Cross-Border Intangible Asset Valuation

The world economy is more of a running on intangible assets. The large proportion of the enterprise value in knowledge intensive industries now lies in brand, patents, customer relations, proprietary software, trade secrets and organisational know-how. By being held, licensed or transferred across national borders, which they are regularly in multinational enterprise (MNE) groups, these assets generate a combination of technical and regulatory problems, which neither traditional accounting nor national practice of valuation is completely capable of addressing on its own. The cross-border valuation of intangible assets is an area of intersection of financial valuation theory, international taxation, transfer pricing regulation and accounting standards, which requires the breadth and depth of the professionals who practise this area.

Cross-border intangible asset valuation is quickly being noted as a competitive requirement to the junior to mid-level professionals pursuing their careers in corporate finance, M&A advisory, international tax, or forensic accounting. The Base Erosion and Profit Shifting (BEPS) project by the Organisation of Economic Co-operation and Development has radically changed the approach to intercompany IP transaction by tax authorities. Simultaneously, the introduction of IFRS 3 purchase price allocation requirements by an ever-growing list of jurisdictions, such as a large number of jurisdictions in Asia-Pacific and the ASEAN region, implies that the need to obtain technically robust intangible asset valuations in cross-border M&A has never been more. Experts with a better grasp of the intersection of valuation methodology and transfer pricing regulations as well as international accounting principles will be well placed in a host of different jobs.

This paper will give an organized, practical summary of the main concepts, procedures, issues, and practical lessons which characterize the cross-border practice in intangible assets. It also explains the reason as to why, organized learning, including cross-border IP valuation training ASEAN-focused programmes that are being increasingly provided by professional bodies and specialist providers are useful to professionals who are interested in developing expertise in this complicated area or consolidating existing expertise. It is interspersed with process frameworks, case illustrations and comparative tables to make sure that the discussion is rooted in practice.

