Certified Asset Based Intangible Valuation

Asset Based Valuation of Intangible Assets Under SFRS and IRAS Frameworks in Singapore

Introduction to Certified Asset Based Intangible Valuation

The intangible assets in the current knowledge-based economy are sometimes the greatest source of enterprise wealth. Physical assets of a company are often overshadowed by brands, intellectual property, customer relationships, proprietary technology as well as contractual rights. Consequently, asset based valuation of intangible assets has emerged as an important methodology of financial reporting, tax compliance, transaction support, and strategic decision making especially in such jurisdictions like Singapore where both the accounting and tax authorities are strict in their standards.

This paper offers an in-depth and practical discussion of asset based valuation on intangible assets which is particularly intangible assets sfrs requirements and intangible assets iras expectations. Through focus on regulatory consistent valuation practice in Singapore, the discussion provides the professionals in the finance field, the valuation field, auditors, and corporate leaders with the clear guidelines of defensible and compliant intangible asset valuation.

1. Understanding Asset-Based Valuation for Intangible Assets

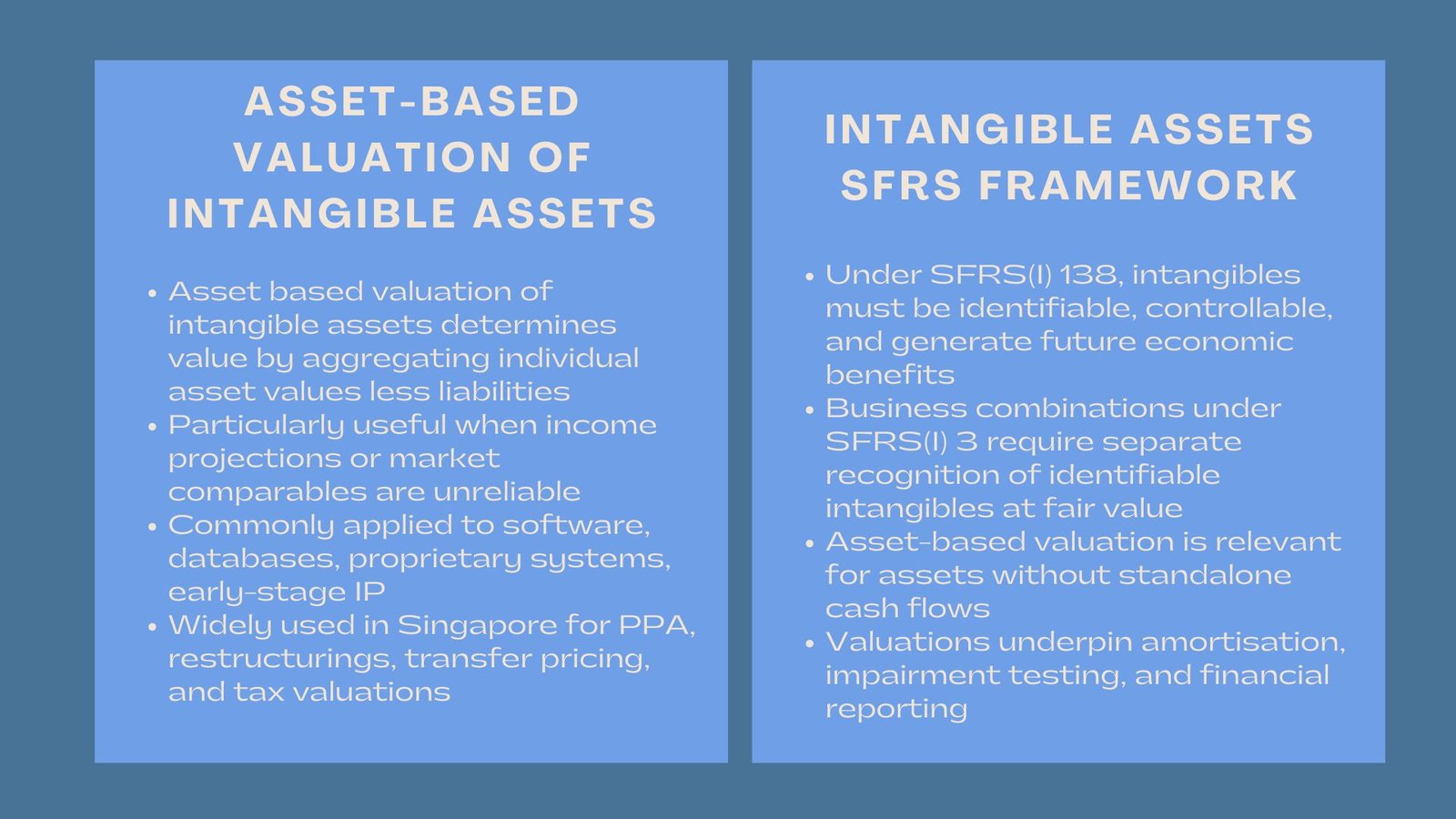

Asset-based valuation has long been related to tangible assets like property, plant and equipment. Nevertheless, when properly adjusted, asset based valuation intangible assets offers an orderly method of establishing the ascertained worth of identifiable non-physical assets. The value of a business or reporting unit under this approach is determined as the sum total of the value of individual assets in the business or reporting unit, less liabilities.

The valuation of assets in terms of intangible assets is based on replacement cost, reproduction cost or economic benefit forgone in case the asset is not available. This approach is particularly applicable when projections based on income are not very reliable or the amount of market comparables is limited. These can be internally developed software, proprietary databases, technical expertise or nascent intellectual property.

The use of asset-based valuation of intangible assets in Singapore is predominantly used in purchase price allocation exercises, internal restructurings, transfer pricing and tax associated valuations, where loaned compliance with intangible assets sfrs and intangible assets iras requirements is the most essential.

2. Intangible Assets Under SFRS: Recognition and Measurement

Intangible assets recognition and measurement are based on the Singapore Financial Reporting Standards (SFRS) that are highly aligned with the IFRS. The knowledge on intangible assets sfrs is something necessary in the application of any valuation methodology.

According to SFRS(I) 138 an intangible asset should be identifiable, the entity should have control over it as well as that it should be able to bring future economic benefits. Identifiability is realized either in the form of separability or in the form of contractual/legal rights. This definition is direct on the type of assets that can be included in an asset based valuation intangible assets exercise.

