Valuing Blockchain Intangible Assets

The high rate of development of blockchain-based businesses has presented a new field of operation of professionals in corporate finance and valuation. Whenever an organisation that functions within the cryptocurrency or distributed-ledger area is acquired, listed, or otherwise required to prepare financial statements, it introduces with it a category of assets that is not readily amenable to the conventional accounting models. The valuation of intangible assets on blockchains has consequently become a niche field one that needs professionals to be both versed in the intricacies of decentralised technology, and skilled enough to meet the demands of accounting and capital markets.

The learning curve may be steep to the junior to mid-level professionals who are venturing into this field. The presence of network effects, tokenomics, smart-contract libraries, and on-chain user data as unique value drivers are created through blockchain ecosystems and cannot be found in any standard industry. However, the overall aim is the same as in any business combination, which is to determine, individually identify, and consistently measure each identifiable intangible asset obtained in compliance with such frameworks as the IFRS 3 intangible asset valuation requirements, International Accounting Standard(IAS) 38, and local regulatory advice.

This paper takes a tour through the theoretical underpinnings, practice-related, frequent pitfalls, and experience of this developing discipline. Even though you are about to do your first purchase price allocation (PPA) project based on a crypto exchange, or you are thinking of taking a course on valuing digital assets Singapore to train your technical abilities, the following insights are supposed to be a useful starting point.

