ESG Intangible Assets Valuation

The environmental, social and governance factors have shifted firmly to the edges of the corporate strategy to the middle of investment decision making. What started as a reputational prism by asset managers who were socially conscious has become a strict analytical model that informs capital allocation, credit ratings, compliance in regulation, and in M&A due diligence. Central to this transformation is a misleadingly straightforward question: how do the results of ESG commitments of an organisation have a quantifiable economic impact? The solution, to a great extent, is to comprehend ESG intangible assets valuation, the science of identifying, calculating and reporting the monetary worth of non-physical assets that are influenced by the environmental stewardship, social capital, and quality of governance.

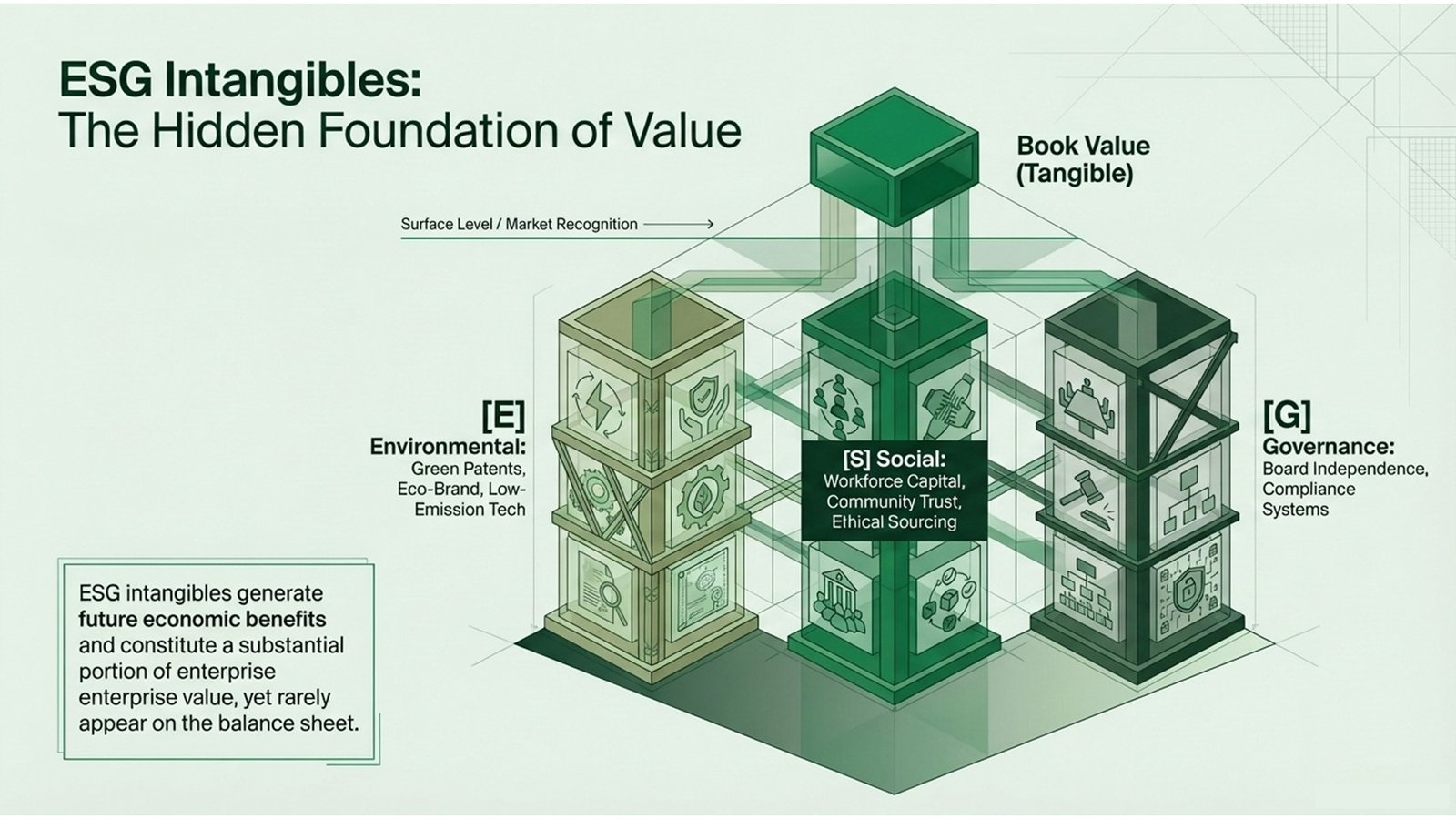

This is among the most important developing skill sets to junior and mid-level finance professionals. Intangibles with a connection to ESG, such as the green intellectual property and workforce culture, governance structures and supply-chain trust, can represent a significant part of enterprise value, but are seldom listed on the balance sheet. Even under International Financial Reporting Standards, in the traditional financial statements only a fraction of the value which advanced investors and acquirers would attribute to good ESG positioning is reflected. It is in this gap between book and market value, that ESG in corporate valuation is more of an art and a science.

This article provides a systematic discussion of the identification and valuation of ESG-related intangibles, why the significance of disclosures of intangible assets has become the strategic focus of boards and finance teams, and what procedures and tools practitioners can apply to incorporate ESG considerations into the standard valuation practice. The discussion contains real-world cases, process frameworks, and comparative tables to as much as possible turn it into a practical discussion.

What Are ESG Intangible Assets and Why Do They Matter?

An ESG intangible asset is a non-physical resource that provides economic gain to an entity in the future and the existence or value of the asset is substantially affected by the environmental, social or governance practices of the entity. This is a very general definition, and intentionally. Practically, ESG intangibles are a broad spectrum: the reputation of a pharmaceutical company on ethical clinical trials, the portfolio of carbon-capture patents of an energy company, the base of loyal customers of a retailer, who has been able to develop based on transparent supply-chain practices, or a board-level governance infrastructure of a bank that minimizes the chances of regulatory fines. All these assets do have economic substance- it affects revenue, cost, risk or growth- although none of it will be reflected as a line item on the balance sheet.

