Intangible Asset Valuation in Malaysia for Brand Value

Introduction to Intangible Asset Valuation in Malaysia for Brand Value

Enter any Malaysian supermarket and you will instantly know some of the brands the font on a packet, the colour of a label, the name of a household product which has been in shelves over decades. It is not marketing that you are looking at. It is an asset, which can be worth hundreds of millions of ringgit, and should be duly identified, measured and reported in accordance with the international financial reporting standards.

The most challenging aspects of financial reporting in Malaysia are the intangible asset valuation. With the increasing number of companies by way of acquisitions, listing and/or investing in Bursa Malaysia, or even raising their own level of private equity capital, the necessity of quantifying what you cannot touch physically, such as brands, customer relations and technology platforms, licences and proprietary processes has never been more urgent. In the case of junior and mid-level finance workers, the knowledge of this space can get them in the audit and advisory, corporate finance and reporting activities in industries.

It is an article that discusses the valuation of intangible assets in particular brand value, and covers the standards that guide it, the measurement measures that are applied to it, the challenges that are actually encountered by the practitioners and the practical knowledge, which assists the professionals to develop in this area. It is the basis you should have whether you are going through a valuation report in the first time or even preparing to work in a valuation or transaction team.

The Framework Behind Valuation Numbers | Intangible Asset Valuation in Malaysia for Brand Value

