party |

| Initiation | Week 1–2 | Recruit PPA valuation expert; get deal documents and model. | CFO / Corporate Development |

| Asset Identification | Week 2–4 | Interview management map business model catalogue all intangibles. | Valuation Specialist + Legal |

| Data Collection | Week 3–6 | Collected financial estimates, client information, IP records, market information. | Finance Team + Specialist |

| Valuation Modelling | Week 5–10 | Establish income models of each intangible; discount; sense-check goodwill. | Valuation Specialist |

| Draft Report | Week 10–14 | Prepare PPA report; include assumptions; present to the management. | Valuation Specialist + CFO |

| Audit Review | Week 14–20 | Answer auditor questions; update assumptions (where necessary); complete values. | Finance Team + Auditors |

| Finalisation | Within 12 months | Final PPA to record on balance sheet; to prepare amortisation schedules; to record to impairment testing. | Finance / Accounting Team |

Goodwill Impairment: The Ongoing Valuation Obligation

Valuation of goodwill and a work of intangible assets does not conclude as soon as a PPA is signed and the accounts of the transaction are closed. In both IFRS and the US GAAP, the impairment of goodwill should be tested on a periodic basis (at least once in a year) and more often in case any of the triggering events indicate that the carrying amount of goodwill will not be recovered. To IFRS reporters, this will entail comparing the carrying value of cash-generating unit (CGU) which is the smallest unit of assets that produces independent cash flows to its recoverable amount, which refers to the fair value less costs of disposal and value in use. In the case of reporters of US GAAP reporters under the ASC 350, it entails the generation of a comparison between the carrying value and the fair value of a reporting unit with any surplus being known as impairment loss.

The implications of the practice are crucial. The goodwill that was reported when a purchase was made under optimistic assumptions is currently under the annual review as per the current market developments and new financial projections. The balance of goodwill can be threatened in case the business that is purchased performs poorly during the initial years of the deal as is the case with most acquired businesses. This is exactly what is meant by the fact that the quality of goodwill valuation in mergers and acquisitions at the point of acquisition, is so crucial to the long-term financial reporting. The goodwill that has been incomplete identified or aggressively identified by incomplete intangible identification is not a one-time accounting issue, it is a continuing risk that should be managed, disclosed and defended to both auditors and investors as long as such goodwill continues to appear on the balance sheet.

A good example is that of the telecommunications industry. One of the European telecom giants purchased a local broadband carrier and deemed a good part of the purchase price to goodwill, as only a small number of relationship assets with customers and a small technology platform were identified. The cash flows of the business were materially impacted in three years as a result of accelerating the customer churn and competitive pricing pressure. The impairment test showed that the recoverable amount of the CGU was significantly less than the carrying amount, and the group had to charge off more than EUR 400 million of goodwill a charge which provoked great shareholder concern and a regulatory investigation into the original reason of acquiring the company. A more stringent use of intangible asset valuation methods at the deal time – reflecting a greater value of customer relationship, which would have been amortised, would have decreased the balance of goodwill and, perhaps, the ultimate impairment.

Conclusion: Implications to Practitioners.

The valuation of goodwill and intangibles is among the most intellectually challenging undertakings in corporate finance as it puts financial modelling together with accounting standards, market research, and business judgement into a combination that few other exercises necessitate. In case with junior and mid-level professionals developing a knowledge base in the area of goodwill and intangible assets valuation, the competence pathway is through theoretical knowledge and experience. The theoretical framework – of knowing what causes an asset to be identifiable, what causes it to have useful life and what causes the right discount rate are the key pillars. However, the practice of that framework, in live transactions using incomplete information and conflicting stakeholder pressures, is what develops true professional competence.

There are a number of practical implications of the analysis presented in this article. First, spend time in the process of asset identification – it is the most frequently squeezed part of the deal and at the same time, the quality of all the further valuations rests squarely on the ability of having the correct list of assets to value. Second, be conscious in choice of method. The three mainstream intangible asset valuation techniques, i.e. income, market, and cost, are applicable in different situations, and the selection of one of them must be based on a clear rationale, rather than on convenience. Third, develop sensitivity models of any model. The assumptions that guide intangible values, such as the rate of attrition, royalty rates, useful lives, discount rates are all uncertain in nature and giving a range of outcomes is more convincing, not less so, of a valuation.

Fourth, consider outside the deal. The values that will be determined during the goodwill valuation during the merger and acquisition will be reflected in the balance sheet, earnings, and impairment risk of the acquirer in the years to come. The imposition of aggressive useful lives or understating intangibles to reduce the amortisation in the near-term presents long-term reporting risk. A properly designed PPA which properly recognises and recognises the value of every intangible although it may increase short-term amortisation is a more justifiable, and more manageable, financial result. And fifth, keep records of all. It is more about the quality of the reasoning than the numbers in valuation. These analyses will be re-examined by auditors, regulators, and future management teams, and it is the professional who presents a clear, well-documented trail of assumptions and judgements that his/her work will stand the test of fire – and his/her professional career will also gain the reputation that goes with it.