These assets have increased in importance in the economy as the institutionalisation of ESG investing has increased. As per the estimation of leading asset managers, assets under management labelled with ESG are a multi-trillion dollar sector of the international investment market today. Regulation or their own requirements demand increased disclosure on the part of institutional investors (pension funds, sovereign wealth funds and insurance companies) that ESG factors are reflected in their investment analysis. This directly puts pressure on the need to have dependable ESG intangible assets valuation, since investors cannot make any sense in integrating things they cannot measure. A company that has a good ESG reputation, but incomplete or inconsistent disclosure is a good way to leave value on the table.

The table below summarises the key categories of ESG intangible assets of all three pillars, and gives examples of them and notes about how they relate to investors. This taxonomy is the place to begin in learning to apply ESG in corporate valuation in an organized, justifiable manner.

| ESG Pillar | Intangible Asset Type | Illustrative Examples | Investor Relevance |

| Environmental (E) | Green IP & technology | Know-how in low-emission processes, carbon-capture patents. | Minimizes stranded-asset risk and regulatory risk. |

| Environmental (E) | Brand / licence value | Eco-certification, sustainability ratings | Encourages high end pricing power. |

| Social (S) | Workforce capital | Index of employee well-being, DEI programmes. | Associated with productivity and retention. |

| Social (S) | Customer relationships | Social responsibility, loyalty of sourcing. | Reduces customer-churn risk |

| Governance (G) | Organisational capital | Independence of the board, whistleblower system. | Reduces cost of capital through reduction of risk. |

| Governance (G) | Data & compliance systems | TCFD-aligned reporting infrastructure | Satisfies institutional ESG mandates |

Table 1: Intangible Asset Category of ESG by Taxonomy, Examples and Relevance to Investors

How ESG Factors Are Integrated into Corporate Valuation

Incorporation of ESG factors into corporate valuation is not an issue of adding a random premium or discount of a share price of a firm. It involves a methodical evaluation of the impact of ESG-related intangibles on the major value drivers of a discounted cash flow (DCF) or multiples-based model: revenue growth, operating margins, capital expenditure needs, working capital efficiency, and discount rate. ESG in corporate valuation is best used where the analyst is able to trace a causal line between a particular ESG attribute such as a best-in-class employee health and safety programme and a measurable financial impact such as reduction in staff turnover costs or insurance premiums.