The Regulatory Landscape: Why Cross-Border IP Valuation Is Uniquely Complex

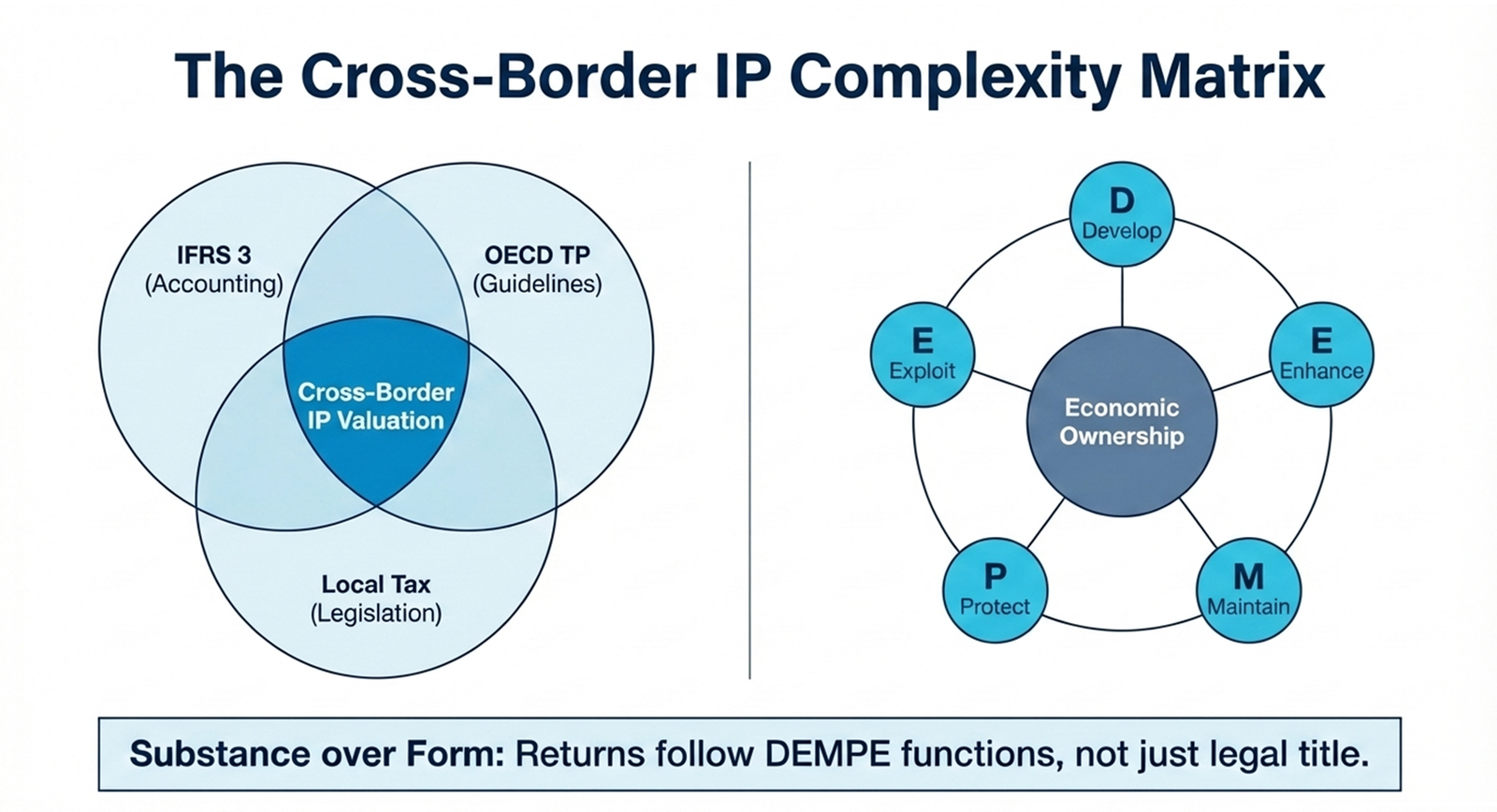

The appreciation of an intangible asset in one jurisdiction is in itself a difficult task. When done across borders, this adds to the complexity many times over since the valuer has to meet the requirements not only of at least three sets of rules: international financial reporting standards (principally IFRS 3 and IAS 38 of business combinations and intangible asset recognition), but also of the OECD Transfer Pricing Guidelines of Multinational Enterprises and Tax Administrations and to the domestic tax laws of all the jurisdictions Such structures do not necessarily all point in that direction. An amount of fair value that is calculated under the IFRS 3 financial reporting model, such as the one that needs to be charged into the accounts to reflect the arm-length price, may not be the same as the price that must be charged under the transfer pricing model under the same transaction and this can create documentation and reconciliation issues to the finance unit.

The BEPS project of the OECD (especially Actions 8-10, which concern the correlation of transfer pricing results with the creation of value), has been the most significant of the regulatory changes in the last 10 years in the cross-border valuation of the intangible asset. BEPS Actions 8-10 presented the notion of DEMPE functions: the discussion of which of the members of an MNE group actually Develops, Enhances, Maintains, Protects and Exploits an intangible asset. The main idea is that economic ownership of an intangible and thus the right to the returns of it must be the result of the performance of DEMPE functions, as opposed to the legal title in a low-tax jurisdiction. This has had far-reaching ramifications on IP holding structures that MNEs must make sure that the entity claiming IP returns has a real economic presence in the jurisdiction in which it is registered.

The ASEAN region has been experiencing a fast changing regulatory environment on cross border IP valuation. Most of the countries such as Malaysia, Thailand, Vietnam, Indonesia and the Philippines have revised their transfer pricing regulations over the recent years and have been shifting closer to the OECD guidelines but still have certain local characteristics. This convergence brings both opportunity and complexity to practitioners: opportunity, since an overarching consistent conceptual framework is now applicable across the region; and complexity, since the specifics of implementation, documentation thresholds and audit priorities are quite different across jurisdictions. The following table highlights the most important regulatory frameworks to Cross-Border Intangible Asset Valuation in major jurisdictions, including some of the ASEAN markets.