These initial recognition under intangible assets sfrs would usually have to be measured at cost. But, under business combinations that are subject to SFRS(I) 3, intangible assets should be recognised independent of the goodwill and measured at fair value as at the acquisition date. This is where the asset-based valuation methods will be of special interest, particularly to assets that are yet to produce stable cash flows.

Later measurement using SFRS may use the cost model or the revaluation model, but the latter is not widely used since there are no active markets on most of the intangible assets. The valuation done at the time of first recognition should therefore be sound, properly documented and justifiable since it underpins amortisation, impairment test and subsequent financial reporting.

3. Asset-Based Valuation Methodologies for Intangible Assets

Implementing the use of the asset based valuation of intangible assets needs to make a selection of the cost-based methods that are a reflection of the economic reality. The most widely used methods are the replacement cost method, and the reproduction cost method.

The replacement cost approach values the cost that must be incurred to reproduce an asset with the same utility at current materials, technology and processes. This method is common to software and databases, as well as internally developed systems, especially when functionality and not literal replication is the motivation of the economic value.

The reproduction cost approach, in its turn, approximates the cost of creating a full-scale copy of the asset. It is a more suitable approach to the unusual assets (proprietary algorithms or specialised technical documentation) where duplication needs to be identical to the original.

Regarding intangible assets sfrs, both solutions need to be modified in relation to physical deterioration (where applicable), functional obsolescence and economic obsolescence. These amendments make sure that the valuation of assets will be based on the current service potential of the asset and not the past investment.

In Singapore, auditors and regulators would like to see that asset-based valuation are clear in terms of assumptions about costs, obsolescence, and such in terms of the sources of data. This anticipation is rather consistent with intangible assets scrutinizing tax-based valuations.

4. Intangible Assets and IRAS: Tax and Valuation Considerations

Whereas SFRS regulates financial reporting, intangible assets iras guidance deals with taxation, transfer pricing and similar issues of capital allowance. IRAS lays so much emphasis on whether the results of valuation establish arm length and the substance of the economic value.

The application of asset based valuation intangible assets is common to support pricing in the restructuring exercises or transfers between related parties where the use of income based methods may be questionable because of uncertainty or untrustworthy projections. IRAS requires the valuations to be able to demonstrate that costs that are recorded are directly related to the creation of the asset and the mark-ups or even reevaluations should be economically reasonable.

In the taxation of intangible assets iras considerations, whether the asset is subject to allowances, amortisation of the asset, and whether the expenses are deductible are important consideration. IRAS can question the expenses allocations, especially the internally developed intangibles, to make sure that the valuations do not unnaturally overvalue the asset values to construct tax advantages.