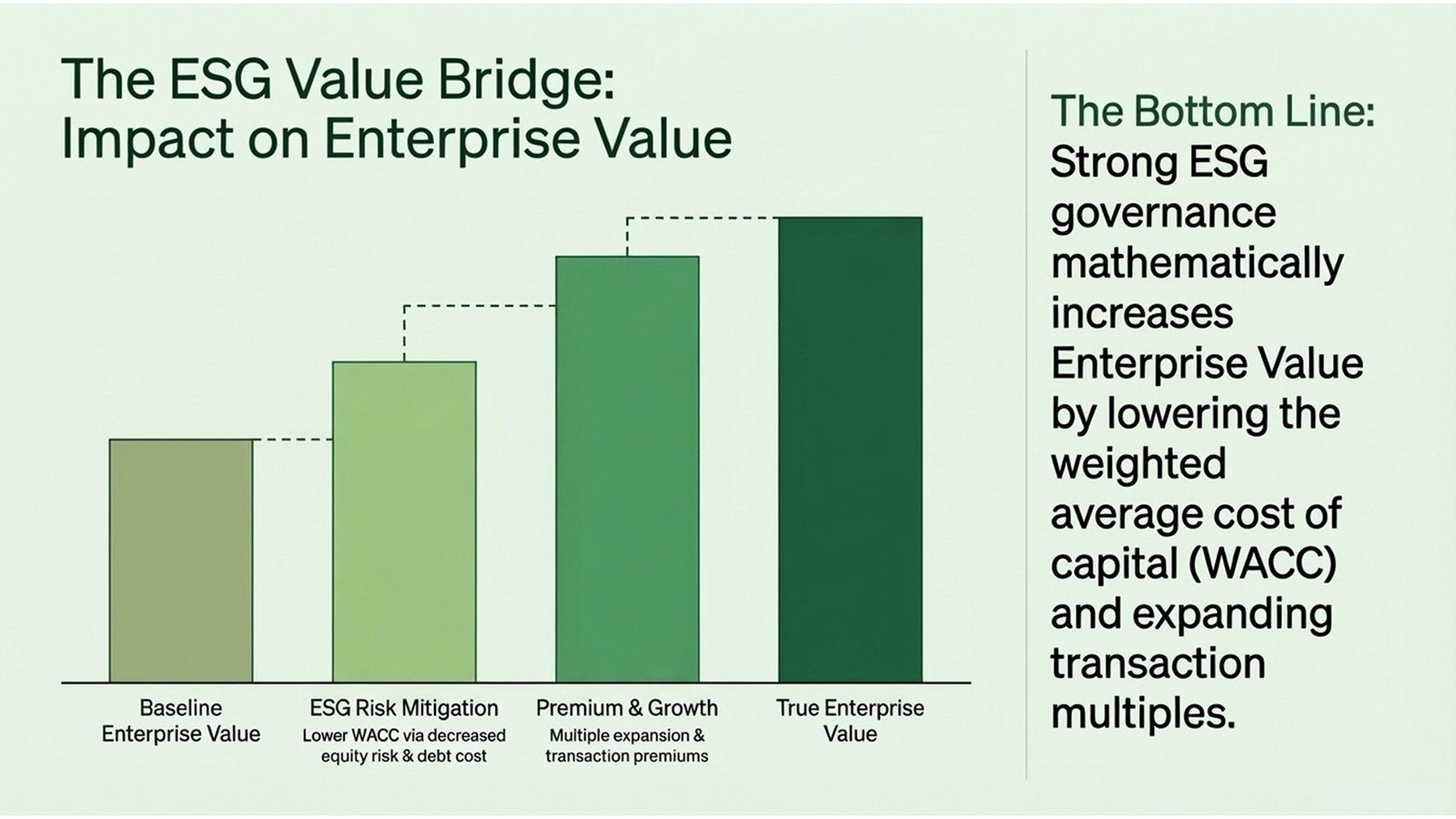

Within DCF framework, good ESG governance is able to reduce the weighted average cost of capital (WACC) in two senses. First, it minimizes the equity risk premium, as it signals that the management has foreseen and mitigated the most important operational, regulatory and reputational risks. Second, it has the potential to lower the cost of debt a lender will be willing to provide a borrower with more favorable rates on a sustainability-linked bond or a green loan when the borrower satisfies pre-established ESG KPIs. In contrast, firms exhibiting low ESG track records can have an increased cost of borrowing, increased regulatory capital requirements, and an increased exposure to stranded-asset risk, which all raise the discount rate and squeeze enterprise value. The dynamic renders ESG intangible assets valuation, not just an academic activity, but an effective risk-management instrument to both corporates and their investors.

