Human Capital as an Intangible Asset

Ask the average finance professional to name the most valuable asset of a company, the first response is to indicate the balance sheet – property, plant, equipment or a patent portfolio. But in a majority of the contemporary organisations, the most valuable creation that can drive long-term value is all off the balance sheet, the knowledge, relationships, judgment and capability of its people. It is what the economists and strategists refer to as human capital and learning to look at it as an asset, but not only as a cost, is one of the most practically effective changes a professional may incorporate in his or her career.

The difference between the accounting and the true valuation of people by investors is huge. When the acquiring company obtains it at a high price that is far beyond the book value, the price is in large part an recognition of intangibles: brand loyalty, proprietary know-how, client networks and the richness of the workforce. Knowing how to calculate the value of human capital assets and why it is important will enable junior and mid-level professionals to not only talk more convincingly to the senior leadership but also learn why their growth as a person has an economic aspect.

The target audience of this article is professionals that are either establishing their careers, are training towards more strategic positions or are managing the people strategy within an organisation. It takes a stroll through the definition of human capital, the manner in which human capital is valued, the impact of the productivity of employees on enterprise valuation, cashflow valuation of customer relationships linking people with financial performance, and what you can do personally and at an organisational level to translate these ideas into practice.

What Human Capital Actually Means and Why It Belongs on the Asset Side

Economists Gary Becker and Theodore Schultz popularized the human capital term in the 1960s when they proposed that investments in people (in terms of education, on-the-job training and health) would yield a payoff just like investments made in physical assets did. The term human capital can be used in relation to business to mean the sum total of skills, experience, judgment and personal contacts that the employees would bring to work daily. It is why a senior salesperson can get deals done that a junior counterpart fails, and why a competent project manager will get things done on time and others fail to.