| Region / Jurisdiction | Primary Framework | Important IP Valuation Requirement. | Notable Feature |

| OECD Members | BEPS Actions 8–10; Transfer Pricing Guidelines | DEMPE; functions analysis Arm length pricing. | The allocation of risk should be economic. |

| European Union | ATAD I & II; Pillar Two (GloBE rules) | At least 15% effective rate of tax on MNE profits. | There is increased scrutiny of IP box regimes. |

| United States | IRC §482; Treasury Regulations | Apply commensurate with income to IP transfers. | Periodic Adjustments Authorized by IRS. |

| ASEAN (selected) | Guidelines on national TP; APA programmes. | Different levels of documentation per country. | Quick alignment of standards to OECD standards. |

| China | Tp Special Issues; SAT Bulletin 6 (2017). | Value chain analysis; place-specific benefits. | Local market premium concept was implemented. |

| India | Income Tax Act 92; Safe harbour rules. | There is strict documentation; APA programme is active. | Intensive audit on the IP transactions. |

Table 1: Key Regulatory and Transfer Pricing Frameworks by Region

Valuation Methods in a Cross-Border Context

The valuation techniques of cross-border intangible asset valuation are essentially those used in domestic assignments; the income approach (with the relief-from-royalty method and the multi-period excess earnings method), the cost approach, and the market approach. The difference in a cross-border situation is that it is more difficult to implement each of the methods consistently and reliably in all economic settings, tax regimes, and currency zones. An arm length royalty rate on a technology licence between a parent company in the US and a company in Germany might not be suitable on a licence to a manufacturing affiliate in Vietnam in a risk different profile, currency and regulatory environment. All these differences must be explicitly and documented changed by the practitioner.