Other than the DCF, ESG factors are having a greater implication on valuation multiples. The academic and investment bank research has recorded a consistent ESG premium in the transaction multiples, especially those with high regulatory risk, such as the energy, mining, chemicals, and consumer goods industry. ESG due diligence has been institutionalised as a pre-investment gate in private equity and ESG value-improvement programmes are now regularly structured under post-acquisition value-creation programmes. To practitioners in M&A advisory, equity research or corporate treasury, the ability to determine the impact of ESG attributes on multiples is thus essential as any technical modelling ability.

Five Key Steps in the ESG Intangible Asset Valuation Process

A disciplined series of steps that reflects the traditional practice of valuing intangible assets is followed to complete a rigorous ESG intangible assets valuation engagement, which includes extra layers of ESG-specific information collection and judgement. The flow process table below gives a tabular view, the discussion below expounds on the most important aspects at each of the stages.

| Step | Activity | Output / Deliverable |

| 1 | Establish valuation purpose and standard to be used. | The scope of engagement note: IFRS 3 PPA, impairment test or investor reporting. |

| 2 | MAP ESG strategy to asset classes (E, S, G) | ESG asset taxonomy in accordance with IAS 38 identifiability. |

| 3 | Gather ESG reports and ratings, as well as operational information. | Authenticated information set based on TCFD reporting, GRI filing, ESG rating companies. |

| 4 | Choose and use valuation techniques, by class. | Draft fair value estimates, scenario and sensitivity analysis. |

| 5 | Compare the benchmark results with market and transactions data. | Comparables analysis; support of royalty rate and discount rate. |

| 6 | Balance the ESG intangible values in the total business valuation. | Enterprise value bridge with contribution of ESG values. |

| 7 | Create disclosure ready valuation report. | Documented report with complete assumptions which are auditor-supported. |

Process Flow 1: ESG Intangible Asset Identification and Valuation – Step-by-Step Workflow

The initial one is to establish a clear purpose of the valuation. The nature of the engagement (purchase price allocation under IFRS 3, impairment test under IAS 36, a fairness opinion to an investor, or a sustainability-based incentive design exercise), the intended use of the value, the required level of documentation, and the amount of conservatism that should be applied by the valuer, all depend on the purpose. The mixture of these purposes is one of the pitfalls of beginning the career and the problem will become down-stream as the review of the output by auditors or regulators reveals it.

Mapping ESG strategy and asset categories and bringing together ESG data are the second and third steps that require specialist knowledge to pay off. ESG intangibles can hardly be identified as such in the accounts of a company. The analyst has to interpret sustainability reports that are prepared following the Global Reporting Initiative (GRI), Task Force on Climate-related Financial Disclosures (TCFD) and International Sustainability Standards Board (ISSB) standards and convert their qualitative narratives into asset categories, meeting the identifiability requirements of IAS 38. This not only needs an accounting literate, but also a vision of what the ESG outcomes really lead to in business performance. Intangible asset disclosure importance is made immediately obvious here: when companies have disclosed sustainability in a detail, consistent and independently audited manner, they will present much more raw material to this step than those with vague, or boilerplate sustainability reporting.

The fourth and fifth steps include the choice of the relevant valuation method, and the stress-testing of the results. The second big table in this paper summarises the key methods and how they can be used in various ESG intangible assets classes. One of the most important disciplines at the modelling stage is scenario analysis: since ESG-related value drivers, such as the regulatory policy, consumer sentiment, climate physical risk, etc., are especially vulnerable to structural change, a single-point estimate is nearly never enough. The valuer is expected to outline at least a base case, an upside case of accelerated ESG tailwinds, and a downside case of reversal in regulations by the authorities or a lack of stakeholder engagement.