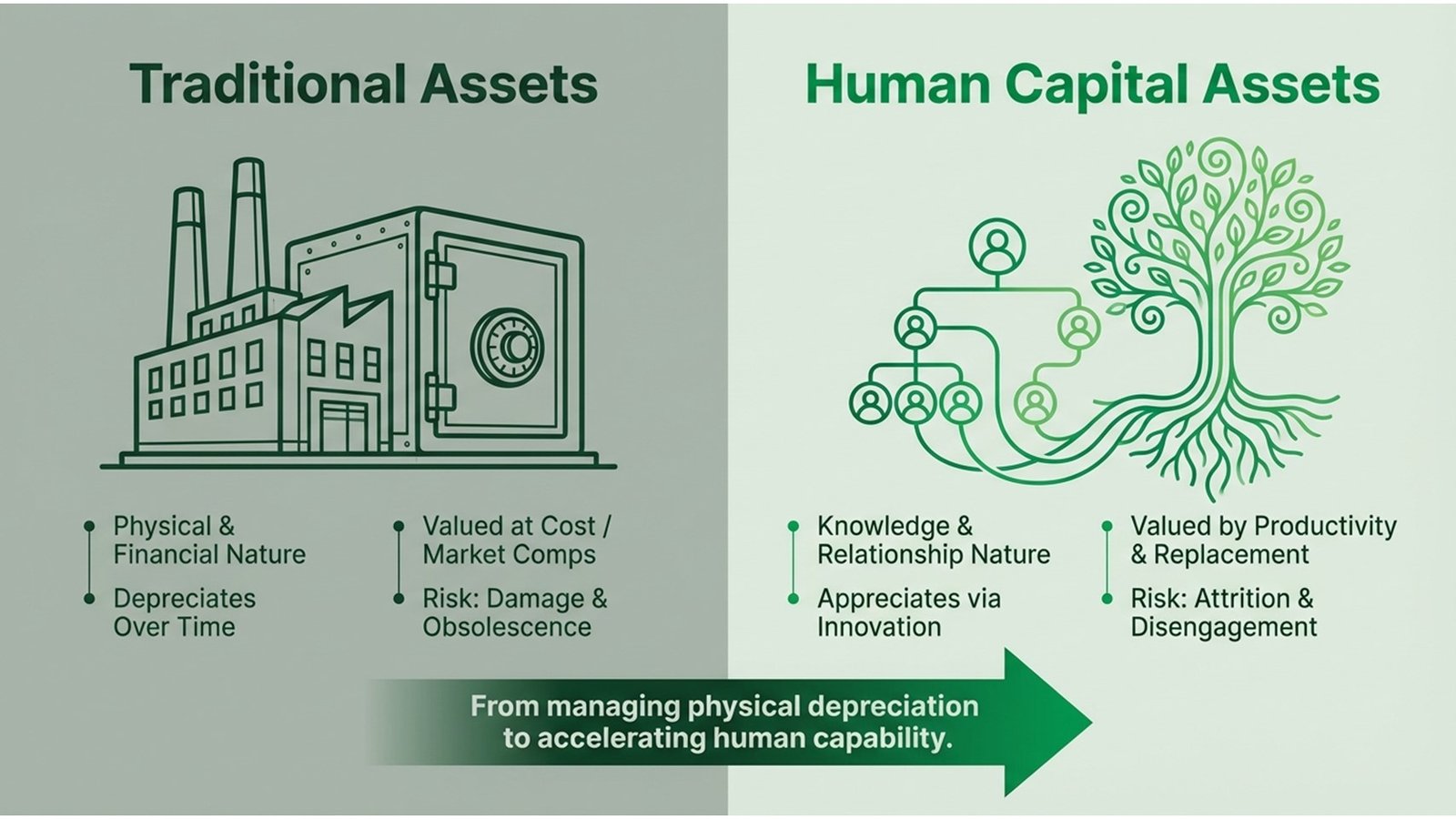

Human capital is an odd asset because it is not a tangible asset but is mobile. Human capital is unlike a factory, or a software licence, which can be walked out the door at the end of the day, and may never come back. This presents problems of valuation which the traditional accounting frameworks were not created to deal with. In the vast majority of worldwide accounting principles, the costs of training are charged against earnings in the year they are incurred as opposed to being capitalised over their useful life, thus one company that invests a lot in its human resource will report a smaller short-term earnings – although its long-term competitive advantage will be enhanced. This is a chronic underpricing problem due to this accounting imbalance.

Experts that are able to discern this difference acquire a valuable perspective. In examining the financial statements of a company, an expert analyst does not look at earnings before interest and taxes and leave but questions employee tenure, amount of training investment per head and employee turnover. These are human capital quality signal which are not reflected in the numbers however, which have a far-reaching impact on the cash generation in future. The following table compares the traditional asset characteristics with the human capital.

Table 1: Comparison Between Traditional and Human Capital Assets

| Dimension | Traditional Asset | Human Capital Asset |

| Nature | Physical or financial (equipment, cash) | The knowledge, skills, behaviour, relationships. |

| Will be on the Balance Sheet? | Yes -at cost or fair value | Uncommonly – dealt with as a cost. |

| Valuation Method | Depreciation schedules, comps in the market. | Measures of productivity, replacement cost. |

| Risk of Loss | Physical damage, obsolescence | Attrition, disengagement, knowledge drain |

| Value Creation | Production at full load. | Innovation, client trust, improvement of the process. |

Five Key Principles of Human Capital Asset Valuation

Managing human capital in an organised manner fits the disciplined approach of organisations that manage it financially. The five principles that follow summarize the key practical lessons out of human capital asset valuation models of major corporations and consultancies.

Table 2: There are Five Major Principles of Human Capital Valuation

| # | Key Point | What It Means in Practice |

| 1 | Monitor Financial Metrics as Track Person Metrics. | Sit with P&L should be revenue per employee, cost-to-hire and time-to-productivity. |

| 2 | Link Capability to Value Drivers | Determine the skills that bring in money or save money, and then invest in those initially. |

| 3 | Quantify Retention Risk | Simulate the loss of a key account manager or technical head and how it would affect the revenue. |

| 4 | Embed Learning ROI | All training programmes must have an output that can be quantified – less time to close deals, reduced errors, increased NPS. |

| 5 | Report HH to Leadership. | Develop quarterly human capital scorecard that will be reported with financial outcomes to the board. |

All these principles demand a change of thinking where HR data is perceived in terms of administration as record keeping as opposed to management intelligence. Other firms such as Microsoft have gone to the extent of connecting their People Analytics capability to the CFO office, as they understand workforce data is as financially significant as sales pipeline data. Any junior analyst or HR business partner who is able to elucidate these five principles in an occasion with the finance team will stand out right away.