Understanding the Blockchain Intangible Asset Landscape

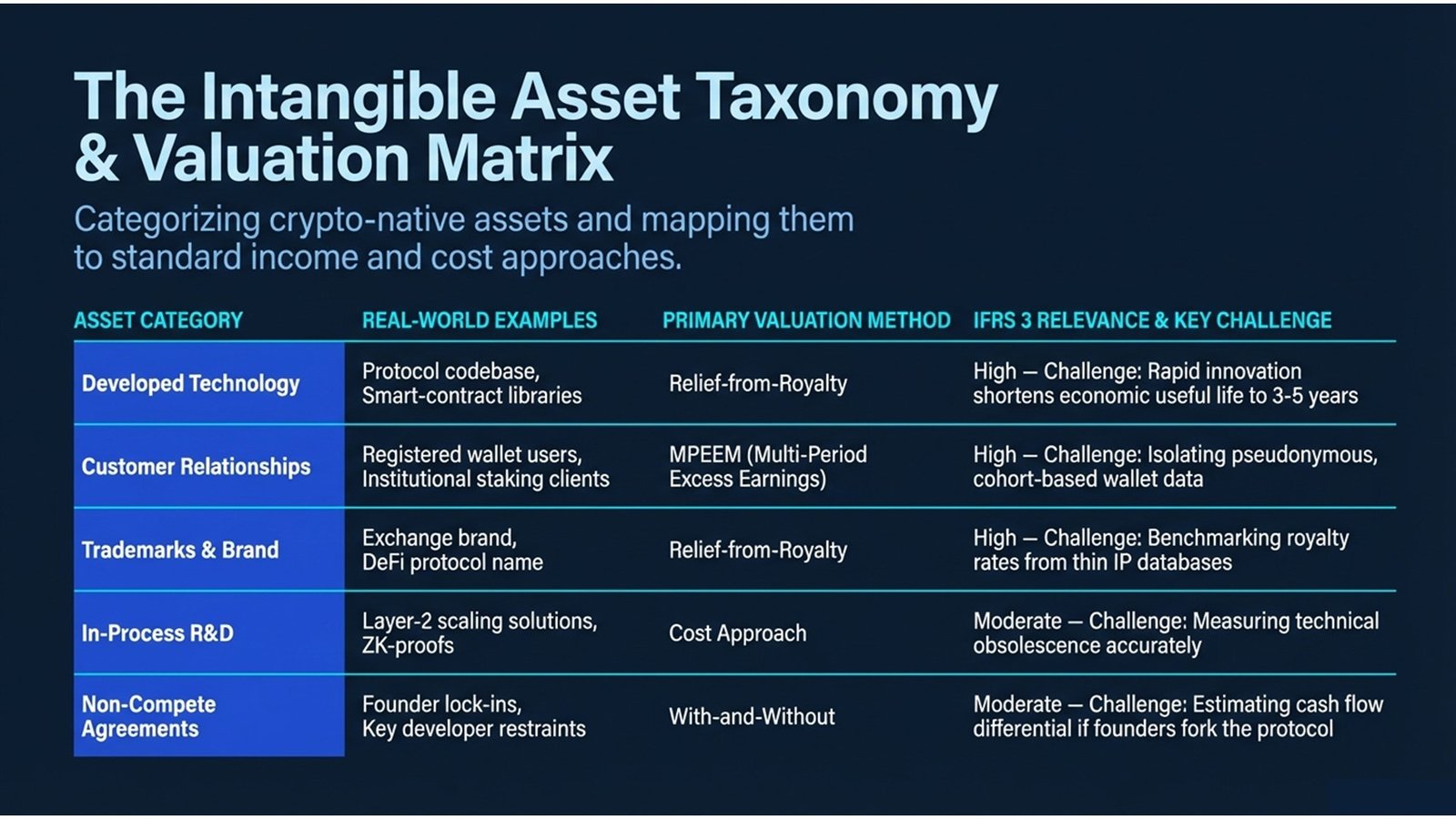

The practitioner has to know what it is that is being valued before a valuation model is constructed. Blockchain firms are able to maintain a relatively eclectic list of intangible assets, most of which are not reflected in the balance sheet of the target before acquisition. These include developed technology (including proprietary consensus mechanisms, validator node software and smart-contract libraries) and the customer-related intangibles (including registered wallet user bases and institutional staking relationships). It is also common with brand equity, in-process research and development (IPR&D) of next generation protocols and non-competition agreements with developers of the founding. The intangible asset valuation of blockchain requires that the practitioner should systematically catalogue such assets before they can use any methodology.

The following table summarizes the most prevalent types of intangible assets experienced by blockchain business combinations, along with examples of such and the valuation approaches that are used in most cases.

| Asset Category | Examples | Valuation Approach |

| Developed Technology | Libraries of smart contracts, protocol codebase. | Relief-from-royalty method |

| Customer Relationships | Wallet clientele, institutional customers. | Multi period excess earnings technique. |

| Trademarks & Brand | Protocol name Exchange brand, DeFi. | Relief-from-royalty method |

| In-process R&D | ZK-proof systems Layer-2 scaling solutions. | Cost or income methodology. |

| Non-compete Agreements | Lock-ins by the founders, the major developer constraints. | With-and-without method |

Table 1: Common Blockchain Intangible Asset Categories and Valuation Approaches

It should be mentioned that tokens as such, such as utility tokens, governance tokens and security tokens, may or may not be intangible assets under IAS 38. Characterisation of regulations is very crucial here. The definition of intangible asset may apply to a utility token that will provide the holder access to a platform service whereas a token that is a financial instrument will be considered in IFRS 9. This classification question is required to be solved at the beginning of the practitioners since it is the factor that defines recognition and measurement treatment.

Applying IFRS 3 in a Blockchain Context

Valuation policies of IFRS 3 intangible assets in a business combination imply that an acquirer must separately recognise intangible asset of the acquiree when the asset is identifiable, that is, separable or it is a result of contractual or other rights and the fair value of this asset is reliably determinable. This empirically results in a two-step screen, where one is the identifiability requirement; the second is the ability to come up with a defensible fair value. The blockchain companies have particular issues in both stages that are not encountered in traditional M&A deals.

In the identifiability front, the open-source code of a protocol might seem to be inseparable due to its visibility to the public. Nevertheless, the code is frequently less important than in the network of validators, participants of governance, and developers around it, who maintain it and upgrade it as the economic moat which cannot be easily replicated even in case the code can be forked. On the same note, customer relations of a blockchain platform can be pseudonymous, however, the economic value of a recurring active-wallet cohort is provably isolable and has been realised in a number of high-profile crypto acquisitions over the last few years.

Regarding measurement, the standard income-based approaches are the most consistent with the requirements of the IFRS 3 intangible asset valuation criteria, especially the relief-from-royalty method of the intangible assets of technology and brand, and the multi-period excess earnings method (MPEEM) of the intangible assets of customer relationships. Cost-based methods are also common to IPR&D with future streams of revenue being too speculative to be reasonably modeled. The following process flow table will indicate the step-by-step process that a qualified valuer would use in conducting a PPA in a blockchain business combination.

| Step | Activity | Deliverable / Outcome |

| 1 | Determine the perimeter of acquisition. | Listed assets and legal entity structure proved. |

| 2 | Filter screen assets in relation to IFRS 3 recognition requirements. | List of separable or contractual intangibles Long list. |

| 3 | Break down every intangible (technology, brand, CR, IPR&D, other) | Taxonomy and method of valuation of assets. |

| 4 | Gather financial and operation information on an asset-by-asset basis. | Turnover, expense statistics, traffic, royalty standards. |

| 5 | Construct valuation models and assumptions testing. | Draft Fair value estimates sensitivity Analysis. |

| 6 | Re-allocate the fair value of total purchase price allocation (PPA). | Completed PPA schedule, computation of goodwill. |

| 7 | Make technical valuation report and auditor support pack. | Approved report which is disclosed to the financial statements. |

Process Flow 1: IFRS 3 Purchase Price Allocation Step-by-step Workflow of Blockchain Transactions.