Real-World Cases, Challenges, and Lessons Learned

Real transactions and investment decisions are the best way of demonstrating the practical issues of ESG in corporate valuation. A prime example of this is the acquisition of one of the largest consumer goods companies in Europe by a global private equity consortium in early 2020s. The target had gone to great lengths over ten years of investment in sustainable sourcing programmes, to have Fairtrade and Rainforest Alliance certification on its major inputs of commodities. As part of the due diligence process, the valuation team of the acquirer was required to identify and value separately the intangible assets that they acquired under the IFRS 3. The customer relationship intangible, which was to a large extent motivated by ethical sourcing reputation of the brand, was monetized on a multi-period excess earnings model that singled out the revenue premium of ESG-conscious consumer groups. The resultant fair value of this asset was significantly greater than pre-acquisition assumptions had anticipated and the discovery had directly impacted the acquisition firm post-deal integration strategy where focus has been on security of the certification infrastructure instead of rationalising the infrastructure to reduce expenses.

The second educative case would be testing the impairment of exploration assets of a big North American oil and gas company following the constraining carbon rules. With governments in major operating jurisdictions shifting to more aggressive pricing of carbon the company valuation team needed to conduct a review of the impairment of its current intangible exploration resources, including, but not limited to, capitals of cost associated with drilling rights and geological information under IAS 36. The exercise involved combining climate scenario analysis (based on IEA Net Zero by 2050 case as a point of reference), into the recoverable amount calculation. The moral was clear: environmental regulatory risk, when appropriately modeled can transform what seems to be highly profitable long-term assets into those that are economically stranded in a single valuation cycle. This case is a compelling example of the intangible asset disclosure importance that goes beyond the compliance with the financial reporting to operational risk management.

A third instance, based on the equity research space, is the adoption by a large institutional asset manager of scores of governance quality in its discounted cash flow models of emerging market equities. The company created its own methodology that translated ratings of third-party governance into basis-point adjustments of the equity risk premium in the calculation of its WACC. Firms that had good board independence, clear policies on related-party transactions, and good whistleblower policies paid a lower equity risk premium as compared to governance laggards in the same industry. Back-testing showed that the adjusted models were better predictors of future stock price behavior of a three- to five-year horizon, which confirms the intuition that governance capital is a real concept of value-generating, and not a mere compliance form. The case supports the idea that the systematic application of intangible assets valuation of ESG enhances the results of investments, and does not only respond to the requirements of the regulations or reputation.