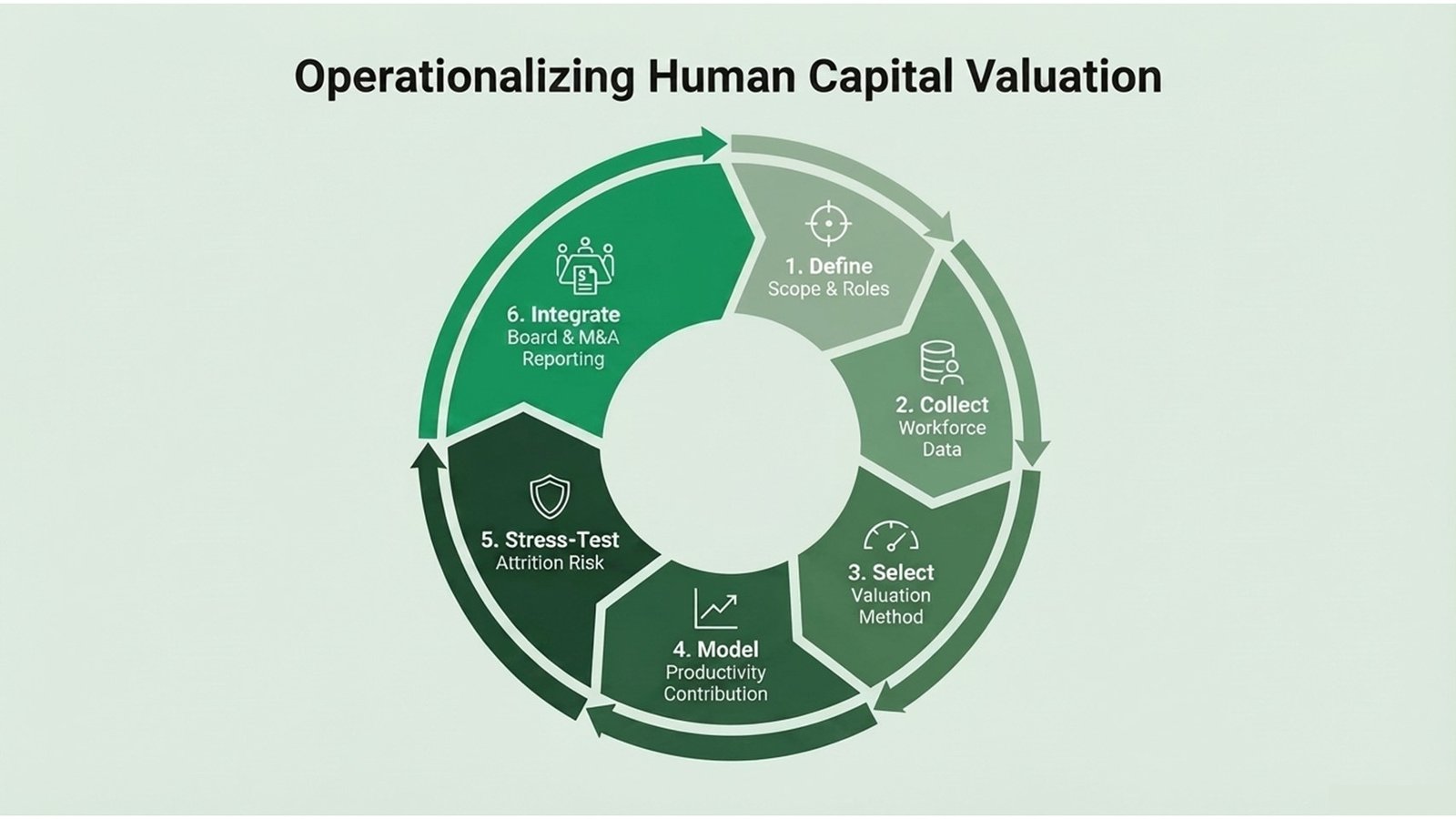

The very procedure of actually undertaking a human capital asset valuation takes a repeatable format, be it in a large corporation undertaking an internal audit or in an advisory firm undertaking a client in a merger or acquisition. The figure below indicates the major steps.