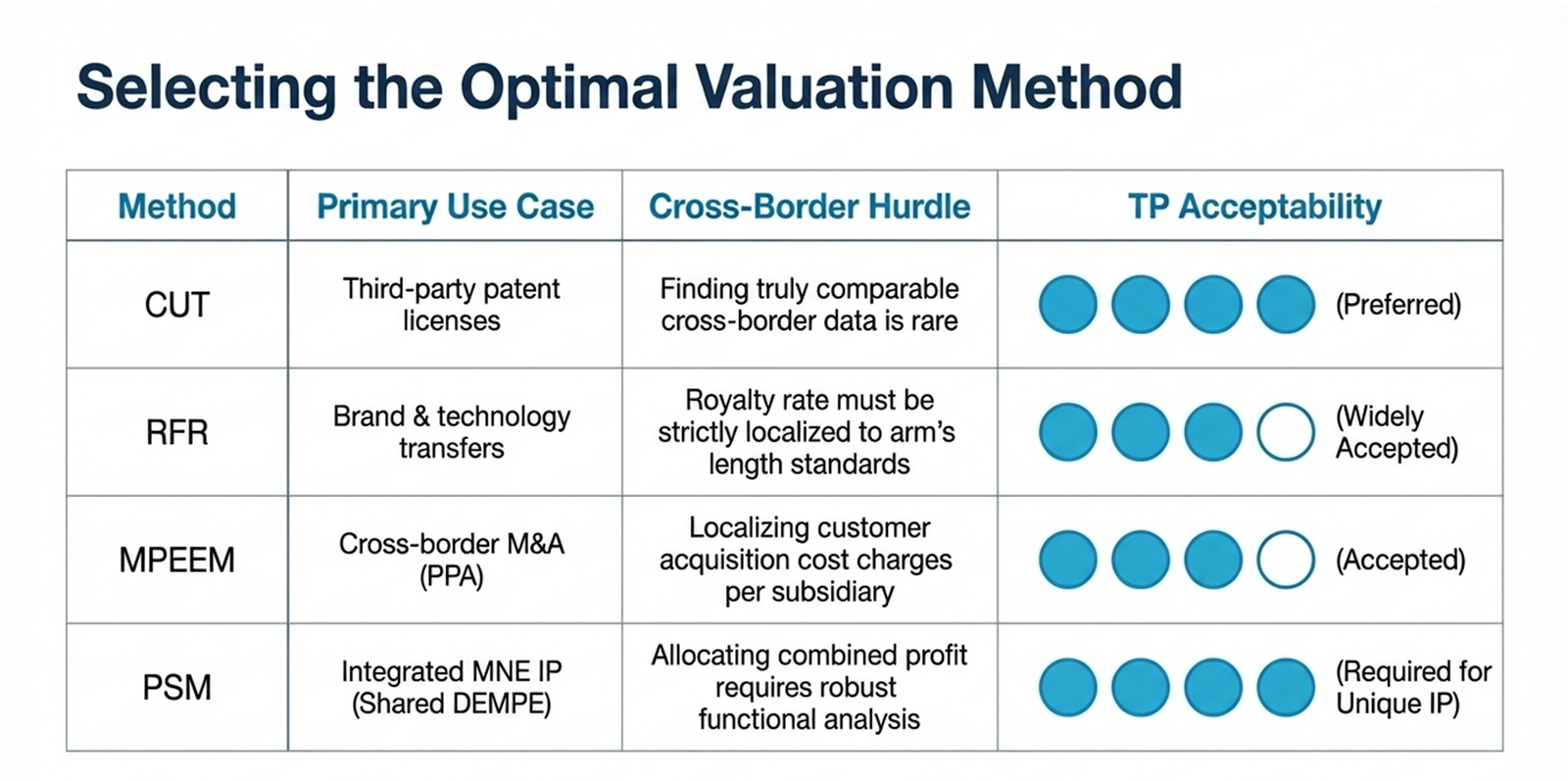

The most direct method which can be accepted as pertinent to transfer pricing purposes, but is also the hardest to put into practice, is the Comparable Uncontrolled Transaction (CUT) method, where third-party licences are found to comparable intangibles between unrelated parties. There are few truly similar cross-border licences, especially of highly unique intangibles like proprietary algorithms, specialised manufacturing process or market-leading brand. In many cases, practitioners have to deal with less than perfect comparables that are obtained in royalty rate databases like RoyaltySource, ktMINE, or Royalty Range, and have to make and record the adjustments to differences in geographic scope, exclusivity, and contractual term as well as the economic conditions of the corresponding markets. A method of profit split has been popularized by BEPS of highly integrated groups of MNEs in which no one entity can be easily defined as the party under test- a situation that is typical in technology and pharmaceutical multinationals with distributed R&D operations. The following table is an organized comparison of the major valuation techniques when used in cross-border.

Another issue that can be very complex and is not always taken seriously by practitioners new to work across borders is currency issues. In cases where the future flows of royalty or profits are in one currency, but the discount rate is in a capital market in a different currency, the valuer needs to convert cash flows to a single functional currency based on forward exchange rate forecasts, or use a local-currency discount rate based on the inflation and risk differentials between the two economies. One of the most frequent technical errors made when valuing intangible assets cross-border, which is also becoming the focus of more and more scrutiny by tax authorities and auditors, is inconsistency in currency treatment applying a USD-denominated discount rate to cash flow of Indonesian Rupiah cash flows without correction, e.g.

| Valuation Method | Normal Cross-Border Application. | Cross-Border Complexity | TP Acceptability |

| Similar Uncontrolled Transaction (CUT). | Licences of patent with third party standards. | It is hardly possible to find really similar cross-border licences. | Preferred where available |

| Relief-from-Royalty (RFR) | Group to group brand and technology transfers. | Royalty rate should be what is arm length in each jurisdiction. | Widely accepted |

| Multi Period Excess Earnings (MPEEM) | Cross-border M&A PPA Customer relationship. | The charges of CAC have to be localised on a subsidiary basis. | Accepted |

| Profit Split Method (PSM). | Well-integrated MNE IP that have common DEMPE functions. | The combined profit allocation is done using strong functional analysis. | Needed to be unique IP. |

| Hybrid Cost Plus / CUP. | Contract R&Ds; toll manufacturing with IP. | Uniformity by jurisdiction demanded. | Moderate |

Table 2: Cross-Border Valuation Methods – Applications, Complexity and Acceptability of Transfer Pricing.