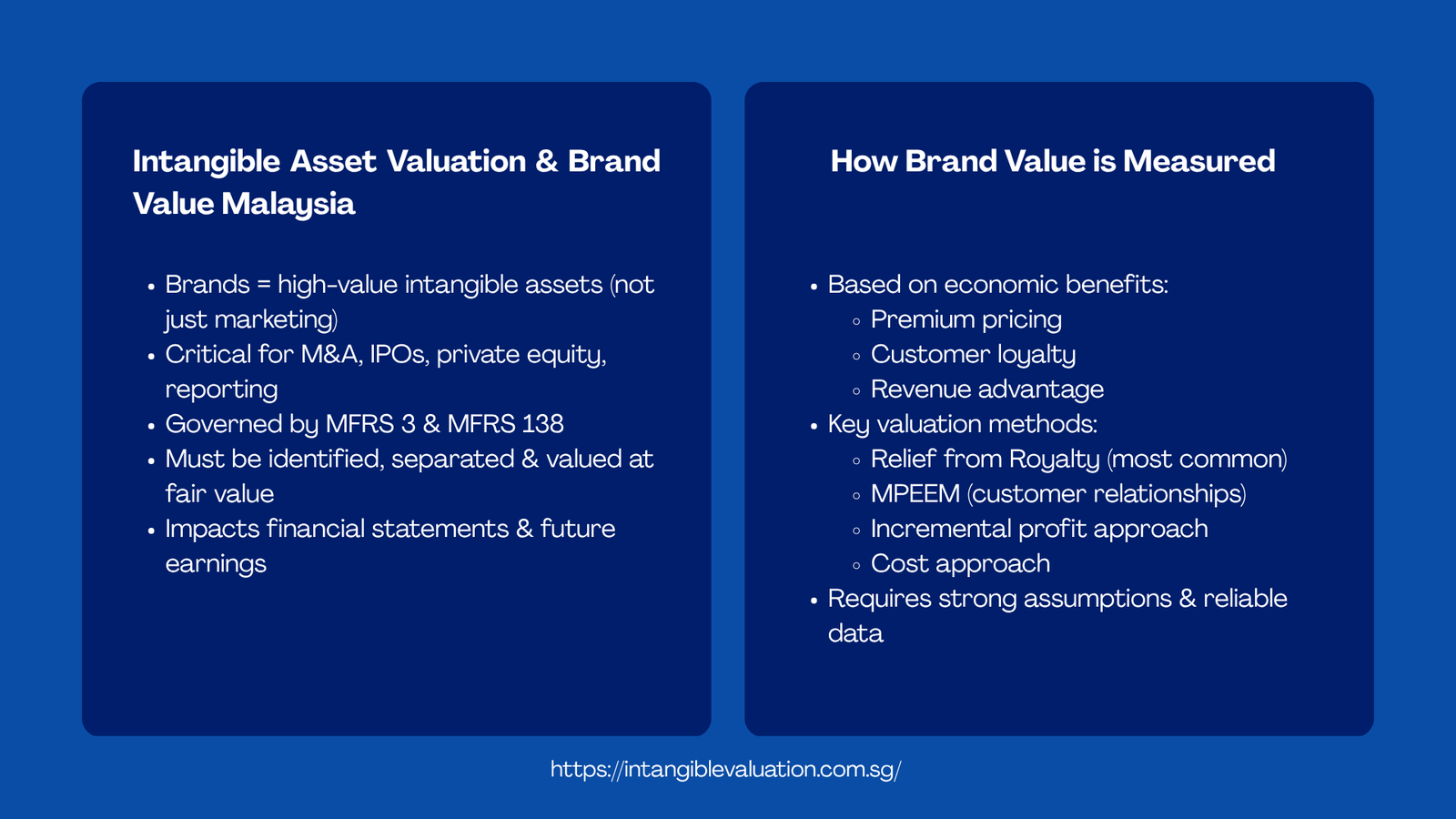

Any valuation specialist requires a clear legal and accounting framework in which he or she can place a number on a brand. In Malaysia, the companies that use the Malaysian Financial Reporting Standards (MFRS) framework have two prevailing standards with regards to intangibles: MFRS 3 which is a reflection of IFRS 3 in the context of business combinations, and MFRS 138, which is the local variant of IAS 38 in the context of intangible assets that are not part of business combinations.

The first step in learning how to value intangible assets under the IFRS 3 is a simple yet a powerful prerequisite that when a company buys another business, it should recognize and separately recognise all intangible assets that fulfil the definition in the standard as long as they are either separable (they can be sold or transferred separately) or are brought about by contractual or legal rights. It implies that a brand that was not previously included in the balance sheet of the acquiree prior to the transaction suddenly has to be included in the consolidated accounts at a fair value on the date of acquisition. The same is so in case of customer lists, non-compete agreements, proprietary recipes, software and franchise rights.

The reason why brands and tech require the appropriate models to value their intangible assets becomes obvious as soon as you comprehend that there is much more to lose. Two of the most frequently acquired intangible assets in Malaysian deals are brands and technology and they are also two of the most hard to reliably value. The value of a brand does not rely on the market price of a piece of machinery or the similar sales of a building, as the value of a brand is based on the future revenue prospects, consumer feelings, positioning competition, and legal safeguards of the brand. The badly designed model will result in a figure, which will not be able to pass an audit examination and not be able to be economically realistic, and the outcome of this will be visible in the income statement in terms of over or under amortisation costs in future years.

Understanding Intangible Asset Valuation in Malaysia for Brand Value

Brand value does not just represent recognition or reputation. When applied to financial reporting, the quantified economic advantage that a business may receive owning a particular brand is the premium pricing that it allows, the customer loyalty that it will command, how quickly it will bring in a revenue than an unbranded version would bring in revenue. The availing of that economic story into an auditable number is the essence of brand valuation.

The best illustrations in Malaysia can be found in the food and beverage industry, particularly in the case of the acquisition of existing local firms by the bigger regional or foreign organizations. In case a domestic food manufacturer is purchased then the acquirer needs to know the extent to which the price paid is associated with the brand, the extent to which it is associated with the customer relations, and the extent to which it is associated with other identifiable assets. All of these elements must be valuated separately, assess the useful life separately, and amortised separately – or where the brands have unlimited lives, impaired every year.

There is another useful lens in the retail sector. A Malaysian retail chain having a strong brand equity, a customer base and a developed portfolio of the own brand is a complicated case of valuation. The brand might be practically something that cannot be separated with the customer relationships and the store network, but under the IFRS, they should be separated to be included in the accounting. This is where IAS 38 intangible asset valuation: why brands and tech need proper models is more than a technical issue, it is a practical challenge, and it determines the way the financial statements are interpreted and the way the management takes post-acquisition decisions.

In the case of technology companies, the situation is even more difficult. When a Malaysian fintech is purchased by a banking group, it includes proprietary technology stack, user base, and possibly a recognisable brand. All these must be appreciated individually, employing different methodologies, different input of data, and different assumptions of useful life and obsolescence risk. Not only the opening balance sheet is dependent on the quality of that work but the earnings profile of the combined entity in future years.