Process flow 1: What to Do with Human Capitals: Steps in Valuing Assets

| Step | Action | Output / Deliverable |

| 1 | Define the Scope | Determine the roles, business units or talent pools that are being valued. |

| 2 | Collect Workforce Data | The number of employees, experience, qualification, performance score, absenteeism and the rate of attrition. |

| 3 | Select Valuation Method | Select cost-based (replacement cost), income-based (productivity contribution) or market-based approach. |

| 4 | Model Productivity Contribution | Select cost-based (replacement cost), income-based (productivity contribution) or market-based approach. |

| 5 | Stress-Test for Attrition | Simulation: What would be the effect of the top 10% of the performers to leave? |

| 6 | Report and Integrate | Incorporate values of human capital in investor decks, board reports, and M&A due diligence packs. |

How Employee Productivity Affects Enterprise Valuation

The correlation between the workforce capability and the firm value is well-known in the corporate finance theory, and is poorly comprehended in practice. When analysts make up a (discounted) cash flow of a company, they are effectively assuming how well the organisation can continue to make future income – and that capacity is a direct proportion of how well and how productive the people are. This is the reason why the employee productivity affects enterprise valuation than it is explicitly recognized by most financial models.

Take the example of a middle-sized professional services company which has 400 consultants. Incremental revenue can be in the tens of millions per year, should the average utilisation increase by six percentage points, i.e. by a six-percentage-point increase in the workforce planning and skills development. Such a productivity increase will directly translate into a significant increase in enterprise value at a normal EBITDA multiple of eight to ten times. The management team did not purchase new equipment or a new business, they were able to enhance the output of the people that they had. It is the economic argument of the importance of investing in human capital development in the form of money which any board member can easily comprehend.

An actual case scenario of such dynamic is that of Infosys, the Indian technology services giant. In early 2010s, when attrition rates were high, the company recorded a drop in client satisfaction scores, as well as project overrun. The economic cost was great–not only in the immediate replacement hiring costs, which the company calculated to be about 1.5 times annual salary per turnover, but also in the delay, more difficult to quantify, loss of client trust and quality of project delivery. Taking Infosys as an example, employee engagement scores rose, attrition dropped and revenue growth re-accelerated when the company invested in a new leadership-led, large-scale workforce capability and culture transformation programme since 2014, which demonstrates that employee productivity is a factor that influences enterprise valuation not just in theory but in empirically measurable, empirically visible outcomes.

Customer Relationships as a Human Capital Cashflow — The Overlooked Link

The value of human capital in creating and maintaining client revenue is one of the least valued aspects of human capital. Client relations are not institutionalised in the organisation in the sense that the organisation has client relations in many service-intensive services, such as consulting, financial advisory, private banking, logistics, and healthcare, among others. Hinduism is held by individuals. A client remains not due to the brand on the letterhead but rather due to the trust that he or she has with a particular relationship manager, account director or clinical specialist. This is where the cashflow valuation of customer relationship is a very important tool.

Customer relationship cashflow valuation is the idea that the future client revenue can be thought of as a stream of cash flows that can be credited to the human relationships that create and sustain the revenue at least to some extent. With a key account manager who has a 10 year history with a strategic client leaving, there is no possibility that the future revenue of this client is at risk. In other instances it is existential. Companies that do not model this risk will always find it at the most inopportune time – when the buyer is undertaking a due diligence exercise of the acquisition, the auditors of the buyer will devalue the client revenue of the target since it is held by a few individuals that are leaving the company.

A good illustration of the application of this principle is in the wealth management industry. In several instances of advisor migration across companies, Morgan Stanley has publicly admitted that in such instances, client assets usually accompany advisor migration. This is not an exception, industry studies always indicate that in the private wealth, 40 to 70 percent of client wealth might be able to follow an outgoing advisor, based on the relationship strength, and quality of transition. What this means for practice is that any serious customer relationship cashflow valuation has to take into consideration the concentration of relationship ownership in particular persons and systems of transfer or institutionalisation of such relationships.