Five Key Steps for a Robust Cross-Border Intangible Asset Valuation

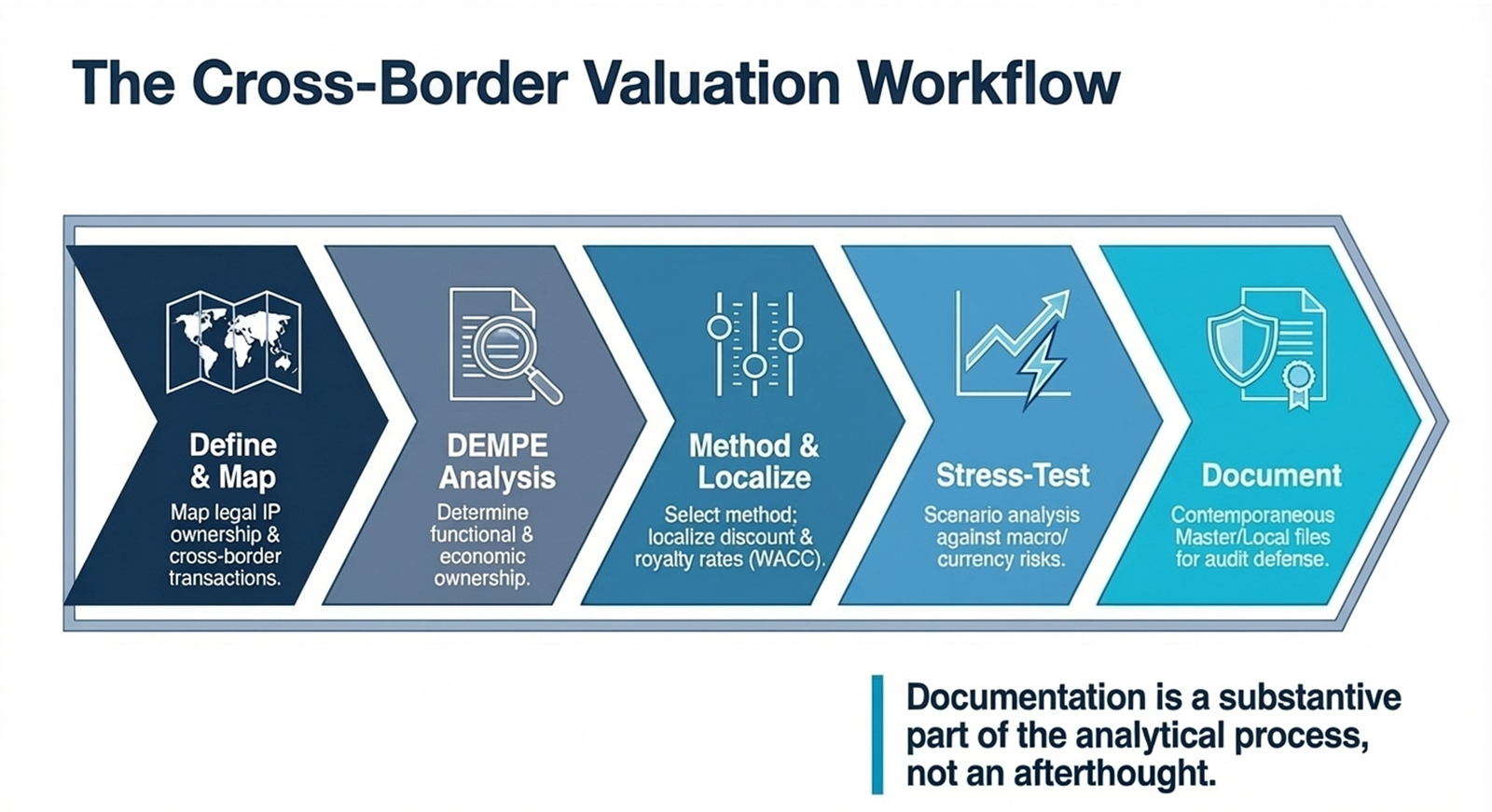

There is no single sitting to create a robust cross-border intangible asset valuation. The product of a rigorous multi-level process, which combines legal, financial, operational and regulatory inputs, is it. The 7 essential stages of a cross-border IP transfer valuation are as outlined in the process flow below; five main practitioner disciplines which underlie success in each of the stages are addressed in the succeeding paragraphs.