Thus, there is high urgency that intangible assets sfrs valuations are aligned with intangible assets iras expectations. Although accounting and tax purposes are different, differences in reported fair values and tax position may attract audits, disagreements or reassessments.

5. Asset-Based Valuation in Purchase Price Allocation

Asset based valuation of intangibles in Singapore Purchase price allocation (PPA) is one of the most frequently used after a business combination. According to SFRS(I) 3, the acquirers should separate all recognisable identifiable intangible assets with goodwill.

Various intangible assets in most acquirings (assembled workforce, in-process R&D, proprietary systems, etc.) do not currently produce independent cash flows. Asset-based valuation gives a viable solution in such occasions, which complies with the requirements of intangible assets sfrs.

Valuers normally use replacement cost methods to determine the value of such assets, and in some cases, they use the obsolescence and contributory asset charges. In an intangible assets iras point of view, the PPA valuations can subsequently affect tax amortisation, calculation of deferred taxes, and subsequent transfer pricing positions.

Consequently, good documentation and consistency among reporting structures are necessary to curb regulatory risk.

6. Challenges in Valuing Intangible Assets Using Asset-Based Methods

Although it is useful, asset based valuation of intangible assets have a number of challenges. A major challenge is to establish the actual costs that are used to create an asset. Over- and under-inclusion of overheads or inefficiencies may distort value, whereas inefficiency at the other end may be inept at indicating the economic truth.

The other difficulty is associated with the evaluation of obsolescence. The utility of intangible assets can easily be lost in technological change, regulatory changes and competition in the market. Valuers will be required to reflect such risks accruing to the entity using professional judgement under intangible assets sfrs and intangible assets iras requires that the assumptions made under intangible assets are commercially reasonable and supportable.

Furthermore, the asset-based approaches might not be appropriate to reflect a potential upside, which is why they are less appropriate to high-growth or innovation-intensive assets. This is why asset-based valuation is frequently applied together with income-based valuations to bring triangulated support to the validity of fair value assessments.

7. Best Practices for Compliance and Defensibility

To be sure that the asset based valuation intangible assets can withstand audit and regulatory scrutiny, best practice in Singapore is focused on transparency, consistency and alignment with standards. The selection of methodology, cost inputs, factors of obsolescence and reconciliation to financial and tax reporting results should be clearly stated in valuation reports.

Coherence of intangible assets sfrs valuations prepared to account with and intangible assets iras positions prepared to compute tax means a decrease in the risk of challenge. In case of variation, they need to be clearly stated and provided through regulatory directions.

The involvement of experienced valuation consultants who have worked in Singapore regulatory environment will also increase the defensibility, especially where the transaction is complex and the intangible portfolio is worth a lot.

8. Conclusion: Strategic Importance of Asset-Based Valuation for Intangible Assets

The intangible assets will keep defining enterprise value, so asset based valuation intangible assets is a crucial methodology in the Singapore financial and tax environment. Used properly, it gives a systematic, open, and standards-based method of value to assets that cannot be priced in the market or whose income streams cannot be forecasted.

Awareness and alignment to intangible assets sfrs helps to record the financial position correctly whereas adherence to intangible assets iras position helps to reduce tax risk and to defend ourselves during an audit or a dispute. These frameworks combined highlight the strategic relevance of stringent intangible asset valuation- not as a formal check-up, but as a baseline of sound decision-making, success of transactions and value management in the long term.

Frequently Asked Questions

Q1. What is asset-based valuation for intangible assets?

Asset-based valuation estimates an intangible asset’s value based on the cost to replace or reproduce it, adjusted for depreciation and obsolescence. It is commonly used when reliable income projections or comparable market data are limited.

Q2. How does SFRS affect intangible asset valuation?

Under SFRS(I) 1-38, an intangible asset must be identifiable, controlled by the entity, and expected to generate future economic benefits before it can be recognised. These requirements guide valuation for financial reporting and business combinations.

Q3. What are IRAS requirements for intangible asset valuations?

IRAS expects valuations to be supported by reasonable assumptions, proper documentation, and arm’s length principles. This is particularly important for transfer pricing, restructuring, and tax compliance purposes.

Q4. When should the asset-based valuation approach be used?

This approach is suitable for assets such as internally developed software, databases, proprietary technology, and technical know-how, especially when market comparisons or future cash flow estimates are difficult to obtain.

Q5. Why is proper documentation important in asset-based valuations?

Comprehensive documentation explains the valuation methodology, cost inputs, and assumptions used. It supports compliance with SFRS and IRAS requirements while improving audit readiness and the credibility of valuation reports.