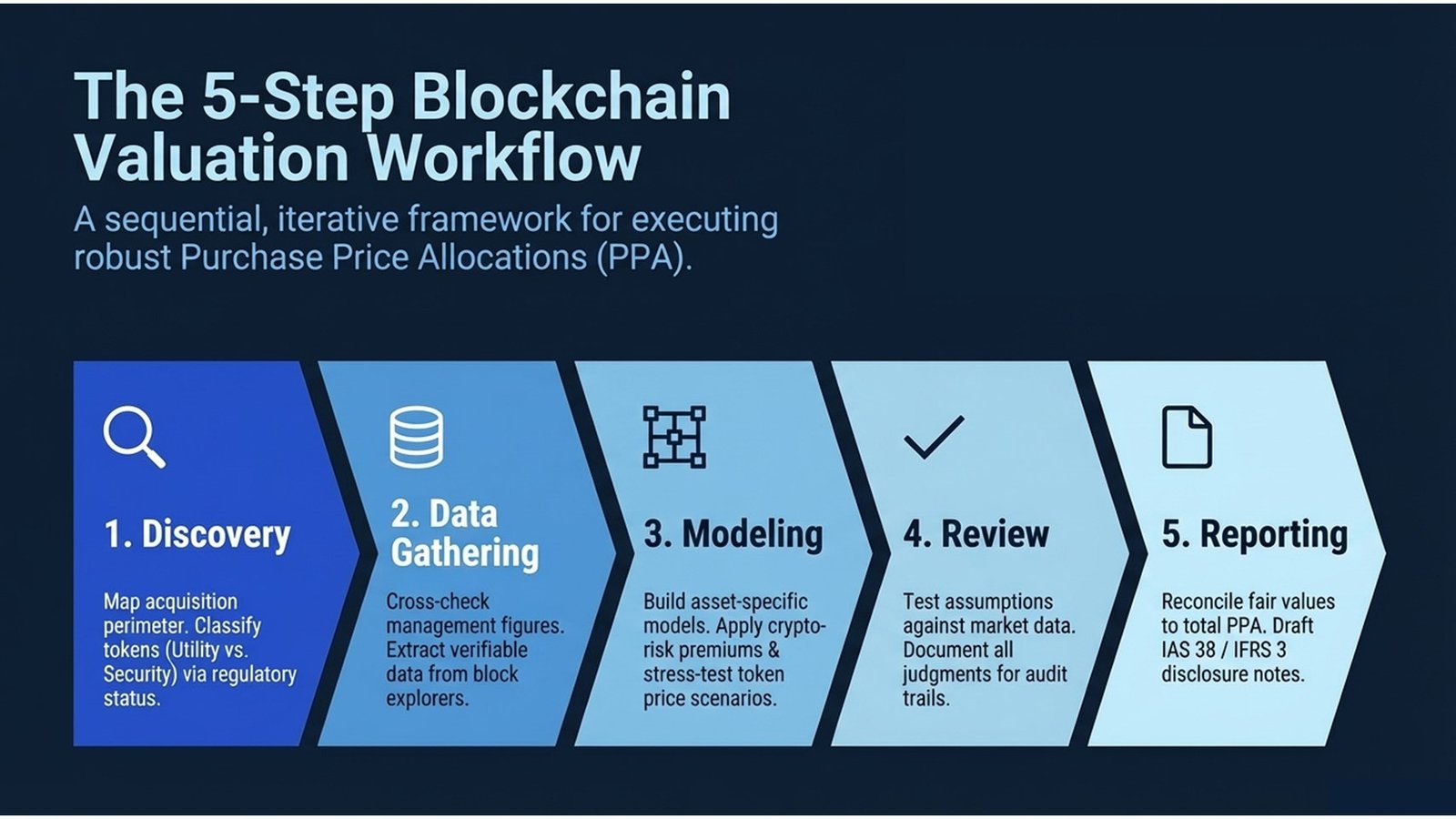

The Five Key Steps in Blockchain Intangible Asset Valuation

Based on the existing valuation practice and the nature of the decentralised technology business, a strong blockchain intangible asset valuation engagement includes five major steps. These are steps, which are sequential and are usually iterative as new pieces of information received at the later stages may necessitate a revisit of the conclusion made earlier.