| Step | Activity | Output / Deliverable |

| 1 | Determine the transaction: nature, parties and jurisdictions. | Status of transaction and map of legal entities and IP ownership. |

| 2 | Carry out functional analysis (DEMPE): who is developing, enhancing, maintaining, protecting and exploiting the IP? | Report of the functional analysis; economic ownership determination. |

| 3 | Recognize the intangible assets and determine valuation techniques to use according to OECD principle. | Inventory of intangible assets; technique of choosing method memorandum. |

| 4 | Obtain market information: royalty rates, CUT deals, similar company multiples. | Benchmarking data; royalty rate band or similar deals. |

| 5 | Develop and stress test valuation models; use scenario and sensitivity analysis. | Base, upside and downside scenarios on draft valuation. |

| 6 | View local country documentation requirements and APA eligibility. | Application assessment APA Country-by-country documentation checklist. |

| 7 | Prepare technical valuation document and transfer pricing document. | Master file, local file and valuation report to submit to tax authority. |

Process Flow 1: Cross-border IP Transfer Valuation – Step-by-step Workflow.

The initial critical discipline is to base the analysis with the clear functional and economic profile. Prior to any model, the valuer should have the knowledge of who among the MNE group does the functions, who assumes the risks and who utilizes the assets that are involved with the IP in question. It is on this functional analysis that all the other steps will be based on. Technologically advanced but constructed upon an incomplete or misrepresentative functional analysis will not pass the test of even a well-endowed tax agency.

The second discipline is to choose the method, which best fits the facts, not the one which has the most favourable result. The OECD Guidelines stipulate that when doing transfer pricing, the most suitable method must be used depending on the nature of the transaction and the existence of other similar data which are reliable. Practically, advisers sometimes will choose approaches that will reduce the purported value of an IP transfer to tax purposes, or inflate the purported value to financial reporting purposes. High audit jurisdictions like India, Germany and more recently a number of ASEAN markets have developed the skill of determining method selection based on outcome and not facts.

Third, make rigorous localisation of assumptions. The rates of discount, royalty rate, growth rate and even tax rate all have to be indicative of the economic conditions of the jurisdiction where the cash flows in question are to be generated or where the IP is to be exploited. One global WACC that is used consistently throughout a cross-border structure can hardly be appropriate. The jurisdiction-specific discount rates constructed by practitioners should be based on the local risk-free rate (usually the yield on government bonds in the currency of the country being considered), a market risk premium suitable to the local equity market and a beta based on similar companies in the same business and location.

Fourth, scenario and sensitivity-analyze stress-test. Macro-level uncertainties that are particularly sensitive to cross-border IP valuations include fluctuations in exchange rates, changes in regulatory policies, changes in networks of bilateral tax treaties and political risk. An estimate of a point, which does not involve a sensitivity analysis, creates an illusion of accuracy. By showing a variety of results in varying situations: base, optimistic and stress, not only do you get a more honest answer, but also it will demonstrate analytical rigour to the auditor or tax authority that will go through the work.

Fifth, establish documentation trail at the beginning. The requirements on documentation of transfer pricing have greatly increased after the implementation of the three-tiered documentation framework by the OECD (Master File, Local File, Country-by-Country Report). In cross border IP transactions, the valuation report should be able to stand on its own as a contemporaneous document of the arm length analysis- one that was done prior to the execution of a transaction and not re-written post-factum. The earlier the professionals develop the documentation habit, the more they consider the audit trail as part of the valuation process and not a quick fix after the fact, the stronger their work would be in regard to its defensibility and worthiness to clients.