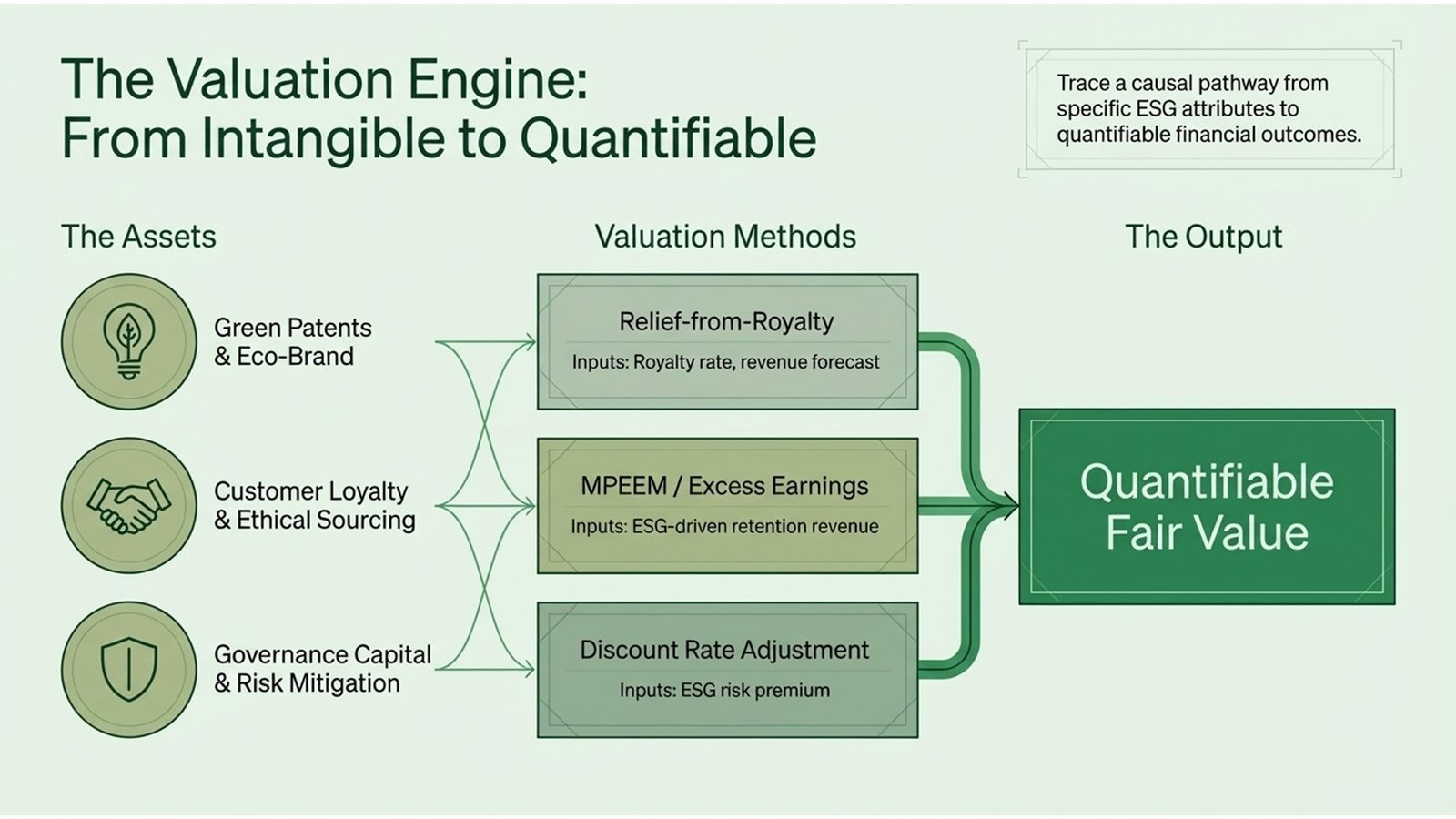

| Method | Best Suited For | Key Input / Driver | Main Limitation |

| Relief-from-Royalty | Green patents, environmentally brand licences. | Royalty rate, revenue forecast | Essential ESG royalty guidelines. |

| Cost Approach | Compliance systems, internal ESG data systems. | Replacement / reproduction cost | Disregards benefit created economically. |

| MPEEM | Ethical sourcing loyalty among the customers. | Revenue due to retention as a result of ESG. | Separating ESG contribution is not easy. |

| Discount Rate Adjustment | Governance capital, risk reduction on ESG. | ESG risk premium / score | Conversion to a score to rate is subjective. |

| Real options / Contingent Claims. | Clean transition to energy, green R&D. | Volatility, life of option, exercise price. | Requires sophisticated modelling |

Table 2: Valuation ESG Intangibles Assets – Comparison and Limitations

Disclosure, Investor Expectations, and the Path Forward

The connection between the quality of disclosure and valuation of ESG intangible assets is mutual and more and more determinant. An improved disclosure allows more effective valuation; more effective valuation allows investors to be willing to pay higher prices to ESG-linked value. This virtuous circle is, however, dependent on the quality and comparability of the disclosure standards- an area which has been long considered a weak point in corporate ESG reporting. The spread of rival frameworks (GRI, SASB, TCFD, CDP, UN SDGs) resulted in a disjointed market that posed a challenge to investors and valuers to compare companies on like-for-like basis. The creation of the ISSB and the release of the IFRS S1 and IFRS S2 is the biggest step in the right direction to resolve this issue and its gradual implementation by jurisdictions worldwide is likely to greatly enhance the availability of raw material in the intangible asset disclosure importance-driven valuation work.