Process Flow 2: Customer Relationship Cashflow Valuation Steps

| Step | Action | Output / Deliverable |

| 1 | Map Key Accounts to People. | Determine the employees who own, manage, and/or impact each of the significant client relationships. |

| 2 | Determine Client Revenue at risk. | Calculate the value of revenue and margin of relationship based accounts. |

| 3 | Assess Relationship Depth | Evaluate the client relationship on breadth (contacts), level of trust and tenure of a contract. |

| 4 | Use Discount rate of People Risk. | Discount rate of relationship that is focused on an individual as opposed to a team is increased. |

| 5 | Construct Cashflow Model. | Future cash inflows (in project) per client relationship in terms of 3/5 years. |

| 6 | Become a part of Enterprise Valuation. | Reported as an element of intangible asset value in conjunction with brand, IP and goodwill. |

Challenges, Lessons Learned, and the Path to Better Practice

Although the argument of considering human capital as an asset that can be measured and handled is strong, the majority of organisations are still at the dawn stage. A number of structural and cultural issues always arise when firms are trying to institutionalise their way.

The initial issue is fragmentation of data. Payrolls, performance management and learning management systems, and CRM systems typically are not integrated in terms of workforce data. Significant human capital asset valuation demands linking the information that organisations have never formulated to communicate with. Those that have already taken steps forward such as Unilever and IBM have succeeded in doing so by establishing centralized people analytics systems that centralize workforce data and tie it to business and financial performance. The moral of the story is that data architecture is not a process, but rather a strategic investment.

The second problem is the short-termism that most corporate budgeting processes have. Training and development budget is often the first victim when the company is pressurized to reduce its costs- although a cut in the budget directly decreases the human capital asset base. Those organisations that have succeeded in this like Accenture have hedged investment in learning by instituting formal policies that regard it as capital expenditure and not an operating expense. In the minds of professionals in this tension, the best case is to invest human capital by using the rationality of employee productivity affects enterprise valuation to translate the people decisions into the monetary language of returns, rather than costs.

A third difficulty is measurement savvy. The most popular and common backward-looking indicators used by many organisations to measure human capital are: headcount, attrition rate and training hours undertaken. These measures give you an idea of what occurred but not what it was valuable. More advanced organisations are moving to future-oriented, value-based metrics: coverage ratio of talent pipeline, critical role preparedness, and relationship depth index of client-facing teams. The following are the building blocks of a true customer relationship cashflow valuation model and it needs a level of analytical sophistication, which most HR functions have yet to acquire. The message is not to wait till you have perfect data, begin with proxy measures and improve them as time goes on.

Conclusion: Turning Insight into Action

Human capital is not a soft concept that is clothed in financial terms. It is a tangible, quantifiable source of enterprise value and those who comprehend this and can effectively convey it are in a better place to make strategic decisions, attract investment in their teams and be able to communicate effectively with financial stakeholders. Such frameworks of human capital asset valuation are not exclusively the tools of the CFOs and M&A advisors. They are workable lenses that can be used by any intelligent professional in his/her work.

In the case of junior to mid-level professionals, the initial move of immediate importance is to start thinking in value terms as opposed to activity terms. Report what the training has brought about, rather than that your team went through 200 hours of training, faster onboarding, reduced errors, better client retention. Once you are able to demonstrate that employee productivity has an impact on enterprise valuation, you no longer get perceived as a cost centre but a value driver.

To people in client-facing positions, begin to develop institutional memory on your important client relationships. History of relationships with documents, share insights with your colleagues and make sure that your most valuable ties to clients are not entirely reliant on the individual. It is not merely good professional practice, but what good custodianship of a customer relationship cashflow valuation asset is like in the day to day business.

Lastly, lobby in your organisation to ensure that human capital is analysed in the same manner as financial capital. Indicate that push for people measures be included in board packs. Support programs which relate workforce data to business results. Modelling their return to champion training investment. It is not the organisations that have the most machines that will be the leaders in their industries in the coming decade: it is the organisations that comprehend, develop and retain the human capital that can make everything possible.