Real-World Cases, Challenges, and Lessons Learned

The cross-border IP transactions are one of the few areas of corporate finance that have spawned more litigation and regulatory controversy, and the case law that has developed over the last 20 years can provide valuable lessons to practitioners. The result of the case in the Altera Corporation case that dealt with the assignment of costs related to stock-based compensation in a cost sharing arrangement in the US Tax Court showed just how high the stakes of cross-border IP cost-sharing agreements are and how the IRS was ready to challenge long-established structures. Although the case ended with a certain interpretation of a particular regulatory provision, the overarching implication to practitioners of cross-border intangible assets valuation is that the cost-sharing arrangements must be created on a platform of true economic substance and up-to-date documentation, rather than tax optimisation itself.

Another didactic example is the cross-border M&A operation of a large European pharmaceutical company, which took over a mid-sized Asian biotechnology company, which had a pipeline of early-stage oncology programs. The purchase price allocation exercise involved the valuation team of the acquirer to value each compound in the pipeline separately, with a risk-adjusted net present value (rNPV) approach that discounted the estimated peak sales revenues, based on the likelihood of a compound progressing to the next development phase. The international aspect brought a lot of complexity: the discount rate needed to include not only the risk profile of the global pharmaceutical industry, but also the risks related to the jurisdiction of the regulatory approval in Asian markets. It was a lesson that when it comes to cross-border M&A, the PPA is not a purely domestic operation, carried out in the home market of the acquirer, but it should incorporate a global outlook on the risk, price and economic life. This form of multi-jurisdiction PPA challenge will become more common as professionals with cross-border IP valuation training ASEAN-relevant programmes face more and more cross-border mergers and acquisitions.

The third case is about the reorganization of the IP holding of a global consumer technology group following the BEPS reforms. The group had long been holding its IP in a low-tax European location via a structure that preceded the DEMPE analysis needs. After the BEPS, the tax authority of the group in the main country of its operation questioned the current flows of royalty on the grounds that the IP holding company did not have human resources and the ability to make decisions, which could be considered the economic owner of the intangibles. The case consumed years to settle and finally a large change of royalty rate and redistribution of profits to the operating jurisdictions. The most important lesson is that which can hardly be overemphasized: economic substance should be coupled with legal form in the practice of Cross-Border Intangible Asset Valuation in the present day. A valuation, which values a flow of royalty appropriately, but which is contained in a structure that does not represent a true economic ownership will ultimately be subject to regulatory scrutiny, no matter how technically sound the underlying valuation analysis is.

| Phase | Key Actions | Cross-Border Considerations |

| Pre-Deal | Mapping IP ownership; determining cross-border licensing. | Establish ownership of intangibles by the entities that possess them in the legal context vs. the economic exploitation by others. |

| Due Diligence | Make a survey of intercompany agreements; evaluate the history of TP compliance. | High audit risk flag jurisdictions or flag jurisdictions that are in dispute over tax authority |

| Valuation | Use IFRS 3 PPA; intangibles are to be valued at fair value at date of acquisition. | Modify country risk discount rates; localize royalty rates. |

| Integration | Revise IP holding structures to be post-deal structure. | Model tax effect of IP migrations; take substance requirements of BEPS into account. |

| Post-Deal Reporting | Complete PPA disclosures; set up continued TP policy of IP royalties. | Make IFRS 3 fair values and future royalty flows the same as TP pricing. |

Process Flow 2 Cross-border M&A PPA Intangible Assets

The ASEAN Dimension and the Case for Specialist Training

The ASEAN economic region has a particularly interesting setting of the practice of cross-border intangible asset valuation. Ten different economies at highly varying levels of regulatory maturity make up the region, which has a combined GDP that has increased significantly within the last twenty years and a booming M&A market fueled both by foreign investment into the region and among region members. Japanese, South Korean, United States, and European technology, consumer goods companies, healthcare, and financial services companies have all made large purchases in ASEAN markets which have created PPA requirements as well as current transfer pricing commitments of IP assets which cross more than one jurisdiction.