5 Key Methods of Intangible Asset Valuation in Malaysia for Brand Value

An intangible asset has no right way of valuation. The right approach would be based on the nature of the asset and availability of data, the objective of the valuation and the stipulations of the relevant accounting standard. There are five contemporary ways of valuing intangible assets, which are well known in practice and knowledge of each one provides finance professionals with a valuable framework through which they should review and doubt valuation outputs.

| Method | Best Used For | Core Logic |

| Relief from Royalty | Brands, trademarks, technology | Is of the opinion that the asset is worth the savings of royalties that are occasioned by holding the asset as opposed to licensing. |

| Multi-Period Excess Earnings (MPEEM) | Customer relationships, key contracts | Recognizes cash flows attributable to the asset, which have been adjusted by deducting returns to the entire assets. |

| Incremental Cash Flow / Premium Profit | Brands with pricing power | Evaluates the extra profit made when compared to an unbranded or generic substitute. |

| Cost Approach (Reproduction / Replacement) | Technology, databases, assembled workforce | Determines the cost of recreation or replacement of the asset at the present price. |

| With-and-Without Method | Non-compete agreements, exclusivity rights | Comparisons of business value in place or value without the place. |

The most prevalent brand valuation method in Malaysia as well as abroad is the Relief from Royalty method. The reasoning is beautiful: in case you did not own the brand, you would have to license it with another person. The brand as a value is then the current value of the royalty that you are spared by having it. To implement this approach, it is necessary to choose a suitable royalty rate, which is usually based on similar licensing contracts or industry databases and apply it to estimated revenues that could be attributed to the brand. The resulting stream of royalty earnings is then discounted to present value by a risk-discounted interest rate.

The customer relationships are the most valuable intangible in a service business acquisition, and the standard method in acquiring a business of that type is the Multi-Period Excess Earnings Method (MPEEM). The approach separates cash flows generated by a given customer base and then removes the returns which can be accredited to all the other assets the brand, the technology, the workforce, the fixed assets and only the earnings due to the customer relationship are left. One of the more technical aspects of the IFRS 3 work in valuation that is a concept and this is a contributory asset charge concept, and this is one of the areas that junior professionals can require time to build intuition.

The other approaches have a narrower role. Cost method is most applicable to technology assets, especially in situations where the asset is not directly contributing to revenue but in the operations. The with-and-without approach is especially applicable in non-compete arrangements, where the enquiry is not what the asset yields, but what is lost by the business in the event such covenant is not present.

4 Stage of Intangible Asset Valuation in Malaysia for Brand Value

Having an idea of the process involved in valuing an intangible asset assists the finance professional to play a more important role in the process, either in preparing information to be presented to an external specialist, or by reviewing a draft report, or explaining the exercise to a non-finance stakeholder.

| Stage | What Happens | Who Is Involved |

| 1. Asset Identification | All intangible assets to be valued include defining and documenting intangible assets, according to legal, contractual and separability criteria. | Valuer, legal counsel, management. |

| 2. Data Gathering | Gather financial forecasts, market information, royalty rates, customer information, and IP reports. | Finance department, commercial director, IT. |

| 3. Modelling and Analysis | Develop valuation model of each asset, methodology, stress-test assumptions. | Valuation specialist |

| 4. Audit and Review | Introduce current results to auditors, answer questions, complete report. | Valuer, audit, CFO or finance director. |

Stage one – identification of the asset- is the stage in which most engagements succeed or fail at the initial stage. Malaysian businesses, especially those which have expanded via organic means other than acquisitions, do not possess a clear internal listing of their intangible resources. In an acquisition that creates an IFRS 3 exercise, the management is often shocked to find out that there are numerous intangibles that have to be valued. An example of this is a Malaysian logistics company that has been acquired by a regional infrastructure group and may have route licences, long-term customer contracts, fleet management software and an established brand; each of these needs different treatment.

Stage two – data gathering – is the stage where the junior and middle-level professionals can exert the greatest influence. The quality of the inputs has a complete effect on the accuracy of the valuation: projected revenues, customer retention rates, royalty rate benchmarks, discount rate inputs, and useful life assumptions. When the finance professionals know what the valuation model needs and have access to clean, well-documented information, then the engagement will be smoother and the output more justifiable.

Stage three – and four belong mostly to the specialist domain, whereas those in the field of finance that know how to value intangible assets under IFRS 3 will be in a much greater position to be critical in reviewing the model outputs as well as participate constructively in the sign-off process with the auditors.

Common Challege in Intangible Asset Valuation in Malaysia for Brand Value – Brand and Technology Valuation

There can be no complete discussion of the intangible asset valuation without reference to what makes it really hard. These technical issues are genuine and their knowledge generates the type of practical intelligence that is not often taught in text books..

| Challenge | Why It Arises | How It Is Managed |

|---|---|---|

Separating brand from goodwill | Both brand and goodwill are excess value; to draw the line between them, one needs to study them carefully. | Enforce separability and contractual standards; capturing rationale. |

| Selecting royalty rates | Similar licensing information is unavailable particularly to the niche Malaysian brands. | Utilize a variety of data sources; use judgement that is recorded. |

| Estimating useful life | Brands can be indefinite or finite, and the option has an impact on amortisation. | Evaluate renewal history, competitive forces and management intentions. |

| Technology obsolescence | Assets Tech assets are depreciated at a rapid rate; useful life assumptions can be excessive. | Be conservative in assumptions; check in the industry. |

| Auditor alignment | Assumptions that can be challenged by auditors include discount rates and revenue forecasts. | Write sensitivity analysis; record all the important inputs and their sources. |