The purpose and standard of value should be first established. Understanding as to whether the valuation is of IFRS 3 purchase price allocation, impairment test of IAS 36 or an independent fairness opinion will be determinative of which standard of value is applicable, the correct premise of value and the amount of documentation that is necessary to support the audit.

Second, carry out an exercise of identifying and classifying assets. This entails the process of going through legal due diligence documents, technical architecture documents, tokenomics whitepapers, and developer agreements to have a complete inventory of the assets. A common framework followed by many blockchain valuers is based on the structured checklist that is correlated with the categories of intangible assets of the AICPA and then is applied to crypto-related assets.

Third, compile on and off-chain information. The financial information of blockchain companies is abundant; in contrast to the traditional businesses, in which the management accounts are the primary source of financial data, blockchain companies have a variety of verifiable data on the blockchain: total value locked (TVL), number of daily active addresses, size of transaction fees, staking rate, and governance participation rate. The data retrieved through blockchain explorers and third-party analytics tools gives an objective cross-check with the amounts of data reported by the management.

Fourth, model and test valuation models. All the asset classes are modelled in the most suitable manner. At least, the following should be considered in sensitivity analysis: token price scenarios (of token-denominated revenues streams), adoption curves of protocols and discount rates. Since the crypto markets are highly volatile, more scenarios tend to be anticipated than in the traditional valuation.

Fifth, reconcil and record. The total consideration paid should be reconciled to the sum of fair values of all the identified intangibles and the fair value of the net assets that are tangible. Any goodwill is in the form of residual. The extensive documentation of assumptions, data source, and judgement is necessary, not only to the auditor, but also to serve as a basis of impairment testing in future, which will be necessary on an annual basis under IAS 36.

Real-World Cases and Lessons Learned

A number of historic deals in the crypto world have put into action and optimized the methodology of valuing intangible assets by blockchain. The example of the 2022 acquisition of a major US-based cryptocurrency derivatives exchange by a regular financial institution showed how complicated may be the idea of valuing an asset of a customer relationship when the customer base is defined by wallet addresses. Upon seeking advice of auditors, the acquirer valuation team applied a cohort-based MPEEM model to cluster wallets based on trading frequency and average revenue per user which later shaped the approach of other valuers to undertake similar exercises.

The other educative example was the purchase of a blockchain analytics company by an asset manager based in Europe. The main intangible, in this case, was the proprietary transaction-monitoring algorithm that the firm had built in five years internally. The relief-from-royalty approach was implemented based on the royalty rates that were benchmarked against the similar transactions of the financial crime compliance environment in terms of software licensing. The moral of the story: when choosing royalty rates in blockchain-related technology, one should take into consideration the high rate of technological advancement, which can reduce the economic usefulness of an algorithm to a short three to five years, which will have a huge impact on the present value of royalty savings.

The third example, of the restructuring of a decentralised finance (DeFi) protocol after regulatory intervention, showed that the with-and-without approach to the evaluation of non-compete agreements with founding developers is significant. In a restructuring transaction involving the founding team being restricted in their departure, the valuation team estimated the effect of the departure on the protocol revenue by simulating two cases one in which the founding team stayed and one in which it left and joined an opposing protocol. The value that was obtained was tangible and gave the restructuring committee a distinct economic justification of the contractual restraints. The case highlights that the use of IFRS 3 intangible asset valuation is more of a judgement than a technical modelling.

Challenges, Valuation Methods Compared, and the Role of Continuing Education

Possibly the most enduring threat in the blockchain intangible asset valuation is the lack of a sufficiently developed comparable transactions database. Royalty rate databases like RoyaltySource or ktMINE have been used to give benchmarks based on thousands of arm-length licensing deals in conventional industries. In the case of blockchain-specific intellectual property, these databases are thin in nature and the valuers have to frequently search through adjacent technology industries such as fintech, cybersecurity, enterprise SaaS before making judgement amendments to reflect the blockchain environment. The question raised by regulators and auditors has been how such adjustments are derived and they have demanded greater clarity in the documentation.