The convergence in the regulation that is currently being experienced in the region (where Malaysia, Thailand, Indonesia, Vietnam, and the Philippines are all in the process of converging towards OECD-compatible transfer pricing systems) provides a more analytically consistent environment than that which was present even half a decade ago. But convergence is not the same thing as being uniform. There are local sensitivities in documentation requirements, choice of audit selection, availability of advance pricing agreement (APA) programmes and the meanings of the arm length concept such that a practitioner cannot just use a generic OECD analysis and expect it to be universally accepted in all ASEAN jurisdictions. That is exactly what cross-border IP valuation training ASEAN-orientated programmes are aimed at bridging, so that professionals could not only grasp the conceptual framework, but also the jurisdiction-specific awareness that would help them navigate this environment without any issues.

The business case of investing in specialist training in Cross-Border Intangible Asset Valuation is strong to professionals working in or located in the ASEAN markets. The supply of trained professionals in the region is not keeping up with the increasing demand of qualified practitioners to work on IFRS 3 PPAs, preparing transfer pricing documentation regarding IP transactions and preparing advice on cross-border IP restructuring. The response of the professional bodies, specialist valuation firms and university-based programmes has been to create structured curricula that integrate valuation methodology with the transfer pricing rules, case studies based upon actual ASEAN transactions, and practical modelling exercises. Graduates of such programmes with on-the-job training in cross-border interactions are in a good position to pursue high-level positions in advisory firms, MNE tax and treasury operations, and regulatory authorities in the region.

Conclusion: Actionable Insights for Practitioners

Cross-border intangible asset valuation is a highly technical, professionally gratifying specialisation in corporate finance today. It involves the practitioner to combine the competencies of financial valuation, international tax, accounting and economic analysis-and to put them into practice in a wide range of legal, regulatory and economic settings at once. The actionable insights that follow are the summarization of the practical advice that is provided in the entire course of this article into a list of priorities that should be pursued by professionals in this field, at any phase of their career.

Learn DEMPE first. The conceptual basis of cross-border practitioners focusing on intangible asset valuation is the best understanding of how the OECD BEPS Actions 8-10 characterize economic ownership of intangibles by considering them through the prism of DEMPE functions. In its absence, even technically superior models of valuation might be constructed on a structurally unsound basis-one which a prudent tax authority will spot and question.

Establish good localisation behaviour. Do not impose a globally consistent discount rate, royalty rate or growth rate on a valuation across borders without clearly explaining why it is the right rate–and more often, alter it to reflect the economic environment in which each jurisdiction is located. It is the rigor with which a localisation of assumptions can be undertaken that makes the difference between work that can be scrutinized by regulators and that which cannot.

Documentation should be considered in the valuation, and not as a different compliance activity. The contemporaneous documentation is not only an administrative necessity in the transfer pricing, but it is also an element of the analytical process. It is preferable to construct the documentation trail along with (and not after) the valuation model, to come up with more consistent and defensible and ultimately more valuable work product.

Make investments in knowledge specific to ASEAN. The regulatory environment in the ASEAN region is dynamic and consequential among professionals dealing with or advising on transactions of the region. One of the most effective methods to fast-track professional development and develop the jurisdiction-specific competence required by clients and employers in the region is to seek out cross-border IP valuation training ASEAN-focused programmes, be it provided by professional bodies, international advisory firms or specialist training providers.

Lastly, develop intellectual modesty regarding the constraints of any one valuation. Cross-border valuation of intangible asset entails actual uncertainty- future cash flows, suitable discount rates, similar transactions and regulatory outcomes. The most plausible and professionally grown-ups are practitioners who own up this uncertainty, package their products as fully justified approximations as opposed to absolute solutions, and structure their analyses in a manner that they are clear, falsifiable and can be revised as new information comes into the limelight. When a case of tax authority dispute may take years to resolve with a resultant outcome that may redefine the business structure, such rigour and intellectual honesty is not only a professional value but a practical requirement.