The most educative issue within the Malaysian practice concerns the choice of royalty rates among the local brands. As compared to global brands that have a long history of public licensing, a popular Malaysian brand in the consumer goods market might have very little similar transaction information. Valuers have to rely on international databases, make market size and brand strength adjustments, and support their decisions with a systematic reasoning. This is one of the areas where the main defence against challenge is professional judgement which is supported by experience and intensive documentation.

There are other challenges of technology valuation. Fintech, e-commerce and software firms are becoming acquisition targets in the expanding digital economy in Malaysia. The deal rationale is based on their technology assets, which may be proprietary algorithms, mobile applications, or integrated platforms. However, technology wears out fast and what is a state-of-the-art platform today might be partially outdated in three or five years. Valuers that do not consider this risk in their assumptions of useful life and cash flow will have a figure that appears plausible when they are signing but which causes impairment charges within the initial few reporting periods after the acquisition.

The moral of the story to the financial professionals is to always get into the habit of questioning what makes this wrong when examining the valuation outputs. The practical tool of exploring that question is sensitivity analysis, which good valuation reports will always have. When a slight adjustment in the discount rate or growth in revenue assumption can affect the asset value materially, it is important information both to the finance department and the audit committee.

Career Groth Path in Intangible Asset Valuation in Malaysia for Brand Value

To those professionals who are interested in transitioning to intangible asset valuation as either a career specialization or a value add competency in a larger finance or audit position, the road is both available and well organized.

| Career Stage | Recommended Focus | Practical Actions |

| Early Career | Standards and terminology | Know major standards of IFRS/MFRS and understand a valuation report. |

| Mid-Level | Methodology and modelling | Use modelling in actual PPA and impairments. |

| Senior | Judgement and communication | Own engagements and promote international qualifications. |

Real competency in this area can only be developed best when one is exposed to live engagements, albeit in a supportive capacity. Practical knowledge is gained much more quickly through preparation of data rooms, reviewing model inputs, auditor walk throughs, and reading final valuation reports in a critical manner than through studying alone. The volume of work done by the Big Four accounting firms, mid-tier advisory practices, and specialist valuation boutiques in Malaysia on the intangible asset work involving IFRS is all significant, and at the analyst or associate level professionals with strong accounting or finance background are hired.

Knowing five modern methods of valuing intangible assets also provides you with a vocabulary and framework that will prove invaluable regardless of what part of finance your work falls in. This knowledge is useful to audit specialists who look at fair value estimates, corporate finance analysts who model post-acquisition earnings, as well as in-house finance teams that are preparing regulatory submissions. And since the debate on the quality of reporting in Malaysia remains unresolved because the implementation of IAS 38 intangible asset valuation: why brands and tech need proper models continues to inform the discourse around what is considered sound technical valuation work and what is considered sound financial statement preparation, professional people who can bridge the gap between the two will be worth their weight in gold.

Conclusion: Intangible Asset Valuation in Malaysia for Brand Value

The valuation of intangible assets is not a side show in Malaysian finance – it is the core of deal structuring, financial reporting and investor and regulator evaluations of corporate performance. The brands, technology and the relationship with the customer are frequently more valuable than actual assets on the balance sheet, and the error to measure them has real repercussions to all people who are dependent on these numbers.

The most practical actions to be taken by the professionals at the junior to mid-level level are as follows: read MFRS 3 and MFRS 138 focusing on the recognition and measurement requirements and not on the definitions. Identify a valuation report, either by an audit engagement, a transaction which your firm has been engaged in, or a publicly disclosed report, and critically go through it, asking yourself what method was employed and why? Create a simple royalty model in a spreadsheet, using publicly available data on one of the Malaysian brands that you can research, and discover how sensitive the result is to changes in the main assumptions.

All this does not need the title of seniors or a specialist to be started with. It involves inquisitiveness, logical thinking and readiness to dig beneath the figure of the numbers. In a career where learning how to appreciate intangible assets under the IFRS 3 is becoming a likely requirement rather than an extraordinary one, it is one of the more tactical career choices that a finance specialist can make to invest in the same.

Malaysia has the most successful businesses, whose brands, platforms, and customer bases are real and can be valued. Professionals who are able to gauge them properly, rigorously, and clearly communicate, will always be at the table.