In the case of institutional investors, the ESG due diligence process has developed into a multi-step analytical process, rather than a checklist process. The following process flow table shows how a complex asset manager can consider ESG intangible assets throughout the entire investment cycle- starting with initial screening process till the monitoring of the portfolio. Individuals who are interested in working in the equity analysis field, the private equity field or institutional asset management will discover that knowledge of this process is becoming a minimum requirement and not a distinguishing skill set.

| Phase | Investor Actions | Key Considerations |

| Screening | Use ESG exclusion filters; filter shortlist target industries and companies. | Check source of ESG ratings; differentiate laggards and leaders. |

| Assessment | See sustainability reporting, TCFD reporting and proxy filing. | Greenwashing test; disclosure consistency test (over time). |

| Quantification | Incorporate intangible asset values of ESG in DCF and multiples. | Adjust discount rate of ESG risk premium; results of model scenarios. |

| Engagement | Discuss with management ESG targets, KPIs and capital allocation. | Seek board-level ESG accountability; request forward-looking disclosure |

| Monitoring | Monitor ESG score changes, regulatory changes and risk of litigation. | Value assessments on intangible assets should be re-valued at every reporting period. |

Process Flow 2: Investor ESG Due Diligence – Stages, activities and factors to consider.

Greenwashing, where businesses exaggerate their environmental, social and governance performance in their social reporting compared to their actual performance is also a major issue to investors and valuers. The US Securities and Exchange Commission, the European Securities and Markets Authority and the UK Financial Conduct Authority have initiated several high-profile regulatory actions against asset managers and corporates alike which have claimed to be misleading ESG claims. This is a risk and an opportunity to the valuation professional: a risk because it may cause him or her to use the unverified ESG disclosures as inputs to a valuation model and an opportunity because it may allow him or her to provide a real value by subjecting the disclosures to an independent review. Comparing ESG data reported by companies with other sources, such as NGO ratings, regulatory reports, news sentiment analysis, and supply-chain audits has emerged as a significant quality control measure in the practice of rigorous ESG in corporate valuation.

Conclusion: Actionable Insights for Professionals

Valuation of intangible assets and convergence of ESG strategy is not a fad. It is indicative of a more fundamental structural change in the pricing of risk in the market, in the definition of disclosure requirements by regulators and the capital allocation by investors. Among the most profitable investments of time and effort in the field of finance today, building actual skills in ESG intangible assets valuation is one of the most lucrative investments of time and resources among the junior to mid-level professionals in the field. The above discussion has the following actionable insights as a summary of the practical insights.

Develop the conceptual bridge between the ESG strategy and financial value drivers. The most widespread failure mode of analysts who are new to the field is the tendency to see ESG as a qualitative overlay to a fairly traditional financial model. The field needs the reverse of that: based on the ESG results, one is to follow the effects, step by step, to revenue, cost, risk, and growth. Early learning of this analytical habit will make your work stand out compared to your peers who continue to be at the level of ESG scoring without putting it into economic terms.

Research on the disclosure frameworks. The expertise in IFRS S1 and IFRS S2, GRI, and TCFD is taking the form of a minimum requirement in corporate reporting, M&A advisory, and institutional investment positions. Knowing not only what these frameworks entail, but why certain disclosures are decision-relevant to investors and valuers will assist you to better interact with finance directors, audit committees and sustainability teams. The increasing relevance of intangible assets disclosure in financial reporting is that specialists who will help bridge the gap between disclosure of sustainability and the impact on financial reporting will be in demand.

Simulate ESG value drivers scenario-based modelling. Since the uncertainty in the structures of ESG-related value drivers such as policy change, physical climate risk, consumer sentiment shifts is a structural uncertainty, the skill to build and communicate multi-scenario valuations is a requisite technical skill. Begin with basic two- or three-scenario models and develop complexity as you get to know more about the drivers behind it. The science of recording all the assumptions and correlating it to a particular source of data or a particular research will also be helpful to you when your work is audited, by your clients or regulators.

Sceptically treat ESG data inputs. Not every ESG reporting is as reliable as it is in the case of greenwashing. The practice of verifying data reported by companies with independent sources is a career skill that insures your analysis and provides a true value to clients. This is particularly relevant given that ESG in corporate valuation is more mainstream and the motivation to companies to tell positive ESG stories is increasing.

Lastly, learn to be flexible in this field. The regulatory requirements, standards, and the market conventions as well as investor expectations of ESG intangible assets valuation are changing very fast. The habit of lifelong learning, via professional development, through networks of peers and through reading of primary regulatory and standard-setting publications, will help you make sure that your competence keeps up to date with the discipline, and that you will be in a position to make a difference as both the discipline and the market around it continue to evolve.