The estimation of discount rates is also a similar challenge. The weighted average cost of capital (WACC) of a blockchain company may be very sensitive to the assumptions made on the peer group and capital structure, especially at times when the company has a significant share in its treasury in volatile digital assets. Other practitioners take a build-up methodology where a risk-free rate is used and a progression of risk-premiums; industry, size, and company specific are added, to obtain the cost of equity. Others take proxies of market data of listed crypto-native companies. The two methods can be justified however the method adopted must be well written and used throughout the PPA.

The table below is a comparison of the primary value techniques that are typically used in blockchain intangible asset valuations, which can be used shortly by practitioners in determining the best technique to apply to each type of asset.

| Method | Best Used For | Key Challenge | IFRS 3 Relevance |

| Relief-from-Royalty | Technology platforms, IP | Choosing the suitable royalty rate. | High |

| Multi-Period Excess Earnings (MPEEM). | List of customers, major contracts. | Segregating contributory asset charges. | High |

| With-and-Without | Non-competes, agreements | Estimating the cash flow differentials. | Moderate |

| Cost Approach | Besepoke code, in-process R&D. | Measuring obsolescence accurately | Moderate |

| Market / Comparable | Liquid digital assets are referred to as tokens. | Similar data set made thin. | Low–Moderate |

Table 2: Methods of valuation -Comparison of Blockchain Intangible assets.

It is against this background that continuing education has turned out to be not just an optional, but also a professional need. Analysts in this work can be provided with both the theoretical background to the IAS 38 and the IFRS 3, as well as practical skills of blockchain data analysis, by having a structured digital asset valuation course Singapore-based programme, which is offered by professional bodies and specialist training providers. This is usually included in such programmes as token economics, smart-contract architecture, on-chain analytics, and case-based valuation modelling. Formal qualifications in the field are also now becoming more accepted by employers and regulators of those in the careers of cross-border M&A advisory, asset management or forensic accounting.

| Phase | Key Actions | Practitioner Considerations |

| Discovery | On-chain vs off-chain assets On-chain tokens off-chain tokens | Distinguish utility tokens from security tokens; check regulatory status |

| Data Gathering | Pull on-chain metrics: active wallets, TVL, transaction volumes | Verifiable data can be used by using blockchain explorers and DeFi analytics tools. |

| Modelling | Construct revenue based or expenses based models; compare royalty rates. | Stress-test token price stress-test crypto-specific risk premium. |

| Review & Challenge | Observe outside auditor; challenge assumptions in the market. | Record all the judgements to audit trail; expect queries by the regulator. |

| Reporting | Draft disclosure notes according to the IAS 38 and the IFRS 3 requirements. | Align with local regulatory expectations (MAS, SEC, FCA) where applicable |

Process Flow 2: Blockchain Intangible Asset Valuation Workflow — Phases, Actions, and Practitioner Considerations

Conclusion: Actionable Insights for Practitioners

The blockchain intangible asset valuation lies between the accounting rigour and technology literacy and market judgement. It is a science where the principles, identifiability, reliable measurement, economic useful life, discount rates, will be the same, but the circumstance under which the principles are used is a completely new one. Based on this discussion, there are a number of practical implications of the discussion to those professionals entering this field or moving up the career ladder.

Begin by making investment in the basic knowledge. The understanding of the IFRS 3 principles of the valuation of intangible assets and the working knowledge of how the blockchain technology creates and supports the economic value is the bare minimum. At this point, master on-chain data tools blockchain explorers, DeFi analytics tools, and token pricing APIs are quickly becoming standard tools of the valuer.

Documentation habits should be established at the beginning. All the assumptions, all the similar ones chosen as well as each of the adjustments made must be traceable and clarified. The closer blockchain-related valuations are examined by regulators and auditors, and the more clearly a practitioner can justify his or her work, the better he or she will stand out in an area where no standards are yet being set.

Find peer groups and formal education. Attending a digital asset valuation course Singapore or something similar in your jurisdiction will introduce you to practitioners dealing with the same issues in practice, and will introduce you to the recent regulatory and methodological changes before they are reflected in the textbooks. The profession is fast paced; the most competent persons in the profession will be the ones who learn in groups and constantly because the market will mature and the person will be in the best position to counsel the clients and the employers.

Lastly, accept the repetitive character of this work. The above-discussed cases indicate that valuation of intangible assets that are supported by blockchain can hardly be solved in one step. Coming back to assumptions with the emerging information, working independently with auditors and lawyers, and being intellectually humble about the boundaries of information available in the market is the sign of professional excellence in this specialist and fast-evolving sphere.